Eskom’s Medium-Term System Adequacy Outlook 2026–2030 portrays a power system entering a delicate transition. (Image: iStock)

Eskom’s Medium-Term System Adequacy Outlook 2026–2030 portrays a power system entering a delicate transition. (Image: iStock) Contrary to popular belief, Eskom’s National Control Centre is not located at Megawatt Park in Midrand. It is in Germiston, and it’s the beating heart of South Africa’s energy system. This is where the Eskom system operator (SO) can be found and it is where the decisions are made about when rolling blackouts will take place and who will be affected.

/file/dailymaverick/wp-content/uploads/2023/06/image1-2.png "Eskom National Control Centre, Germiston. (Photo: Supplied)")

The SO must ensure that the grid’s 50Hz frequency is maintained at all times. If there is an unplanned outage at a power station, it is captured by the Supervisory Control Acquisition Data system. If an alternative supply is not immediately available from other power stations or other backup systems, then the SO notifies all the distribution control centres around the country as to what loads need to be shed and when.

We all depend on the handful of people who monitor the national grid 24/7 and make the quick decisions that affect whether we will have lights that day. After 16 years of load shedding, our SO might well be one of the world’s most competent load shedding managers.

Unlike citizens in many other countries in the world, when it comes to energy, South Africans take for granted that all their energy needs will be met by one gigantic state-owned company — Eskom. This includes the assumption that the company that generates energy from its 15 enormous coal-fired power stations is also responsible for transmitting the electricity via the national electricity grid transmission system to every corner of South Africa.

At the subnational “distribution” level, households and businesses know they are supplied either by their local municipality or by Eskom directly. The split is roughly 50/50.

In reality, in many parts of the world, generation, transmission and distribution have been “unbundled” into separate operating entities, some remaining state-owned, while in many cases these entities are privately owned.

Since the publication and Cabinet approval of the Eskom Roadmap in 2019 by the Department of Public Enterprises, the government’s official position has been that Eskom needs to get unbundled into three entities: generation, transmission and distribution. Eskom has worked hard to abide by this policy framework, starting off by internally restructuring into three separate “divisions” of generation, transmission and distribution.

This has included the setting up of the National Transmission Company of South Africa (NTCSA), wholly owned by Eskom Holdings Ltd, which is, in turn, owned by the state. However, it could not be formally launched until board members have been approved by DPE and the Cabinet, which has still (inexplicably) not happened.

Many private sector players are still hopeful that four years after the publication of the Eskom Roadmap, the NTCSA might actually get established. Many trade unions and radical NGOs remain sceptical about this idea because they see it as the first step towards full-scale privatisation not only of generation, but transmission (ie, the grid) as well.

Once the NTCSA has been fully established with its own board, CEO, executive team and staff, all assets related to transmission can be transferred to NTCSA. These are the cables, substations, pylons, depots and land holdings associated with the structure and operation of the transmission business. Excluded from this are the distribution assets that will be transferred to a distribution entity of some kind (but details about this remain opaque).

Private investors

The generation assets (power stations and associated infrastructures) will remain with Eskom until they are sold to private investors (if they are functional and not too old, such as Medupi and Kusile, and even Tutuka if it wasn’t so corrupt), decommissioned (because they are old) or retained as profitable generation units by Eskom Generation.

We should, therefore, anticipate a future where many public, municipal, community, cooperative and private actors will own energy generators and the NTCSA will either be the buyer and onward seller of this electricity, and/or charge generators a fee for using the grid to “wheel” electrons across to a distributed market of diverse buyers.

In his Budget Speech in February 2023, the Minister of Finance, Enoch Godongwana, sealed Eskom’s future as envisaged in the Eskom Roadmap by making it clear that the transmission business is what Eskom’s future is all about. By cutting off funds for fixing Eskom’s power stations, Godongwana effectively put an end to the illusionary notion that the power stations can be fixed as a solution to load shedding. Even when the newly appointed minister of electricity boldly announced in April 2023 that he would be going to Cabinet with a budget to fix the power stations, Godongwana quickly quelled that expectation.

