CORPORATE CORNER

SA Company Results: The Latest

Your one-stop shop for all the latest corporate results of South Africa's major companies.

Tuesday, 23 April 2024

Capitec’s success story — 22m clients and counting…

Once upon time, it was the “newcomer” in the banking industry, but Capitec has grown to become a leading case study in banking success, boasting an active client base of 22-million, earnings of R10.6-billion, and 11.2-million app users for the year to end February 2024.

Transaction volumes increased 21% to 9.9 billion, driving a 29% increase in transaction and commission income to R14.8-billion. Gerrie Fourie, chief executive officer of Capitec, says this growth aligns with the bank’s strategy of shifting the market towards digital banking.

Strategic initiatives such as “value-added services”, payments and Capitec Connect, contributed R2.9-billion in net income, while the insurance business contributed R3-billion, and the relatively recently launched business banking division brought home R478-million in profit after tax.

Capitec App users increased by 180,000 a month and registered more than 11 million logins a day – that’s more than 500,000 people using the app every hour, illustrating how the brand has become a part of people’s daily lives. Fourie says the bank’s strategy has remained razor-focused on the future.

“Over the last three years, we’ve invested R6.3-billion in re-platforming our systems and migrating our data to AWS Cloud services, developing innovative payment solutions and building three new businesses,” he says.

Card payments increased by 30% to 2.5 billion, which means the Capitec card was used 6.6 million times daily across South Africa and in top international destinations. The bank further introduced Capitec Pay, the first API-based payment solution in South Africa, which enables secure card-free online shopping by simply entering a cellphone number and authenticating it using the Capitec app. Capitec Pay processed 134 million transactions with a value of R26.7-billion.

Clients with inflows of more than R15,000 a month into their Capitec account have increased by 17%. Fourie says more than 2.9 million clients have net salaries of more than R15,000 paid into their Capitec accounts, with 600,000 clients depositing salaries of more than R50,000 a month.

The bank implemented a new online banking platform that allows clients to onboard remotely in minutes with no paperwork, for a low monthly fee of R50 and the same low transaction fees as personal banking for all businesses, regardless of size.

It seems that having conquered the South African market, Capitec is looking to expand not only in offerings, but also to other shores.

In March this year, the bank got the green light from the South African Reserve Bank to increase its ownership of Cyprus-based AvaFin, an international consumer online lending group, from 40% to 97% at a price tag of around R530-million. Fourie says Avafin presents a strategic opportunity to diversify the bank’s income sources and build on its experience in foreign markets. DM

Monday, 25 March 2024

Cash-flush private education group AdvTech hikes dividend by 45%

Private education provider AdvTech’s CEO, Roy Douglas, enters retirement on a high note, helping the market leader achieve double-digit revenue growth and solid enrolments in both schools and tertiary divisions.

AdvTech has also hiked its dividend by 45%.

Since Douglas took over from interim CEO Frank Thompson in November 2015, the group has almost doubled its enrolments, from 47,209 to 93,728, at an annualised growth rate of 8%.

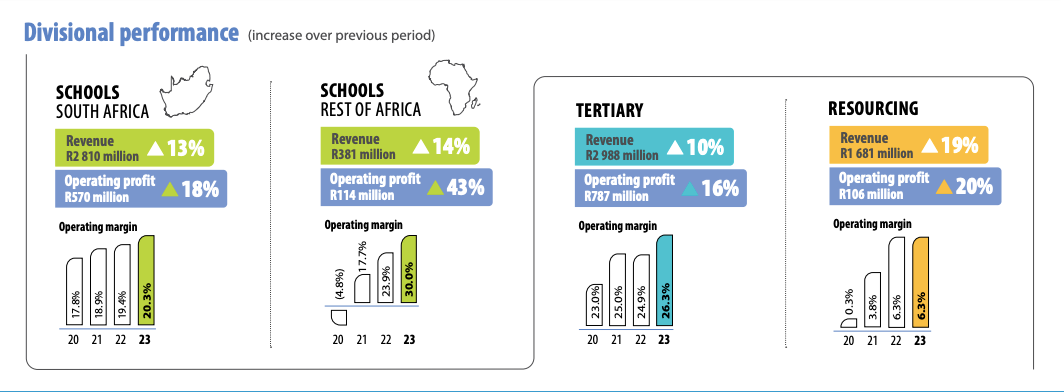

The latest financial year, ended 31 December 2023, saw AdvTech basking in strong demand for quality education, helping it grow revenue by 13% to R7.86-billion (up from R6.96-billion in 2022), and headline earnings per share by 19%.

Over the same period, operating profit increased by 18% to R1.57-billion (2022: R1.33-billion) and the operating margin improved to 20.1% (up from 19.1%).

AdvTech’s tertiary division — which includes Varsity College, Rosebank College, Vega and Capsicum Culinary Studio — has done exceptionally well for the group, with revenue up by 10% and operating profit increasing by 16% to R787-million.

Schools in South Africa (Trinity House, Crawford, Evolve online school and Junior Colleges) continue to do well, seeing 13% growth in revenue to R2.8-billion, while the rest of Africa (Kenya and Botswana) had boosted revenue by 14% to R381-million and hiked operating profit by 43% to R114-million.

It saw a marked improvement in collections during the year and the more favourable ageing of the debtors’ book, with the loss allowance reduced from R438-million to R405-million.

The group is cash-flush too: it says cash generated by operating activities was up 10% to R1.94-billion, which helped fund R669-million in capital expenditure and pay R189-million in finance costs, R415-million in dividends and R375-million in tax; repay R78-million in lease liabilities and settle debt of R190-million.

In a statement, board chairman Chris Boulle said Douglas successfully led the group in its expansion strategy during his tenure.

“He has refocused the educational division brand portfolios into well-positioned brands with distinct value offerings. This, together with a focus on effectiveness and efficiencies, resulted in a solid competitive advantage, and an agile and adaptive business model.”

Boulle praised Douglas’ leadership during the pandemic for being responsive to a dynamic environment, where more than 70,000 students were seamlessly transitioned to an online environment.

“He leaves AdvTech in a strong position to continue its growth trajectory.”

Douglas has an MBA and a degree in economics and has previously worked at Unilever, Nampak, Deloitte and House of Fraser (in the UK). He told Daily Maverick that while Covid was a stressful period, they look back at it now with a “great deal of fondness” because it helped the group stress-test the business.

“We had made several changes to structures and systems processes within the organisation school division in particular. We were able to leverage the technical expertise, knowledge and experience that we had in the group in terms of online education in a matter of three weeks. We never dropped a single academic day during that period.”

Geoff Whyte, another economist, replaces Douglas as group CEO.

Whyte is described as a commercially focused business leader with more than 30 years of experience across various industries, including Nando’s, Unilever, PepsiCo, Cadbury Schweppes and SABMiller.

Douglas said AdvTech had great growth in revenues, margins and operating profits, which enabled them to fund expansion programmes, acquisitions and developments.

Due to strong cash generation, the board has seen the opportunity to significantly enhance the dividend this year.

“It’s been a wonderful 10 years and I look back with great fondness.” DM

Monday, 18 March 2024

Sun International rides the gaming and tourism wave

Sun International has reported a strong set of results, with earnings from gaming up 78% and exceptional growth in some of its resorts and hotels, buoyed by leisure, conferencing and sports tourism.

SunBets is up by almost 80% year on year, while resorts and hotels have been reinvigorated by a surge in leisure, sports and business.

International leisure travellers have also driven up demand for the group’s Cape Town hotels. Tourism has made a notable recovery, as reflected in Stats SA’s latest tourism and migration data, showing that 20.1% (195,423) of all South Africa’s visitors in December were from abroad.

Sun International has cashed in handsomely on this segment, with revenue from rooms, food and beverages growing by 24.1% year on year.

The group’s income is up 7% to R12.1-billion, driven by record income from SunBet, which has generated 116.2% more income for the year, exceeding its five-year targets, and what it describes as “impressive” performance from its resorts and hotels.

Sun’s resorts and hotels were up 17.4% to R3-billion on 2022, driven by its top three performers: Sun City (up 14.8%), The Maslow (up 24%) and stellar performer The Table Bay Hotel (up 54.6%).

Gaming income, which brings in 76.8% of total group income, was 3.3% stronger year on year — despite the economic climate, increased competition and rolling blackouts.

