Illustrative image | Sources: Vapour from cooling towers of the Eskom Holdings Kriel coal-fired power station in Mpumalanga, South Africa on 21 March 2022. (Photo: Waldo Swiegers / Bloomberg via Getty Images) | Adobe Stock | Daniel Acker / Bloomberg via Getty Images

Illustrative image | Sources: Vapour from cooling towers of the Eskom Holdings Kriel coal-fired power station in Mpumalanga, South Africa on 21 March 2022. (Photo: Waldo Swiegers / Bloomberg via Getty Images) | Adobe Stock | Daniel Acker / Bloomberg via Getty Images If we want a power system dominated by clean, renewable energy, we need lots of natural gas – or so we are told.

This drumbeat, which has set up gas as a “critical transition fuel”, has been meted out by government ministers, the oil and gas lobby, some serious researchers and everyone of varying degrees of cynicism in between.

“The gas industry will be with us in the transition, in a big way,” Mineral Resources and Energy Minister Gwede Mantashe told Parliament earlier this month.

“If Shell is able to find domestic offshore gas, this could play a key part in diversifying South Africa’s energy portfolio,” Hloniphizwe Mtolo, the chair of Shell’s downstream operations, told the Eastern Cape High Court in November, adding that gas is a “strategic bridge to low carbon emission targets”.

President Cyril Ramaphosa even endorsed this view. At the Mining Indaba in Cape Town, he told delegates that African countries “need to be able to explore and extract oil and gas” as this would ensure “energy security” as they decarbonise their economies.

But when we say gas is “critical”, how much gas do we actually need?

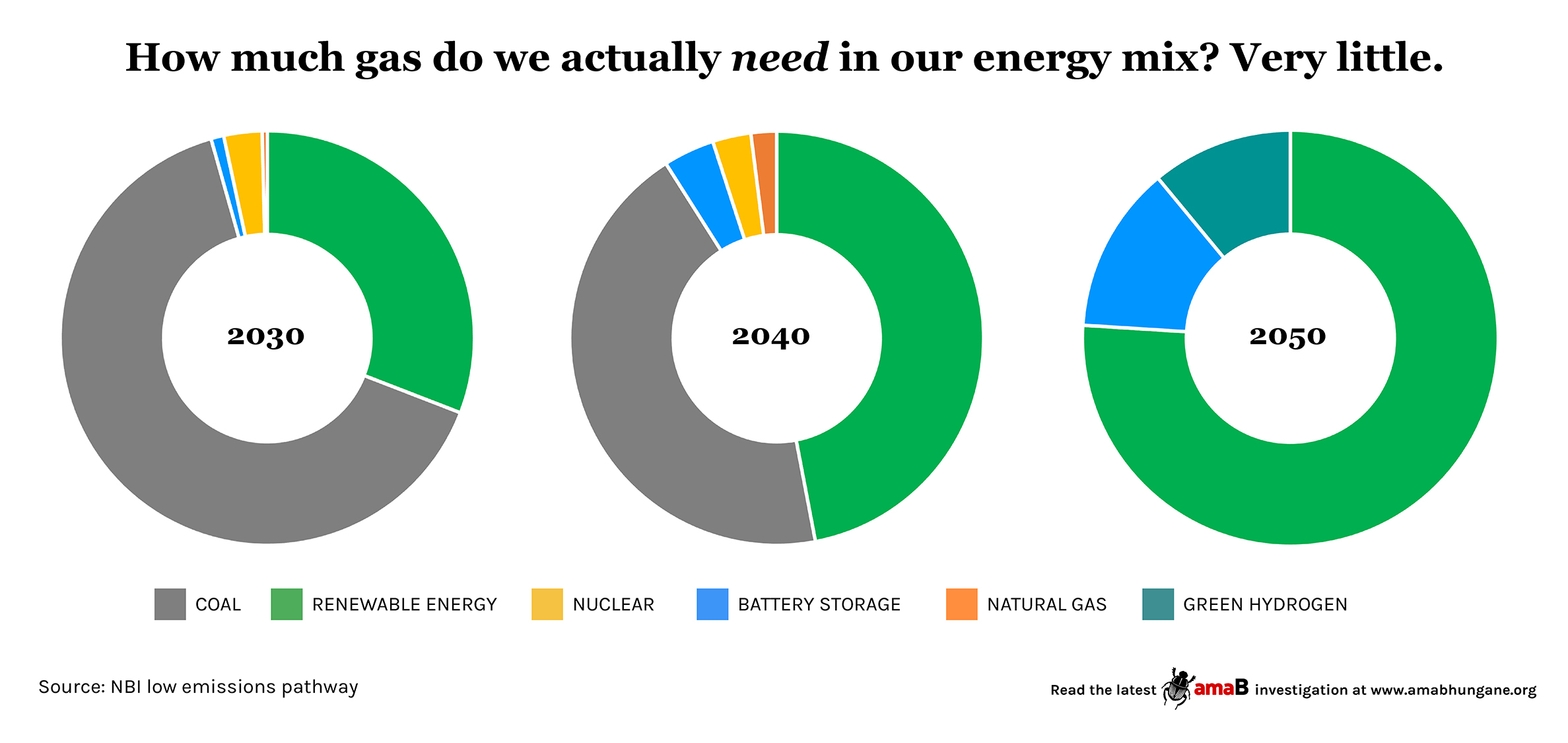

In February, the National Business Initiative (NBI) – a coalition of 86 major companies, including Eskom, Sasol and Shell – published a study showing that the electricity sector likely needs just 17 petajoules (PJ) of gas a year until 2035.