Reimagining Eskom as primarily a transmission rather than a generation business is not simply about changing the institutional ownership of the grid. On the day after the NTCSA is formally launched (ideally before Christmas 2023!) with a balance sheet that includes all the transmission grid-related assets and related debt (and hopefully not more than this), it will be faced with a massive challenge.

For at least the past decade, the grid has been the Cinderella of the national energy system. Faced with its massive generation challenges as a result of poor long-term planning by the government since 1998, plus ongoing corruption and sabotage, Eskom has redirected capital away from the grid. As a result, there is not only a backlog when it comes to maintenance and rehabilitation of the cables and substations, but also a massive backlog in the capacity of the grid to handle additional generation capacity.

The results of Bid Window 6 brought home the seriousness of this reality: of the 4.2GW targeted for Bid Window 6 announced in November 2022 by the minister of mineral resources and energy, Gwede Mantashe, less than 1GW was approved because many bidders selected sites where there was no available grid capacity (eg, Northern Cape).

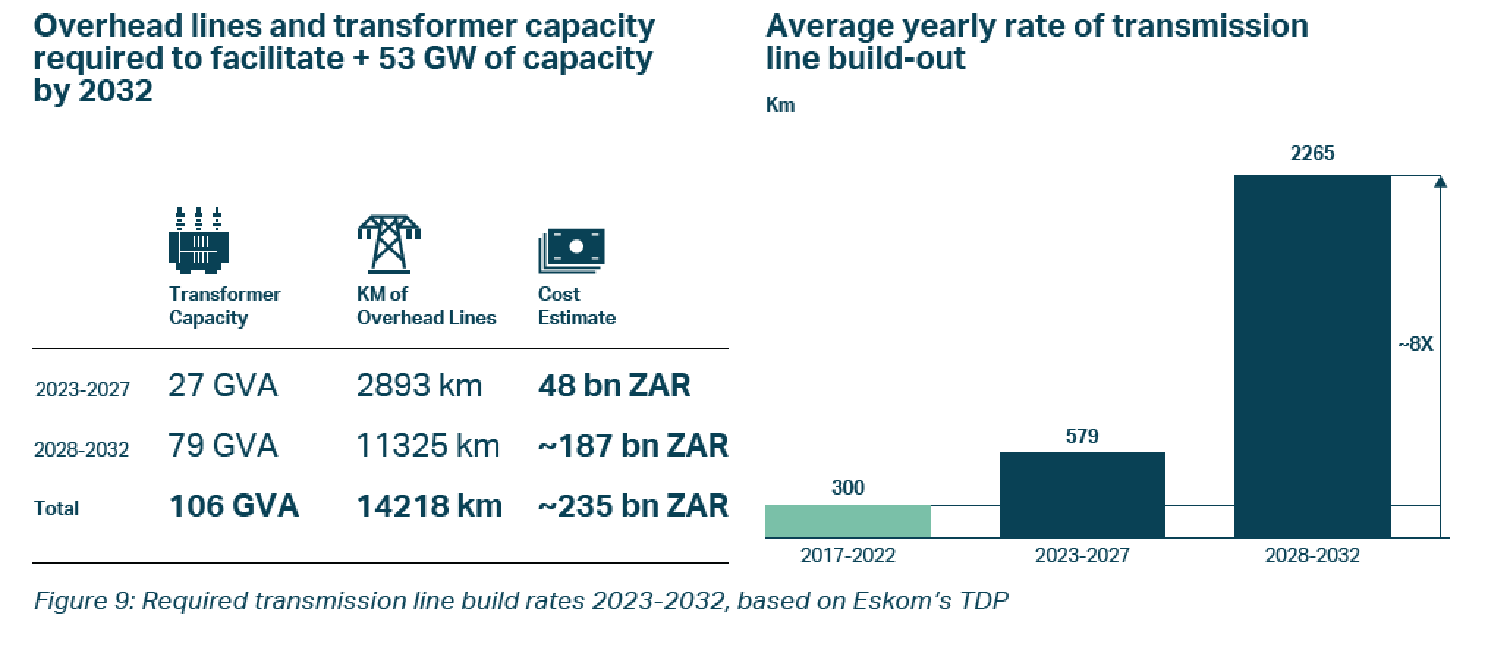

According to Segomoco Scheppers, the MD of Eskom’s Transmission Division, between 2013 and 2022 only 4,347km of new powerlines were added to the grid, ie, just over 400km per annum. This, he argued, needs to increase to 1,500km per annum for the 10-year period 2022-2032 if sufficient capacity is going to be in place to connect all the planned new generation (from multiple sources) to the grid.