Sun International chief executive Anthony Leeming said Sun’s gaming division has seen phenomenal growth in income and profitability.

“Sun City has seen record Ebitda [operating performance] — the highest it has ever made — and SunBet has had record Ebitda and profitability, rising from R733-million to R221-million in a year.”

SunBet also saw substantial growth in its key performance indicators, including almost 270% more unique active players, 268% more first-time depositors and 162.5% more deposits.

The Table Bay has delivered a phenomenal performance, largely due to foreign tourism, while at Sun City “everything’s up”.

“If you look at the restaurants across the group — our food and beverage income from concessionaires is doing incredibly well, with double-digit growth in the urban casinos as well.”

However, urban casinos were still under strain, he said, which reflects the general economy, uncertainty around the upcoming elections, crime, pressure on disposable income, the energy crisis and high interest rates.

Echoing the sentiments of other business leaders, Leeming said they need the general economy to grow so that their urban casinos can grow.

“We have to push really hard. We still expect strong growth, but everything is under pressure.” DM

Thursday, 14 March 2024

Distressed consumers fatten up Standard Bank’s bottom line

Standard Bank’s headline earnings leapt 27% to R42.9-billion for the 12 months to the end of December 2023 with a return on equity of 18.8%.

However, markets did not react favourably, with the share price falling about R13 intraday to close at R186.92 on Thursday.

Net asset value grew by 8% and the bank declared a final dividend of 733 cents per share, which, when combined with the interim dividend, equates to a dividend payout ratio of 55%.

Standard Bank Group chief executive Sim Tshabalala attributed the financial success to differentiated franchises with key performances from Africa Regions and offshore franchises.

On a more sombre note, the effect of the increasing interest rate environment over the past year has never been more evident.

Credit impairment charges increased 22% to R16.3-billion.

The increase in charges was driven by new loan origination, client strain driving partial payments, negative sovereign risk migration and new defaults.

In South Africa, credit impairment charges increased across all portfolios, compounded by the non-recurrence of credit recoveries on the payment holiday portfolio in the 2022 financial year (R500-million).

In Africa Regions, balance sheet growth, client-specific provisions and risk migrations led to higher credit charges.

The group’s credit loss ratio increased from 83 basis points in the 2022 financial year to 98 basis points in the past year, at the top of the group’s through-the-cycle credit loss ratio target range of 70 to 100 basis points.

The bank notes that clients are likely to remain constrained until interest rates decline.

Credit impairment charges are expected to peak in the first six months of 2024, driven primarily by ongoing strain in personal and private banking.

Looking ahead, the credit loss ratio is expected to remain within but near the top of the group’s through-the-cycle credit loss ratio range of 70 to 100 basis points for the 2024 financial year.

Operating expenses increased by 15% to R79.7-billion, impacted by inflationary pressures, particularly in Africa Regions.

Standard Bank is investing in human resources with a 17% increase in staff costs driven by a larger staff complement, annual increases and higher performance-linked incentives. DM

Monday, 11 March 2024

Absa crosses the R100bn revenue threshold, sinks money into IT and new staff

Absa’s financial results for 2023 showcase a mixed bag of gains and pains, with a tidy sum of R126-million from insurance for riot-damaged property.

Absa’s financial statements for the year to the end of December 2023 received an injection of R126-million from insurance proceeds for damage sustained to property and equipment as a result of the KZN riots of 2021.

The banking group crossed the R100-billion revenue threshold for the first time as revenue grew 8% to R104.5-billion, with stronger growth coming from African regions.

“We are seeing the benefits of the strategic choices we made in 2018, as is evident from our diversified business, growing customer franchise and engaged workforce,” says Arrie Rautenbach, Absa group chief executive officer.

The bank’s customer base expanded 4% to 12.2 million in 2023 from 11.7 million a year earlier, but in the face of rising inflation and interest rates, credit impairment charges climbed 13% to R15.5-billion. South Africa’s prime rate of 11.75% at 31 December 2023 was 125 basis points higher than at 31 December 2022 and 475bps above the bottom of the rate cycle from mid-2020 to late 2021.

The credit loss ratio increased from 96bps to 118bps, exceeding Absa’s through-the-cycle target range of 75 to 100bps. Non-performing loans increased to 6.05% of total gross loans and advances as a result of elevated inflows into later-stage delinquencies in the South African retail portfolios.

Non-performing loans grew by a whopping 20% to R80-billion from R67-billion the year before.

In addition to its investment in a BBBEE transaction which placed 7% of group shareholding (equivalent to R11.2-billion at the time) in the hands of employees and communities, Absa has invested significantly in the recruitment of additional frontline staff. Recruitment, together with spend on digital, contributed to a 10% increase in operating expenses. Absa expanded its employee base and, at the same time, invested more in new digital capabilities to enhance customer experience both in branches and online. The number of digitally active customers increased from 3.4 million to 3.8 million.

Chris Snyman, Absa group interim financial director, says the bank has strengthened its balance sheet, with a 7% compound growth in revenues since 2018, while the cost-to-income ratio has improved to 52% from 58% in 2018. DM

Tuesday, 5 March 2024

Sibanye swings into loss on PGM price meltdown, $2.6bn in impairments

The sharp downturn in platinum group metals (PGMs) prices has hit producers hard, with Sibanye-Stillwater taking a $2.6-billion knock in asset impairments. It all adds up to a loss of $2-billion for the 2023 financial year versus a $1.2-billion profit for 2022.

Diversified metals producer Sibanye released jarring results on Tuesday which showed it had fallen deep into the red in 2022 as the PGM price meltdown chowed its earnings and mangled the value of assets.

It’s a dramatic shift from a couple of years ago when PGM producers were reaping record profits from record prices.

The company’s rivals, including Northam Platinum and Impala Platinum, have also posted sharply lower earnings, but have managed to stay in the black.

Sibanye bit the impairment bullet and shut off the dividend taps as it hunkered down for a turnaround in the PGM market, which has been hit by a perfect storm of global economic anxiety, premature obituaries of the internal combustion engine and an unexpected decline in rhodium demand from Chinese makers of fibreglass.

“The Group’s financial results for the year ended 31 December 2023 were similarly impacted by the sudden and sharp decline in PGM and nickel prices,” the company said.

“The 33% year-on-year decline in the average PGM basket prices, in particular, resulted in a dramatic fall in the profitability of the US and SA PGM operations, which in recent years have contributed the bulk of Group earnings and cash flow.

“The significant decline in metal prices and uncertain outlook, along with specific operational performance factors, also resulted in the Group having to recognise impairments of R47.5-billion ($2.6-billion) against various assets, which was a primary driver of the Group reporting a loss for 2023 of R37.4-billion ($2-billion) compared with a R19-billion ($1.2-billion) profit for 2022.”

The impairments were applied to the US PGM underground operation, SA Gold’s Kloof operation, the Burnstone gold project in South Africa and the Sandouville nickel refinery in France. These are non-cash items and an accounting write-down of the value of the assets.

But only #4 shaft at the SA Gold’s Kloof operation is closing down as it is nearing the end of its life.

The US PGM operation, known as Stillwater, has already returned plenty of cash to shareholders and will do so again if and when the market rebounds from its current nosedive.

“Stillwater has paid for itself and shareholders have benefitted from dividends generated from the operation,” Sibanye CEO Neal Froneman told Daily Maverick in an interview.

Indeed, a couple of years ago, Stillwater, located in the US state of Montana, accounted for half of the group’s Ebitda (earnings before interest, taxes, depreciation and amortisation).

Sibanye maintains that the fundamentals of the PGM market point to an eventual rebound.

“We continue to see emerging signals that … support our long-held, robust view on PGM demand,” the company.

These include forecast production growth for the rest of this decade in light-duty vehicles – or cars, simply put – powered by internal combustion engines that require platinum, palladium and rhodium for emissions-capping catalytic converters.

Alongside this is a moderation in growth rates for battery electric vehicles which require other metals. Primary supply is also falling in the face of low prices.

Sibanye has warned before of looming layoffs in South Africa’s PGM sector, but the company did not announce any new planned retrenchments, known as “Section 189” notices.