In other words, starting now, we need to ramp up from 400km per annum to 1,500km per annum. Never before in South African energy history have we achieved this build rate. The highest we achieved was in the 1980s during a phase of massive growth in energy infrastructure construction — our maximum was 1,200km per annum, and that was during a time when far fewer regulations governed the construction of infrastructure.

The shock results of Bid Window 6 due to grid constraints have led many to predict that load shedding will be with us for many years because we simply do not have the grid capacity to connect new energy generators in the short term. And, we need to note, it takes 5-7 years to get through all the regulatory hoops and construction challenges to realise grid extensions in practice.

Running out of runway

With around 30GW of renewables in the pipeline (according to the Energy Action Plan), this is surely a valid concern. However, South Africa is not the only place where there is a mismatch between grid capacity and rapidly growing renewables sectors — while renewables have a lead time of 3-5 years, grid extensions take 5-7 years. Given these realities, running out of runway is a distinct possibility.

Minister Mantashe has also just announced the targets for Bid Windows 7 and 8: 5GW each! If Bid Window 6 could not go above 1GW, how on Earth are we going to connect 10GW? Thanks to his regular Friday press briefing, we now know that the minister of electricity spends a lot of time worrying about this question. And significantly, the National Electricity Crisis Committee (Neccom) has (finally) set up a workstream on the transmission grid. It would seem that the grid may be emerging from its status as the Cinderella of the national energy system.

However, these pessimistic conclusions are based on a failure to make a distinction between long-term planning for areas without grid capacity (eg, Northern Cape) and shorter-term opportunities for creating grid capacity. In our Better Finance, Better Grid report, the Centre for Sustainability Transitions working in partnership with the Blended Finance Taskforce and the Centre for Renewable and Sustainable Energy Studies explore this distinction in great detail, ending up with a far more optimistic conclusion that will be discussed further in a Daily Maverick-hosted panel discussion on 28 June.

When it comes to grid planning for a future based on renewables (because it is the lowest-cost option, and the by-product is decarbonisation, which is good for exports and the environment), it is necessary to take into account:

- The quantum of future demand for energy;

- The geographical location of future demand (ie, where urbanisation and industrialisation are taking place);

- The geographical location of the best wind and solar resources; and

- Where existing grid capacity is located in light of the long lead times to extend the grid.

There are areas in South Africa where there is sufficient cable infrastructure, but limited substation infrastructure. We estimate that there is potential for realising 17GW of grid capacity in the short term if urgent action is taken now to supply these areas with a sufficient number of substations of an appropriate size. This would create the grid capacity needed for just over half of the 30GW of new-generation capacity that is in the pipeline.

The bulk of this 17GW of potential short-term capacity is in the Free State (2.3GW), North West (3.8GW), Mpumalanga (5.1GW) and Western Cape (1.8GW). While the wind and solar resources in some of these areas are less favourable than the Northern Cape, which could increase costs by as much as 10%, the cost of the energy generated remains significantly lower than new coal-fired power. Furthermore, the quality of the resource in these “less favourable” areas is still much higher than in most of Europe where renewable energy is profitably generated.

But not all of the 30GW of new capacity will require grid capacity. The minister of electricity has referred to the need for 15GW of additional renewables. If this refers to utility-scale renewables procured via the Renewable Energy Independent Power Producers Procurement Programme, then this makes sense — 10GW from Bid Windows 7 and 8, plus the unrealised remainder from Bid Window 6 (about 3GW) plus whatever emerges from the ill-fated “Emergency Round”.

Neccom estimates that 9GW of “embedded generation” are in the pipeline — this refers to renewables built by large energy users like mines, factories and malls, and in most cases, this energy will be supplied directly to the users without burdening the grid.