However, Froneman told Daily Maverick that he wouldn’t “rule any out” in the future. DM

Tuesday, 5 March 2024

Shoprite outruns competitors with 14.6% hike in interim sales

South Africa’s biggest and most successful retailer isn’t focusing on what is going wrong. Instead, it’s honing in on what it is doing right.

While its biggest competitor appears to have lost the plot, Shoprite just keeps on winning. South Africa’s biggest and most successful retailer has sold 13.9% more merchandise and gained R4-billion in market share in the past six months – and it expects an even brighter future.

Over the past six months, the group made R121-billion in sales.

On Tuesday, the retailer released its unaudited results for the period ended 31 December 2023.

After almost five years of uninterrupted market share gains, Shoprite is dishing up some stiff competition for Woolworths and Spar and is clearly eating Pick n Pay’s lunch.

Last month, Pick n Pay — which posted its historically worst results in October 2023 — announced it would be listing its prized asset, Boxer, in order to pay off debt.

South Africa’s former darling retailer has also attracted the wrong attention after reports that it planned to liquidate one of its biggest franchisees, owned by the Baladakis family.

Back to Shoprite, where the focus is not so much on where competitors have gone wrong, but on what it has done right.

Shoprite CEO Pieter Engelbrecht kicked off his presentation with an apparent dig at Pick n Pay – which has repeatedly bemoaned the difficulty of doing business in South Africa – saying he could “spend an hour on all the excuses of why things are not great or why the performance could be better or what the reasons are that makes doing business in South Africa extremely challenging, but we’re not going to do that. It’s not what we do.”

Rather, Engelbrecht said, they would focus on how well they did, how the company developed, its increased employment, leadership, and the fun it had with its advertising.

“I’m very happy to say that we have managed to win 34 awards for innovation in retail in the last six months.”

In South Africa, the group’s supermarket sales hit R97.5-billion over the period – a 14.6% increase on the previous six months.

Checkers and Checkers Hyper saw a 13.7% increase in sales, while Shoprite and Usave increased sales by 13.2% and 12.3%, respectively, which Engelbrecht attributed to the focus on putting the customer’s challenges and needs front and centre in the business, a commitment to the lowest prices, in-stock availability, efficient operations, and ongoing product and store development.

Shoprite also increased its foothold in the country, opening 369 new stores over the past year.

Checkers Sixty60, which is on a massive winning streak, hiked its sales by 63.1% over the past six months.

Engelbrecht said while the operating context in South Africa was challenging and costly, especially due to the cost of blackouts, they were pleased to report an increase in profits and dividends for the period.

“The group continues to invest in the business on a number of fronts: tech and digital, supply chain, stores and, of course, people.

“Over the six months, we added a net of 197 new stores to total 3,543 stores and, as a group, our commitment to employment growth resulted in the creation of 2,617 new jobs.”

The board has declared an interim dividend of 267c per ordinary share, which shareholders can expect on 2 April 2024. DM

Monday, 4 March 2024

Aspen expels pig intestines and moves on to greener pastures

Multinational pharmaceutical manufacturer Aspen Pharmacare is poised for strong organic growth after switching manufacturing agreements for the supply of heparin-based syringes to a toll contract manufacturing arrangement.

The move will effectively reduce Aspen’s investment in heparin inventory, and increase operating cash flows in the current financial year and the next.

In the six months to the end of December 2023, Aspen’s investment in heparin inventory was reduced by R1-billion, with a further R2-billion reduction anticipated by the end of June this year.

The active ingredient for Heparin, a blood-thinning drug, is sourced from pig intestines. An outbreak of swine flu and African swine fever in recent years raised concerns globally, prompting a major recall of the injectable anticoagulant by the US Food and Drug Administration and their counterparts in Europe, Australia and New Zealand.

Aspen has countered this weakness in its supply chain with the transition to a toll manufacturing agreement, which means the company’s customers will own and source the active ingredient while Aspen will handle the manufacturing contract.

“It effectively takes away the drag on our bottom line and makes it a working capital-light model,” says Sean Capazorio, group finance officer.

The other big move Aspen made in the first half of the year was the conclusion of a Sandoz agreement, which included acquiring the Sandoz business in China for a net upfront consideration of €27.9-million followed by potential net milestone payments of €9.2-million.

Management expects to get competition authority approval for the deal in May.

Capazorio says the deal will materially mitigate the negative impact of volume-based procurement on Aspen’s existing business in China from next year.

Stephen Saad, Aspen’s group chief executive, says the company has completed the necessary steps to reach the commercialisation stage for the manufacture of mRNA platform products which will augment revenue in the second half of the year.

Revenue climbed 10% to R21.1-billion while operating cash flow per share jumped 44% to 553.2 cents.

The second half of the year will be further boosted by the distribution and promotion agreement with Lilly for sub-Saharan Africa, and the product purchase agreement with Viatris for Latin America.

The agreement with Lilly is effective from January 2024.

Subsequent years will benefit from the launch of key pipeline products including Lilly’s Tirzepatide, marketed globally as Mounjaro.

Viagra, Lipitor, Norvasc, Lyrica and Celebrex are key brands included in the product portfolio acquired for Latin America.

Aspen’s share price has climbed 16.55% over the last year to close at R205.21 on Monday afternoon. DM

Thursday, 29 February 2024

FNB takes a hit of almost R1bn as clients benefit from fee reductions

First National Bank (FNB) will absorb a hit of almost R1-billion in the current financial year on the back of fee reductions, says FirstRand Group chief executive Alan Pullinger.

“Bank fee increases were below inflation across the board in July 2023 and in addition to that, we reduced fees on instant payments,” Pullinger says.

The relatively muted growth in FNB’s fee and commission income for the six months to the end of December was due to sub-inflation fee increases across both retail and commercial accounts.

In addition, with the introduction of PayShap, FNB reviewed its pricing structures for low-value, real-time payments and decided to reduce all related fees and absorb the entire impact of the repricing in one financial year (to 30 June 2024).

“The resultant 30% increase in real-time payment volumes that FNB has already experienced since the repricing action demonstrates this is the correct outcome for customers.

“In the first six months of the current year alone, this resulted in a cumulative R477-million reduction in customer fees,” he says.

Advances growth from FNB’s commercial segment were up 10%, compared with a 14% increase at RMB and a 9% increase at FNB Broader Africa.

The bank says these numbers reflect a consistent origination strategy to focus on sectors showing above-cycle growth, and which are expected to perform well even in an inflationary and high interest rate environment.

Normalised earnings increased 6% to R19.1-billion, driven by strong topline growth, particularly net interest income, which was supported by growth in both advances and deposits.

Advances now total R1.6-trillion.

Pullinger says the credit loss ratio of 0.83% is particularly pleasing since it is well below the midpoint of the group’s through-the-cycle range of 80bps to 110bps.

“This is a commendable result given the prevailing inflation and interest rate cycle and has enabled continued advances growth as the group services the needs of customers through judicious and tactical origination,” he noted.

Across the portfolio, deposits and transactional balances increased strongly, both of which have provided an underpin to the return profile. The retail and commercial segments of FNB in particular registered excellent growth in deposits off an already high base.

This performance reflects the benefit of the group’s approach to origination, particularly post the pandemic when new business was weighted towards the low- and medium-risk categories, and was achieved despite the current pressures from high inflation and interest rates.

Total group operating expenses were 9% higher and in line with expectations.

FNB grew costs below inflation, but this was offset by a significant increase in costs from RMB (+13%) due to elevated investment in platform and geographic expansion.

The UK operations’ ongoing investment in systems and people contributed to cost growth of 11%. Overall, the cost-to-income ratio decreased to 49.9%, given the strong topline growth in the period.

Commenting on second-half prospects, Pullinger said the group expects the macroeconomic environment in the jurisdictions where it operates to remain largely unchanged, characterised by high interest rates and persistent elevated inflation.

“Given this backdrop, we anticipate softer overall advances growth and, given the current high base, deposit growth will slow as households draw down on savings, although commercial deposit gathering is expected to remain resilient,” he said.

Pullinger concluded by indicating that the group expects to generate earnings in the second half similar to the first.

Shareholders will receive an interim dividend of 200 cents per share, representing a payout of 59%. DM

Wednesday, 28 February 2024

Woolworths shows food basket brims with potential

Woolies Food delivered solid growth, with turnover and concession sales growing by 8.4% and 7.2% on a comparable store basis, despite the impact of rolling blackouts, bird flu and the taxi strike.

Subdued spending on discretionary items — particularly apparel — dragged down Woolworths’ half-year profits. And the weak economy is not helping.

In South Africa, Woolworths’ operations were also hamstrung by load shedding, congestion at the ports and the impact of bird flu. It’s not likely to get easier over the rest of the financial year, with the upcoming elections and growing geopolitical uncertainty.

The retailer released its interim results on Wednesday, for the 26 weeks ended 24 December 2023, but said the first half of the 2024 financial year was not directly comparable to that of the prior period because of the inclusion of the David Jones contribution in the 2023 period.

Nobody is immune from the challenging macroeconomic environment, which loomed large in the results, owing to the cost of living crisis and interest rate increases. The retailer said this affected footfall and resulted in a bigger-than-expected pullback in discretionary spending.

Consumers are still spending on food, though.

Once again, Woolworths Food delivered solid growth, with turnover and concession sales growing by 8.4% and 7.2% on a comparable store basis, despite the impact of rolling blackouts, bird flu and the taxi strike.

In the last six months of the period — the height of the festive season spending — sales grew by 8.6%. Online sales through the Dash app were up by 46.6%, although that only comprised 5.1% of South African sales.

Its gross profit margin increased to 24.6%, which it attributed to targeted and effective promotions and value chain efficiencies.

Adjusted operating profit grew by 13% to R1.6-billion. Adjusted for the impact of the blackouts, operating profit grew by 13.2%.

Fashion, Beauty and Home (FBH) was making steady progress.

Woolworths CEO Roy Bagattini said the standout performer was its food business, but FBH — in particular Beauty — was up 16%.

“We’ve doubled our Beauty business in the last three years and our plan is to double it again in the next two to three years. We’re investing heavily in Beauty… It’s a big play for us.

“If you want to establish yourself as a beauty destination, you really have to have the scope of offering different categories and you need to have the right products and experiences. We now have 20% of the beauty market in South Africa.”

Sales for the period under review were affected in part by the late arrival of some summer ranges owing to the ports crisis. Turnover and concession sales grew by 2.2%, with store sales increasing by 1.5%.

The group’s turnover and concession sales from continuing operations were up by 5.4%.

The final six weeks of the period, which included festive season trade, was up by 7.2%.

The apparel business — which is struggling in Australia — saw a 7.4% decline in earnings per share (EPS) from continuing operations, while headline EPS declined by 7.5% and 31% across the group.

The economic environment in South Africa was and remained challenging, exacerbated by the energy and logistics crises which hurt business and consumer confidence.

However, despite the difficulties, its combined southern Africa business grew operating profit by 10% on last year.

Woolworths Financial Services (WFS) showed a 4.9% increase in new accounts and credit card advances. The annualised impairment rate for the period was up slightly to 6.3%, from 5.5% in the prior period.

Bagattini said WFS was a “very interesting business”.

“Obviously, it is very much subject to the economic cycle. We’ve seen a significant return to profitability and performance of that business. We’re also growing our book.

“But if you look at the impairment ratio, we have the lowest level of impairment, given our approach to credit and given the relative target market of our other financial offerings. It is the healthiest book in this sector.”

In Australasia, trading conditions have worsened: consumer sentiment in Australia is at near-record lows and household savings are the weakest since the global financial crisis.

Woolworths noted in a statement that there was a marked shift from spending on goods to services.

Country Road’s sales were down by 5% and 9.5% in comparable stores, although it said the brand was delivering a market-leading performance across key categories.

“Overall trading space increased by 6.6% during the period, supported by the ongoing expansion of our wholesale and concession channels. The contribution from online sales increased marginally to 26.8% of total sales.”

The rest of the financial year was likely to remain difficult, with rising inflation and high interest rates putting pressure on consumers the world over – but South Africa also had the energy, ports and other crises to contend with, alongside the upcoming elections and ongoing global geopolitical tensions. DM

Wednesday, 31 January 2024

Astral Foods reports its first loss in 23 years

If 2023 was a disastrous year for Astral Foods, the chicken producer seems to be more hopeful for the future. After last year’s intensive rolling blackouts, water supply issues, record high input costs and a crushing outbreak of the highly pathogenic avian influenza (HPAI), Astral reported its first loss in its 23-year history.

On Wednesday, it was more optimistic, saying that it was expecting to return to profitability in the first quarter of the financial year ending 30 September 2024, after making good headway in addressing some of its recent issues, including maintaining emergency backup generator capacity at all its operations; benefitting from lower stages of rolling blackouts, which helped keep a lid on diesel costs; putting uninterrupted water supply systems in place to reduce downtime; keeping feeding costs low; and normalising the poultry sales mix, which was previously affected by heavy promotional discounting.

Despite reduced levels of blackouts, Astral was still forced to run its Standerton poultry processing plant on diesel because of municipal power supply interruptions.

It also said it had managed to avoid a shortage of chicken during the outbreak of HPAI, which increased costs as it had to import broiler hatching eggs.

Owing to what it called “depressed consumer spending”, Astral said it had aligned broiler slaughter numbers to adapt to the current market conditions, and was committed to recovering its input costs.

Of the International Trade Administration Commission’s (Itac’s) announcement on poultry sector rebates, which was in response to HPAI-related shortages, Astral said it was dismayed at Itac’s recommended poultry import tariff rebate structure.

“No shortage of chicken has been experienced or expected in the local supply chain with industry production at normalised levels due to numerous contingency plans implemented.”

After last year’s disastrous results, Astral now says it expects that earnings per share and headline earnings per share for the six months ending 31 March 2024 could increase by “at least 300%” to 647c and 654c, respectively.

Importers, however, hailed Itac’s announcement.

Hume International’s logistics and operations director Roy Thomas said consumers had reason to celebrate, as Itac confirmed that it was lifting punitive tariffs on imported chicken.

“This decision was made in response to the impacts of [HPAI] … which has ravaged both global and local poultry supplies. Heeding calls and warnings from importers and businesses such as Hume International regarding the serious consequences of the outbreak on the cost of chicken, Itac’s tariff rebate represents a welcome reprieve for consumers – especially low-income households.”

Thomas said despite claims that bird flu had little impact on supplies or prices on shelves last year, Statistics South Africa’s latest inflation figures showed that egg prices surged by 38%, chicken giblets by 18.3%, fresh chicken portions by 14.6%, whole chicken by 8.4% and individual quick frozen portions by 6.4% — all above average inflation for 2023.

“These price increases clearly reflect the ongoing impacts of bird flu both locally and abroad, in addition to the effect of new import tariffs implemented in August last year.” DM

Tuesday, 30 January 2024

Checkers Sixty60 delivers a competitive edge for Shoprite

Reliable, convenient and quick home deliveries have given South Africa’s largest retail group, Shoprite, the upper hand, boosting sales through its Checkers Sixty60 delivery platform by 63.1% over the past six months.

The group ended the second half of 2023 on a high, with sales up by almost 14% to R121.1-billion, helped along by a record Black Friday and festive season trade.

In an update on Tuesday, Shoprite said its Shoprite and Checkers Xtra Savings rewards programme had also saved customers R8.4-billion over the period.

The group’s core business in South Africa enjoyed a healthy 14.6% jump in sales.

Internal selling price inflation for the period was 7.7%. Checkers and Checkers Hyper grew sales by 13.7%, Shoprite and Usave were up by 13.1% and liquor sales, through LiquorShop, were up by 25.2%.

The group said its robust sales were favourably boosted by its acquisition of 94 stores from the Massmart group, which added 51 Shoprite, one Usave and 42 Shoprite LiquorShops to its stable.

Over the past 12 months, the group grew by 285 stores, bringing its total number of stores to 2,237.

Outside South Africa, where Shoprite has outlets in Ghana, Angola, Mozambique and Zambia, sales were up 20%, increasing in rand value by 6.2%. It has added nine more stores in nine countries over the past year, bringing that total to 258.

Reflecting the impact of the cost-of-living crisis on consumers’ pockets, furniture sales were in the doldrums: OK Furniture and House & Home increased sales by just 1.7%.

Consumers are increasingly cash-strapped, spending less on discretionary items like clothes and appliances while channeling their money towards the necessities of life.