Rooftop solar revolution

Then there is the rooftop solar revolution that was unleashed by the tax incentives announced in the Budget Speech in February that could well result in up to 7.5GW of solar PV energy by the end of 2024. Like embedded generation, solar rooftop PV does not require additional grid capacity. However, the massive increase in embedded generation and rooftop solar will require system changes to effectively manage the stability of the grid.

According to Eskom’s well-formulated Transmission Development Plan (TDP), R48-billion will be required for the period 2023-2027 to cover the cost of 2,893km of overhead power lines plus 27GVA of transformer capacity. For the period 2028-2032, this would have to increase to 11,325km plus 79GVA of transformer capacity costing R187-billion. As already indicated, the focus of the 2023-2027 period for transformer capacity will be where powerlines are mostly in place, ie, Free State, North West, Mpumalanga and Western Cape.

The advantage of the R235-billion investment requirement is that it is not a difficult investment for public and private investors to comprehend. Like a toll road, grid investments unlock flows that can be levied, in this case, electricity from a multiplicity of generators.

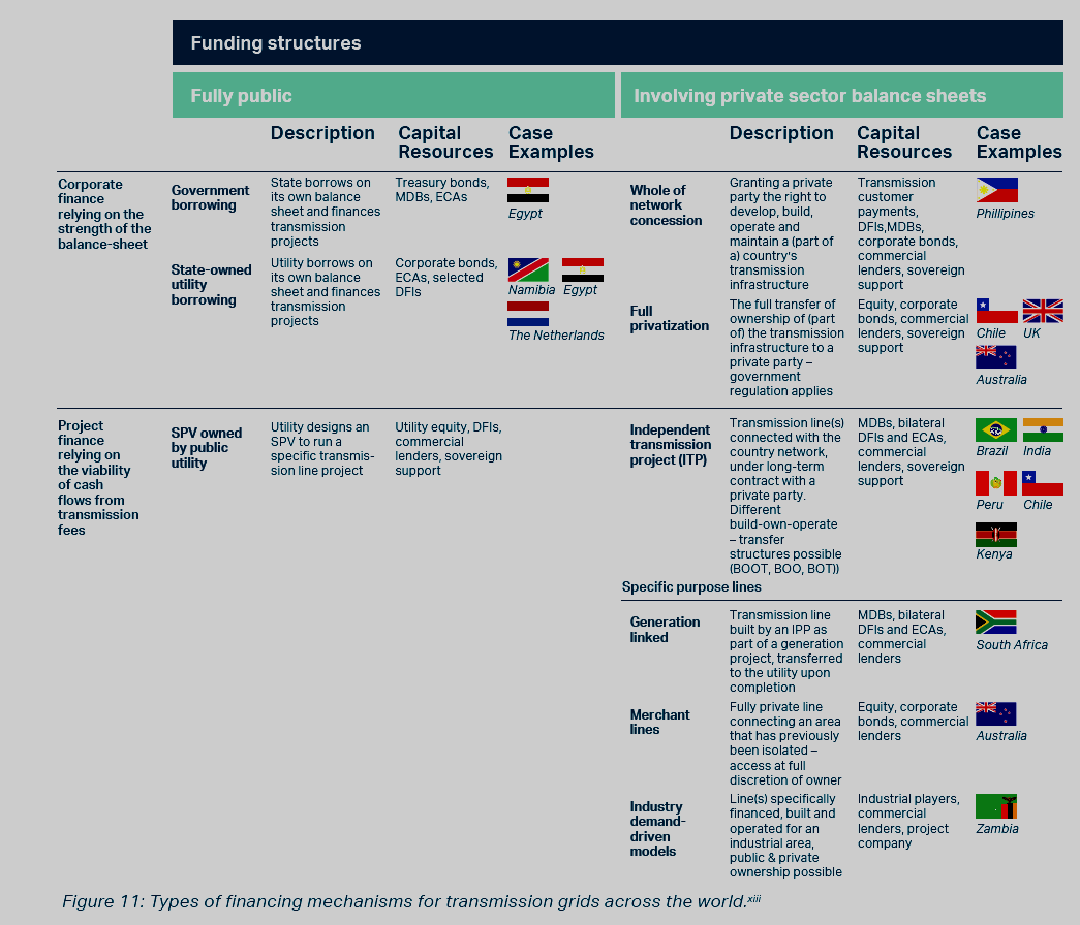

In the Budget Review released together with the Budget Speech in February, the National Treasury opened the door for concessioning off sections of the grid to unlock private-sector investments in public infrastructure. While some fear this is aimed at privatising the grid, in reality it could create space for the “build-operate-transfer” (BOT) solution whereby a piece of infrastructure is concessioned, upgraded/extended by private developers, and later transferred back to the state after targeted returns have been achieved.