The group’s other operating segments, comprising OK Franchise, Transpharm, Medirite Pharmacies, Red Star Wholesale Catering Services (previously Checkers Food Services) and Computicket, reported sales growth of 23.1%.

The OK Franchise division was up by 25%, increasing its store base by 70 stores over the year. A total of 605 stores are now franchises.

Diesel, to power generators due to increased rolling blackouts, cost Shoprite half a billion rand over the period. DM

Monday, 29 January 2024

Truworths owes buoyant sales to Office stores

Clothing retailer Truworths owes most of its healthy recent sales to shoe sales at the group’s UK-based Office stores, which saw a double-digit increase — in pounds — over the past six months.

Store account sales have been flat since 2022, comprising 70% of all retail sales, while 0.9% fewer customers were paying for their goods in cash.

The retail group released a trading update today, for the period from 3 July 2023 to 31 December 2023, which showed an 8.2% increase in retail sales to R12.2-billion compared with the previous financial period from 4 July 2022 to 1 January 2023.

Sales at Office grew by 15.6% to £162-million relative to the prior period’s £140-million, which in rand terms saw growth of 33.1% to R3.8-billion.

It said Office was benefiting from its “unique market positioning, brand partnerships and strong online presence”. Online sales comprised 47% of Office’s retail sales in the current period, growing by 3% in the prior period. The last nine weeks of 2023 saw an 11.7% increase in retail sales to £71-million. Office is expected to grow by 12% for the 2024 financial period, due to greater investment in stores and renovations.

Truworths Africa was down by 0.3%. Poor economic conditions and high interest rates ate into consumers’ disposable income, which affected sales. The group granted less credit due to consumers’ declining credit health, which also hurt sales. Retail sales were down 1.6% to R4-billion for the last nine weeks of the year. Online sales, though, were robust, increasing by 41% and contributing 4.2% to Truworths Africa’s retail sales.

Once again, a retailer blames port congestion for weaker-than-expected sales, which resulted in reduced deliveries ahead of the Christmas season.

Last week, Mr Price said the Durban port congestion disrupted festive season trade, as it kept an eye on the instability of the Red Sea shipping route which has increased time on the water. This also increased shipping costs, although Mr Price said its rates were contracted until June.

TFG said economic conditions in all its operating territories remained challenging.

In its update on 24 January, TFG said: “In South Africa, this was exacerbated by continued load shedding and delays experienced at ports, which impeded the planned flow of inventory. The impact of these import delays was offset to an extent by the ability to increase volumes from TFG’s local manufacturing capacity.”

Woolworths, too, said in its half-year results that the energy crisis — compounded by the fiasco at South Africa’s ports, the cost-of-living crisis and bird flu — had weighed down sales. DM

Wednesday, 24 January 2024

TFG reports healthy growth in turnover

TFG’s latest results show e-commerce is booming. Bash, its online sales platform, grew by almost 45% over the nine months leading up to 30 December, contributing 4.2% towards the group’s Africa business.

The group also saw a 9% growth in turnover, largely owing to robust festive season trading and growth in its Africa division.

In a trading update released on Wednesday, the group, which owns the Foschini, @Home, American Swiss, Coricraft and 30 other brands, said it also grew turnover in the last three months of 2023 by 4.5%.

Turnover was healthier closer to home than in the UK and Australia: TFG Africa grew turnover by 5.1% in Q3 and for the month of December, by almost 12%. TFG Africa’s cash turnover — which grew by 6.6% in Q3 FY2024 — now comprises 75.8% of the division’s Africa turnover and 82.4% of group turnover.

Once again, a retailer has bemoaned rolling blackouts: On Tuesday, Woolworths noted in its half-year results that the energy crisis — compounded by the fiasco at South Africa’s ports, the cost-of-living crisis and bird flu — had weighed down sales.

TFG says turnover has been affected by a softer Black Friday period in South Africa, with Stage 6 load shedding implemented over that weekend.

Its London operations saw a 3% decline in turnover, after the strong bounceback after Covid-19 recovery base in Q3 of 2022, while TFG Australia was down by 7.3% in Australian dollars.

Bash, the group’s online shopping platform, grew turnover by 29.2% in Q3 FY2024.

TFG Africa’s online turnover was also up, by 44.8% in Q3.

Credit turnover was minuscule, up by just 0.7% in Q3, as the group kept a beady eye on the economic climate and accepted only 17.8% of new accounts.

In a Sens announcement, TFG said economic conditions in all its operating territories remain challenging.

“In South Africa, this was exacerbated by continued load shedding and delays experienced at ports, which impeded the planned flow of inventory. The impact of these import delays was offset to an extent by the ability to increase volumes from TFG’s local manufacturing capacity.”

Both TFG London and TFG Australia’s performances were to be viewed in the context of exceptional performance after Covid recovery, the group said, adding that consumers were under pressure from the cost-of-living crisis.

TFG said trading conditions and consumer confidence were likely to remain under pressure, due to inflation and interest rates, and South Africa’s energy crisis and port chaos. DM

Tuesday, 23 January 2024

Woolies counts on food as other divisions hit by ports, energy, bird flu and economic crises

Congestion at the ports, bird flu and the energy crisis are all weighing heavily on Woolworths’ sales in South Africa, which have also been dragged down in both its home market as well as Australia by the cost-of-living crisis.

The food, apparel and homeware retailer released its half-year results on Tuesday for the year ended 24 December 2023, which reveal strong growth from its robust food business in light of a difficult economic environment.

Building on the 15 November 2023 update it released on Sens, it said its performance for the current period has been shaped by an increasingly difficult macroeconomic backdrop due to the sustained effect of interest rate increases and higher living costs.

This was evident in reduced footfall and a greater-than-expected pullback in discretionary spending in both SA and Australia.

South African operations were further bruised by higher levels of rolling blackouts, congestion at the ports and the impact of the bird flu outbreak that was affecting key food product lines.

Woolworths said the economic environment in South Africa “remains challenging, exacerbated by the country’s energy and logistics crises, which continue to impact both business and consumer confidence”.

Despite bird flu, the energy crisis and the port snarl-ups, the food business delivered solid growth, with sales up by 8.4%.

Online sales, via Woolworths Dash, rose by 46.6% and contributed 5.1% towards South African sales.

But the fashion, beauty and home business — reliant on imports — suffered over this period, with turnover and concession sales up by just 2.2%, during what should have seen peak sales.

Black Friday and the festive season helped boost sales in the last six weeks of the period under review by 3.8%.

More customers were signing up for credit, as Woolworths Financial Services saw a year-on-year increase of 4.9% to the end of December 2023, as customers opened new accounts and credit cards.

Impairments were up by 6.3%, compared with 5.5% in the prior period, suggesting customers were under increased strain.

Country Road was battling in Australia and New Zealand, as trading conditions worsened in both countries: sales were down by 5% and 9.5% in comparable stores, although it said this should be viewed off a high base in the prior period, which saw sales growth of 25.5% after the strong recovery from the Covid lockdowns. DM

Wednesday, 29 November 2023

Naspers doubles profits, says profitability in e-commerce is within reach

Naspers has released its interim results alongside its Amsterdam investment arm, Prosus.

Naspers has doubled profits over the past six months. The multinational internet and tech group released its interim results on Wednesday for the half-year ending 30 September, alongside those of its Amsterdam-based investment arm, Prosus.

September marked the fourth anniversary of listing Prosus on the Euronext Amsterdam, which created Europe’s largest consumer internet company.

Naspers and Prosus announced in June that they would unwind their convoluted relationship, which undermined shareholder value.

Introduced two years ago, Prosus owned nearly half of its South African parent (49.5%), while the latter owned 61% of Prosus, in the cross-holding arrangement. The South African Reserve Bank approved a buy-back scheme that allowed Naspers to buy back more of its shares and work to undo the cross-holding, the companies announced in June.

The group said it had made significant progress on its commitments to steer Prosus’s e-commerce to profitability by the first half of 2025 – it is now targeting profitability for the second half of 2024 – and continue its open-ended share repurchase programme; simplify its structure through removing the cross-holding, and highlight the value in its portfolio of assets.

The ongoing open-ended share repurchase programme has reduced Naspers’s net share count by 14% and generated $25-billion for shareholders.

Naspers funds its share repurchase programme with regular sales of Prosus shares.

Ervin Tu, interim group CEO for both Prosus and Naspers, said in a company statement that they were making substantial progress towards driving profitable growth.

“Through active management of our portfolio, we have delivered improved results as our e-commerce portfolio is now close to break-even and growing at scale.

“We’ve simplified our group structure, and the open-ended buyback programme is driving daily NAV (net-asset value) per share growth, magnifying returns over the long term.

“With deep institutional knowledge across a number of technology domains, including AI, we are well positioned to support exceptional technology companies around the world.

“We remain ambitious in our plans and disciplined in our approach to drive real returns for all of our stakeholders,” said Tu.

Core headline earnings more than doubled, increasing by 112%, due to improved e-commerce and Tencent profitability.

Its free cash inflow increased to $677-million – an eightfold year-on-year improvement, and it has access to more than $15.1-billion in cash.

Takealot has sold more products and grown revenue by 15% and 9% respectively. Naspers attributed rising interest rates, inflation, depressed consumer demand and rolling blackouts for creating strain on the business.

The Takealot group has reduced its trading losses by 85% when measured in US dollars. Takealot.com grew its total sales by 15% and expanded its marketplace seller base, which reached about 10,600 sellers in September 2023.

Mr D, its food, grocery and convenience delivery service, grew revenue by 11% and sales by 15% in rand value.

It said Mr D’s partnership with Pick n Pay continues to grow.

Prosus held 25% of Tencent at the end of the reporting period.

E-commerce trading losses were sharply down, reducing from a peak of $270-million to $38-million in the period under review.

Consolidated group revenue from continuing operations increased by $248-million, or 9%, due primarily to strong revenue growth in classifieds, food delivery, and payments and fintech. DM

Monday, 27 November 2023

Oceana thanks its Lucky Star for jump in profits

Fishing and food processing company, Oceana has seen a 28.9% jump in net profit, thanks largely to its popular Lucky Star range of tinned fish and record performance from its international subsidiary, Daybrook Fisheries.

Daybrook produces fishmeal and fish oil, sold primarily to the US pet food and global animal and aquaculture markets.

Lucky Star has seen a surge in sales this year, in a constrained environment, as consumers switch to more affordable forms of protein. Oceana released its annual results on Monday for the year ended 30 September 2023, which revealed a 28.9% rise in headline earnings, to R980-million, largely driven by strong performances from Daybrook, which raised operating profit in dollar terms by 30%, and Lucky Star, which grew sales by 9%. Another element in Lucky Star’s favour: Rolling blackouts, because customers are increasingly drawn to shelf-stable products like tinned fish because they are a safe and convenient protein.

Local canning production volumes were up by 13.1% to 5.2 million cartons. Inventory levels were 18.7% higher than the previous year.

Revenue was up by 22.6% to R10-billion, supported by improved pricing across its products and the effect of the weaker rand on exports, while operating profit from continuing operations climbed by almost 20% to R1.5-billion – the highest level since 2016.

The group also reduced its debt levels to the lowest since it acquired Daybrook in 2015.

Despite positive price movements, the group said its gross margin reduced from 30.8% in 2023 to 28.6% this year, due to rising input costs, which were not passed on to consumers to maintain affordability, lower catch volumes and fish oil yields in both the SA and the US fishmeal and fish oil operations, poorer catch rates for its SA hake and horse mackerel fleets and costs related to rolling blackouts.

Its profit after tax increased by 25.2% to R990-million.

Oceana CEO Neville Brink said a diversification strategy across species, geographies, and currencies helped it to deliver strong growth despite the operating environment being characterised by high inflation and interest rates, currency volatility, a low-growth domestic economy and increased rolling blackouts.

“Diversification enabled us to benefit from higher demand and better hard-currency pricing for many of our products. Record global fish oil prices particularly helped Daybrook. By building and holding higher inventory levels we were able to capitalise on the demand. In the domestic market, investing in our volume strategy for Lucky Star by absorbing some inflationary input costs and protecting consumers has paid off, as reflected in our sales growth.”

Oceana’s new canned meat factory opened in October 2023. It plans to leverage the brand strength of Lucky Star to release other canned food categories in the new year.

Brink said Oceana would continue to grow Lucky Star sales by ensuring high levels of availability and keeping the product affordable relative to competing proteins.

“While we will remain responsive to the impact of rand weakness on Lucky Star margins, our high exposure to foreign-currency earnings provides a natural hedge against rand volatility.”

The shift in the weather cycle to the El Niño effect is expected to improve fishing conditions and catch rates of South African hake, horse mackerel and squid.

Oceana was recently allocated a 15-year fishing right. DM

Tuesday, 21 November 2023

African Bank swings from a loss to a profit intra-year on the back of acquisitions

African Bank’s net profits after tax swung from a loss of R44-million in the first half of the year to a profit of R549-million in the second half. However, this was partially due to a boost from the R1.5-billion acquisition of Grindrod Bank in 2022.

As part of its growth strategy, management has also been quite deliberate in diversifying, moving from what was largely a retail consumer-focused bank to a bank looking to strengthen its offerings through alliances that now bring business banking and insurance to the table.

“There was a very clear focus this year to integrate the Ubank businesses that we acquired, the Grindrod business and further organic growth beyond our comfort zone of consumer unsecured lending. The resultant derisking of the balance sheet positions us favourably for both scale and sustainability going forward,” says group chief executive officer, Kennedy Bungane, announcing the company’s annual results to the end of September 2023.

Despite a worrying jump in non-performing loans (NPL), which climbed to 42% from 37% last year, African Bank remains confident that it is firmly on the path to success

Management says the rising NPL number is due to several factors including:

- More selective disbursements in consumer banking resulting in a shrinking advances book, where NPLs comprise a bigger percentage of the total book.

- Refocused collections processes and workstreams have been implemented and are starting to bear fruit.

The bank revealed that it had grown active customer numbers to just under four million. However, more than half of this number comes from Alliance Banking or banking partnerships with MTN Momo, Shoprite Checkers and fintech company Lesaka.

Sibongiseni Ngundze, chief executive of consumer banking, says the bank saw a 52% growth in transaction volumes over the year, moving to 53 million transactions, largely at point-of-sale and ATMs.

These transactions added up to a hefty R58.6-billion in value. DM

Monday, 20 November 2023

Bird flu and rolling blackouts take R1.6-bn toll on Astral Foods

Six months after it announced that rolling blackouts had cost three-quarters of a billion rand in just half a year, South Africa’s second-biggest poultry producer, Astral Foods, has released its annual results, revealing that it had incurred a R1.6-billion loss over the past year.

This is Astral’s first loss in its 23-year history.

It also had to write off more than a million birds due to the bird flu outbreak, which cost it more than R400-million.

Revenue for the year ended 30 September 2023 was R19.3-billion, in line with that achieved in FY2022, but while revenue in its feed division was up slightly year-on-year, revenue in the poultry division – which adds 82% towards its total revenue – was down due to a 9.6% drop in sales.

The group has reported a full-year loss before interest and tax of R621-million (last year, it made R1.4-billion in profit), due to costs associated with rolling blackouts, the outbreak of avian influenza and poor market trading conditions.

It spent R398-million on emergency diesel generators and additional water cost a further R168-million. The group has a R1.74-billion overdraft.

Astral’s poultry division was further hit by increased expenses of R1.6-billion (rolling blackouts), R31-million (water supply interruptions) and R400-million due to bird flu.

Revenue was down 0.8% due to a decrease in broiler sales volumes and a “less than ideal” product mix, it said, because of a backlog in the slaughter programme caused by rolling blackouts. This resulted in heavier and older birds staying on the farm for longer.

Broiler slaughter numbers were down by 15.3%, sales volumes were down by 9.6% and frozen poultry stock levels were higher.

The feed division’s revenue was up by 11.9% to R11.6-billion, due to higher feed selling prices.

“Biological asset write-downs”, or costs associated with culling chickens due to bird flu, cost the group R400.5-million.

Local chicken producers have been ravaged by the bird flu outbreak. Quantum Foods, the country’s biggest chicken and egg producer, announced on 10 November that it had incurred a loss of R155.3-million, due to culling. DM

Netcare posts healthy results and sets ambitious climate targets

The hospital group saw revenue climb by 9.5% to R23.7bn, while higher activity levels saw normalised operating profit increase by 24% to R2.8bn.