Our research shows that many other countries have in recent decades faced the challenge of financing grid extensions, especially in the context of the transition to a decentralised and distributed renewables-based system. The result is a vast range of public and private sector solutions.

When it comes to corporate finance, Egypt, Namibia and the Netherlands have adopted fully public solutions, while in the Philippines, Chile, Australia and the UK more private-sector solutions have been implemented. For project finance, many more examples exist of countries where private project-level funding is available for publicly owned systems.

Blended finance is becoming the preferred approach. According to this approach, for every $1 of public funding provided by a development finance institution (DFI), like the Development Bank of Southern Africa, $10 of funding is leveraged from private-sector sources. Typically, the DFI acts as the lead arranger and provides a “first loss” and/or tenor extension facility to reduce the risk for private sector investors who would otherwise invest in less publicly useful assets such as offshore financial instruments or yet another unneeded mall. (Mohale Rakgate, CEO of the Infrastructure Fund, South Africa’s largest blended finance vehicle, will speak on the panel on 28 June). DFI and/or sovereign guarantees also play a crucial role in blended finance solutions.

We estimate that the transmission build programme can increase output eight times by addressing four key barriers:

- Access to sufficient capital;

- Addressing planning and permitting hurdles;

- Procurement of materials; and

- Building the capacity of contractors and their workforces.

Access to sufficient capital will depend on whether or not Eskom Holdings chooses to impose too much debt on the newly formed NTCSA. Given the R400-billion-plus debt held by Eskom Holdings, there are fears among potential investors that too much of this debt will be transferred to the NTCSA, thus preventing the upscaling of funding for the grid.

On planning and permitting, the Department of Forestry, Fisheries and the Environment has promulgated the Renewable Energy Development Zones (REDZ). Planning and permitting within the REDZ will be fast-tracked.

On the procurement of materials, it would be unfortunate if South Africa were forced to relax local content requirements in favour of imports to fast-track the delivery of renewables. This would subvert the potential for job creation via upstream industrialisation.

Finally, one of the biggest challenges will be the ramping up of the capacity of South Africa’s engineering, procurement and construction (EPC) contractors so that implementation can go from 400km per annum to at least 1,500km per annum.

Adenco, for example, is one of the biggest black-owned EPCs with a track record in building substations and powerlines (the Adenco CEO will speak on the panel on 28 June). Big corporate players include Siemens and Murray & Roberts; other smaller South African companies include AMP Property Management and Land Acquisition, ARB Electrical Wholesalers, Babcock, Conco Group and Konupi Contractors. Unless these companies have the long-term certainty to justify investing in upscaling capacity to pursue future business opportunities, it is unlikely that it will be possible to achieve the target of at least 1,500km of additional grid capacity per annum any time soon.

By the early 2030s, our energy system will be unrecognisable compared to the present. Load shedding will be a memory, Eskom will have become a transmission business (and will in all likelihood still be state-owned), most coal-fired power stations will have closed down, and hundreds of publicly, municipally, socially and privately owned electricity generators will have proliferated across the length and breadth of the country.

Wheeling will have become the norm and everyone will have access to affordable electricity. But for the system operator in Germiston, life will have become far more complex. Maintaining a stable 50Hz frequency when the bulk of electricity comes from a vast multiplicity of small-scale generators will require new tools for monitoring and stabilising an increasingly complex grid. But the good news is that Eskom’s system operator will no longer need to be the world’s most skilled load shedding manager. DM

Professor Mark Swilling is co-director of the Centre for Sustainability Transitions at Stellenbosch University.

Comments

Scroll down to load comments...