Despite diesel generator costs catapulting by 235% year on year to R124-million, Netcare posted pleasing results for the year to the end of September, giving shareholders more than R1.1-billion in dividends and share buybacks.

The hospital group has ambitious climate targets, having set itself a goal of achieving 100% utilisation requirements from renewable sources, with zero waste to landfill and an additional 20% reduction of impact on water sources by 2030. It has already reduced energy intensity per bed by 39%, exceeding the initial 10-year target set in 2013, and has achieved cumulative operational savings and benefits of more than R1.5-billion to date, yielding an IRR of 40%.

Less than a month ago, Netcare concluded an agreement for a renewable energy supply arrangement with NOA Group Trading, a renewable energy trader. From the first quarter of 2026, up to 100% of six Netcare sites’ energy consumption — comprising about 11% of Netcare’s total energy consumption — will be supplied from renewable energy sources through a combination of wind and solar farms.

Outgoing chief executive Richard Friedland, who has agreed to stay on for another six months until his replacement is ready to take over the reins next year, noted that there were several headwinds in place.

“First, we have interest rates that are at a 14-year high. Then there is the catastrophic collapse of the grid, which still remains incredibly fragile and uncertain. We’ve seen some high inflationary changes coming through on the back of service delivery failures. All these factors make for an incredibly difficult macro-environment,” he said.

Despite this, the hospital group saw revenue climb by 9.5% to R23.7-billion, while higher activity levels saw normalised operating profit increase by 24% to R2.8-billion.

In line with the mental health crisis that has persisted since the Covid pandemic, Netcare’s Akeso clinics’ mental healthcare patient days increased by 12.7%. The newly opened Netcare Akeso Gqeberha facility, along with the 36-bed Netcare Akeso Richards Bay facility commissioned in May 2022, contributed to this growth.

The strong increase in mental healthcare activity resulted in occupancies improving to 72.7% in the 2023 financial year from 68.1% the previous year. The market reacted favourably, with Netcare’s share price moving up by 6% on Monday to close at R13.77. DM

Friday, 17 November 2023

Life Healthcare to shed Alliance Medical Group business, operating profits slide 12%

Life Healthcare will sell off its Alliance Medical Group diagnostic imaging business to iCON Infrastructure in a deal that is expected to net R10.8-billion.

While a pending R21-million deal spells good news for listed hospital group Life Healthcare, the market did not react favourably on Wednesday to its annual results for the year to end September, with the share price falling more than 6% intraday, and more than 8% over the past three months.

Although group revenue climbed 10% to R22.6-billion, operating profit slid 12% to R2.4-billion.

However, management hastened to reassure investors, pointing out that the group remains in a strong financial position, with net debt to Ebitda at 2.0x, compared with the 2.17x reported for the six months to 31 March 2023.

Southern Africa chief executive, Adam Pyle, said operations in the southern Africa region saw excellent volume growth, as the case mix continued to normalise.

“We concluded two significant funder network deals, which contributed to increased activities and occupancies. We rolled out our renal integrated care product across our renal dialysis business and we made good progress in expanding our imaging and nuclear medicine businesses in southern Africa” he says.

The R21-million deal will see Life Healthcare sell off its Alliance Medical Group diagnostic imaging business to iCON Infrastructure in a deal that is expected to net R10.8-billion in proceeds, pending approval from shareholders and regulators.

Shareholders are expected to see about R8.4-billion of this money, while R2.4-billion will be reserved for future growth initiatives. DM

Monday, 6 November 2023

Dis-Chem’s weakening performance shows that Covid-era profits are over

The soaring profits of the Covid era appear to be over, judging by Dis-Chem’s latest interim results, which reveal that profit has declined sharply over the past six months, despite a 9.4% revenue increase to R17.9-billion.

For the period from 1 March to 31 August, revenue grew by 8.1% to R15.6-billion, with pharmacy store revenue growth at just 5.9%. Covid-19 vaccines and testing had weighed heavily on the prior period’s results: if factored out from both periods, retail revenue would have grown by 9.2%.

Over the past six months, the group, which has a market cap of R21.72-billion, opened or acquired 10 retail pharmacies, which swells its footprint to 268 retail pharmacy stores and 54 retail baby stores.

In the period under review, Dis-Chem reserved R279-million in capital expenditure: R156-million for expansion (including stores as well as IT) and R123-million to maintain the existing retail and wholesale networks.

Last month, the Competition Commission approved the purchase of the 63,000m² distribution centre in Gauteng, which will cost Dis-Chem R502-million and will hike capex for H1.

Dis-Chem’s wholesale revenue, which is still its biggest revenue driver, grew by 13.5% to R13.7-billion. The Local Choice franchises grew by 19.1%, while its independent pharmacies grew by 18%.

Contrast that with market leader Clicks, which expanded its retail footprint to 885 stores with the opening of 45 new stores in a year. The group now has a network of more than 880 stores and 710 pharmacies, supported by a growing digital presence. Over the past year, its turnover grew by 8.2% (excluding vaccinations) to R41.6-billion, with retail turnover increasing by 12.2%.

Clicks plans to open between 40 and 50 new stores and 40 to 50 pharmacies, with a capex of R880-million for the 2024 financial year. This includes R487-million for new stores and pharmacies and the refurbishment of 50 to 60 stores. It’s also investing R393-million in supply chain, technology and infrastructure.

The retail pharmacy space is heavily concentrated: the Spar group has more than 140 independently owned Pharmacy at Spar stores nationwide, including clinics at selected stores, the Shoprite group (trading under the MediRite name) has 134, and the Link group has more than 200 across southern Africa.

Dis-Chem’s total income grew by 5.1% to R5.4-billion and retail total income grew by 6.5%, with retail margins down from 30.2% to 29.8%.

Basic earnings per share and basic headline earnings per share are 58.3 cents and 58.2 cents per share, respectively, which are down by 16.7% and 17.2%, respectively.

The group’s retail expenses grew by 11.3%, as Dis-Chem invested in new stores and acquisitions. Other costs included a sharp rise in employee costs of 9.8%, higher diesel costs to run generators during power outages, higher IT costs due to a new point-of-sale system roll-out, and increased advertising expenditure. Wholesale expenses grew by 5.5% due to the increase in volumes through the wholesale space resulting in an increase in casual labour shifts as well as higher diesel and municipal costs.

It has declared an interim cash dividend of 23.24348 cents per share, based on 40% of headline earnings, which is down by 17.3% from the prior comparable period.

Last year’s interim results painted a more upbeat picture: Dis-Chem reported double-digit group and retail income increases, as the Covid threat receded and customers spent on non-pandemic-related items. Its aggressive expansion programme added 251 retail pharmacy stores and 53 retail baby stores over the period, and total income grew by 22.8% to R5.2-billion for the six months ended 31 August. Group revenue also grew 9.3% to R16.3-billion, with retail revenue rising to R14.4-billion.

Commenting on the results, CEO Rui Morais, who succeeded Ivan Saltzman on 1 July, said they were satisfied with the group’s performance during the period, notwithstanding a tough trading environment.

“The constrained economic environment, higher interest rates and costs associated with load shedding have resulted in a weaker performance by the group over the prior comparative period.”

He said the group had also been affected by the base effects of the prior year’s performance, which were distinctly different across the two halves of the year, with the first half of the prior year delivering a strong performance when compared with the second half of the prior year.

“A more equal distribution of earnings across halves is expected in the current financial year. Contributing to the stronger first-half performance in the prior year was the acquisitions of the warehouse properties resulting in a R72-million once-off gain from the release of the lease liability and right-of-use asset as well as the impact of Covid-19 vaccine administration and testing services, which has ended and did not contribute in the current financial period.” DM

Thursday, 2 November 2023

Pepkor customers under socioeconomic pressure, group says in trading update

The cost-of-living crisis is eating into the profits of one of South Africa’s most affordable retail groups, Pepkor Holdings.

Pepkor, which counts PEP, Ackermans, Shoe City, HiFi Corp and BUCO among its subsidiaries, issued a trading update on Thursday for the year ended 30 September, ahead of its annual results, which are expected at the end of November.

The investment and holding company said its customers were under financial pressure due to the high cost of living, high unemployment, rolling blackouts and the disruption of social grant payments.

In May, when announcing its interim results to the end of March 2023, Pepkor raised concern about the disruptions to SA Social Security Agency payments, which were hurting its low-income customers. At the time, it said its customers had no choice “but to prioritise spending on necessities to contend with high levels of inflation, in particular, the increased cost of food and transport”, adding that their ability to earn an income was also affected by “unprecedented levels of electricity load shedding and disruption in social grant payments”.

It said trading hours lost by the group due to rolling blackouts had increased by close to 500% during this period (211,000 hours). Diesel costs increased by 142% to R72-million for the period.

Business has bounced back for Pepkor in the second half of this year, with group revenue, which included a 53rd trading week, increasing by 7.7% to R87.4-billion. The group’s Avenida business in Brazil (which it acquired in February 2022) added 4.3% in FY23 to Pepkor’s revenue, from 2.4% in the previous year.

On a comparable 52-week basis, group revenue increased by 6.5% for the year.

Revenue grew sharply in the second half to 8.8%, boosted by stronger sales: Merchandise sales were up by 6.4%, with sales growing by 8.2% in the second quarter, as compared with just 4.8% in H1.

Key product categories did well for business units: PEP grew its babies, adults and home segments; Ackermans gained market share in its schoolwear, younger girls and lingerie segments; and the JD Group (which owns Russells, HiFi Corp and Incredible Connection) expanded in computer and audio-based merchandise.

The group said trading in durable products and the building materials market was weaker, which weighed on the JD Group and The Building Company’s performance, but both businesses did better than their peers.

BUCO (The Building Company) was relatively stagnant, with sales at the hardware stores up by 0.8% in both H1 and H2.

Stats SA’s latest building update, released on 19 October, suggested that residential completions were down by 9.4% year on year. Confidence among builders also dipped in Q3 of this year, according to the Bureau for Economic Research.

Pepkor’s group cash sales were up by 5.6% and credit sales were sharply up, by 35.6%, due to the implementation of the group’s credit interoperability strategy in its South African clothing, footwear and home retail brands.

However, with 90% of its sales in cash, Pepkor said “credit is not a material sales enabler for the group. Credit continues to be granted on a prudent basis within the group’s conservative credit methodologies.”

Tenacity Financial Services opened a record number of new accounts (794,000) during the year, which helped sales via cross-shopping by customers in group retail brands.

“The group maintained its conservative approach to credit granting. Collections, non-performing loans and provision levels remain well within tolerable levels across all credit books.”

However, its credit book growth had increased debtors’ costs for the year.

It opened 324 new stores this year, which brings Pepkor’s total to 5,917 stores.

Pepkor’s annual results will be published on 29 November. DM

Tuesday, 31 October 2023

SAB’s Zamalek drives sales for AB InBev in South Africa

It’s been a thirsty season and Zamalek – also known as Carling Black Label, South Africa’s top beer brand – has given AB InBev’s local operator South African Breweries (SAB) a healthy boost this quarter, with volume growth in the high teens.

Volumes of global brands grew by more than 35%, driven by Corona and Stella Artois, said the world’s biggest brewer, AB InBev, reflecting on its results for the third quarter of 2023.

The brewing giant’s local unit, SAB saw revenue per hectolitre (hl) growth in the high-single digits, driven by what it said was “revenue management initiatives and continued premiumisation”.

Richard Rivett-Carnac, SAB’s CEO, said their volumes had increased by high-single digits. Earnings before interest, taxes, depreciation, and amortisation (Ebitda) grew by mid-single digits, as top-line growth was partially offset by anticipated transactional foreign exchange and commodity cost headwinds.

In the first nine months of the year, revenue grew by the mid-teens, with high-single-digit revenue per hl growth and a mid-single-digit increase in volume. Ebitda increased by 9.6%.

The group’s top line grew by 7.1% in South Africa, with revenue per hl increasing by 7.3%. Volumes were flattish, growing by 5.7%

“The momentum of our business continued in the third quarter, gaining share of both beer and total alcohol, according to our estimates. Carling Black Label, the number one beer brand in the country, led our performance this quarter with high-teens volume growth, and our global brands grew volumes by more than 35%, driven by Corona and Stella Artois.”

Globally, total revenue was up 5% per hl, with growth of 9%. Underlying profit was up $1.735-billion in Q3 2023 compared to $1.682-billion in Q3 2022.

Budweiser, Stella Artois, Corona and Michelob Ultra did well for the brewing giant outside their home markets, with a 16.3% increase in Q3.

However, despite the top-line increase of 5%, revenue growth in about 80% of their markets was driven by pricing actions, ongoing premiumisation and other revenue management initiatives.

Volumes were down by 3.4%, as growth in the Middle Americas, Africa and Asia Pacific regions was primarily offset by performance in the US and a soft industry in Europe.

The no-alcohol portfolio grew: Sober October wrapped up on Tuesday, and AB InBev has seen strong growth in the no-alcohol portfolio globally, driven by Budweiser Zero in Brazil and Corona Cero in Canada, Mexico and Europe.

Revenue from premium brands grew by 15.1% outside their home markets: Corona was up by 18.8%, Budweiser by 11.8%, Stella Artois by 20.3% and Michelob Ultra by 11.5%.

The Beyond Beer category saw a mid-single-digit increase, globally offset by a soft malt-based seltzer industry in the US. Global growth was driven by the expansion of Flying Fish in Africa and the Vicky portfolio in Mexico.

Leveraging their digital direct-to-consumer products, the group is developing new consumer insights and consumption occasions.

Across Latin America, Zé Delivery and TaDa are driving increased in-home consumption of returnable glass bottle packs by making them more available and convenient, said Michel Doukeris, CEO of AB InBev.

“The strength of our global footprint delivered another quarter of top and bottom-line growth. Revenue increased by 5% with an Ebitda increase of 4.1%. We continue to invest in our strategic priorities for the long-term.”

About 66% of the group’s revenue is through B2B digital platforms, with the monthly active user base reaching 3.4 million users.

On 25 October, AB InBev’s rival, Heineken, reported that it had sold 4.2% less beer in the third quarter, as the Dutch brewer faced a difficult macroeconomic climate and consumers were turned off by higher prices.

In August, Heineken sold its Russia operations for one euro – more than a year after saying it would quit its business there due to the war in Ukraine, and a month after a South African representative assured Daily Maverick in July this year that it had long since exited its Russian business.

Heineken in August sold its business in Russia to domestic firm Arnest Group, which took 100% of shares and assets, including its seven breweries, for a symbolic single euro. It said it had provided employment guarantees for 1,800 employees for three years.

The company had faced criticism for dragging out its departure from Russia, which it vowed to exit in March 2022 shortly after the full-scale invasion of Ukraine. Heineken and other large firms with manufacturing operations in Russia have said leaving has been a complex process with a high risk of assets falling under state control.

CNBC reported that volumes were down 4.2% on the previous year, taking the decline across the first nine months of 2023 to 5.1%. Revenue was higher in the quarter due to price hikes, up 2% to $10.17-billion. DM

Thursday, 26 October 2023

Clicks says 2024 trading likely to be constrained despite resilient results

Leading pharmacy chain Clicks seems fit as a fiddle after declaring its annual results for the year ended 31 August 2023, although it warned that trading conditions were likely to remain constrained in the new financial year.

The health and beauty retailer and pharmacy group has a network of over 880 stores and 710 pharmacies, supported by a growing digital presence.

It has revealed that group turnover for 2023 was up 8.2% (excluding vaccinations) to R41.6-billion, with retail turnover increasing by 12.2%.

Distribution turnover grew by 1.5% for the year as UPD – which provides bulk distribution services for the Clicks Group, major private hospital groups and 1,200 independent pharmacies, as well as pharmaceutical manufacturers – was affected by lost sales opportunities to Clicks and private hospitals during a systems implementation in the first half, as well as lower demand from pharmacies and a shift of products within UPD.

Adjusted total income grew by 10.8% to R12.2-billion (up 7.6% including the insurance recoveries).

The retail margin expanded by 130 basis points and saw strong growth in higher-margin private label products and the recovery in the beauty category, while the low-margin vaccination programme came to an end.

Retail costs were affected by higher insurance premiums and diesel costs, increasing by 11.4%, while retail costs grew by 7.4%.