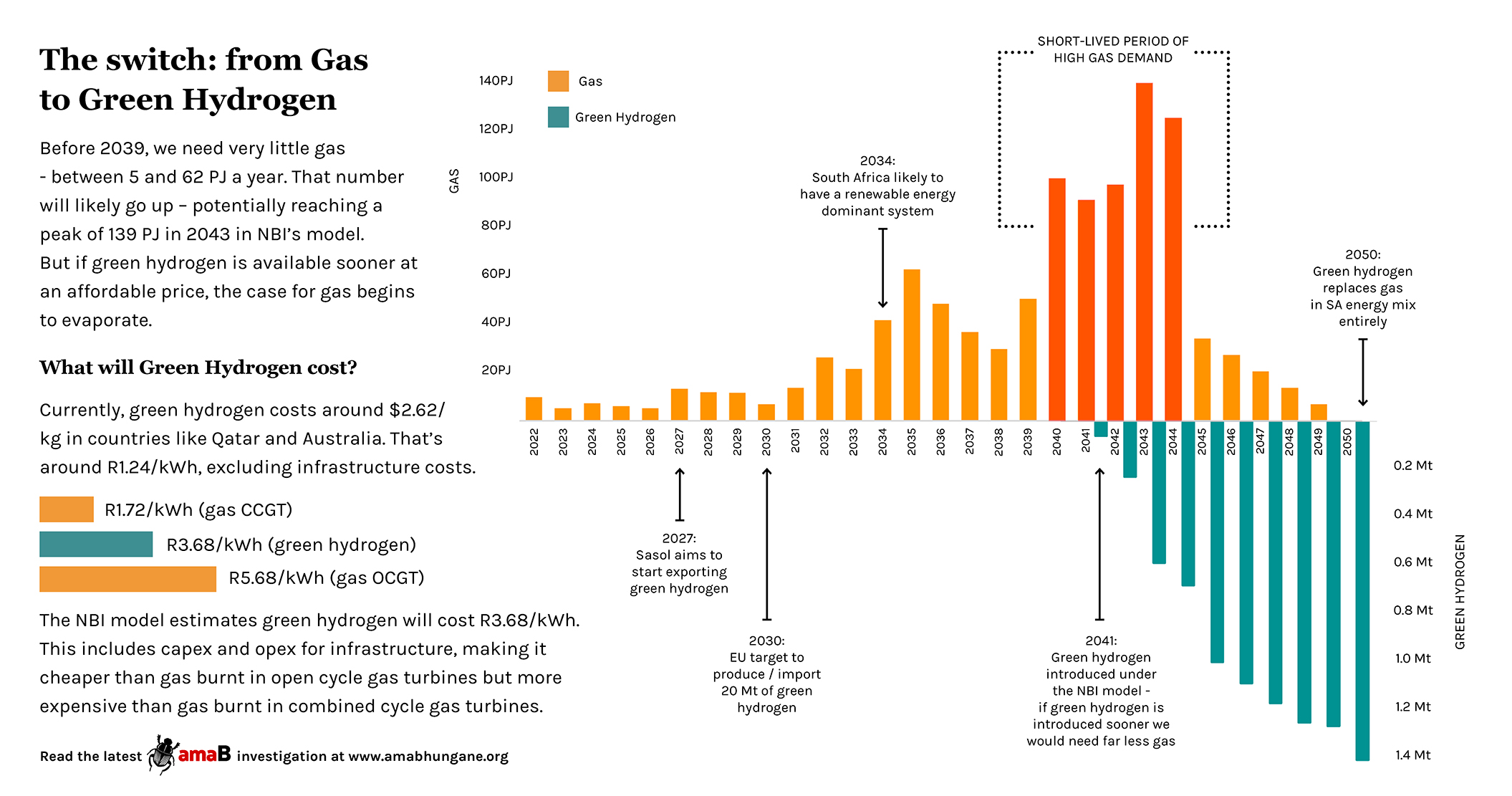

To put that into perspective, South Africa already imports 180 PJ a year from Mozambique. Demand from the electricity sector would increase as we switch from coal to renewables – rising to 100 PJ by 2040 – but is unlikely to ever be high enough to support a domestic gas industry. And will fall off a cliff as soon as green hydrogen – at affordable prices – becomes available.

The NBI report, titled The Role of Gas in South Africa’s Path to Net-Zero, confirms a 2020 study by Meridian Economics and government’s Council for Scientific and Industrial Research (CSIR), which concluded that a flexible power source like gas should make up no more than 4% of our energy mix by 2050.

“[T]he main finding of our work is renewables, renewables, renewables ... we need to build three to four gigawatts of renewables every year from now until 2050,” Steve Nicholls, the NBI’s Head of Environment, told amaBhungane.

But – driven by a desire to exploit the final boom of the fossil fuel industry – a campaign for gas is being waged, based not on what our electricity system needs, but on what a handful of politicians, and oil and gas executives want.

“[T]here are strong indications that South Africa is potentially on the verge of a gas investment flurry that could prove to be a very expensive mistake for the South African people,” the International Institute for Sustainable Development (IISD), a pro-environment research group, warned in a recent Gas Pressure report.

“Many of these indications come from economically and politically powerful gas interests, including interests inside government.”

This plan would turn the electricity sector into the “anchor” buyer of gas in South Africa, delay the roll-out of renewables, and by NBI’s own estimate, generate much higher carbon emissions than necessary.

As much as R1-trillion

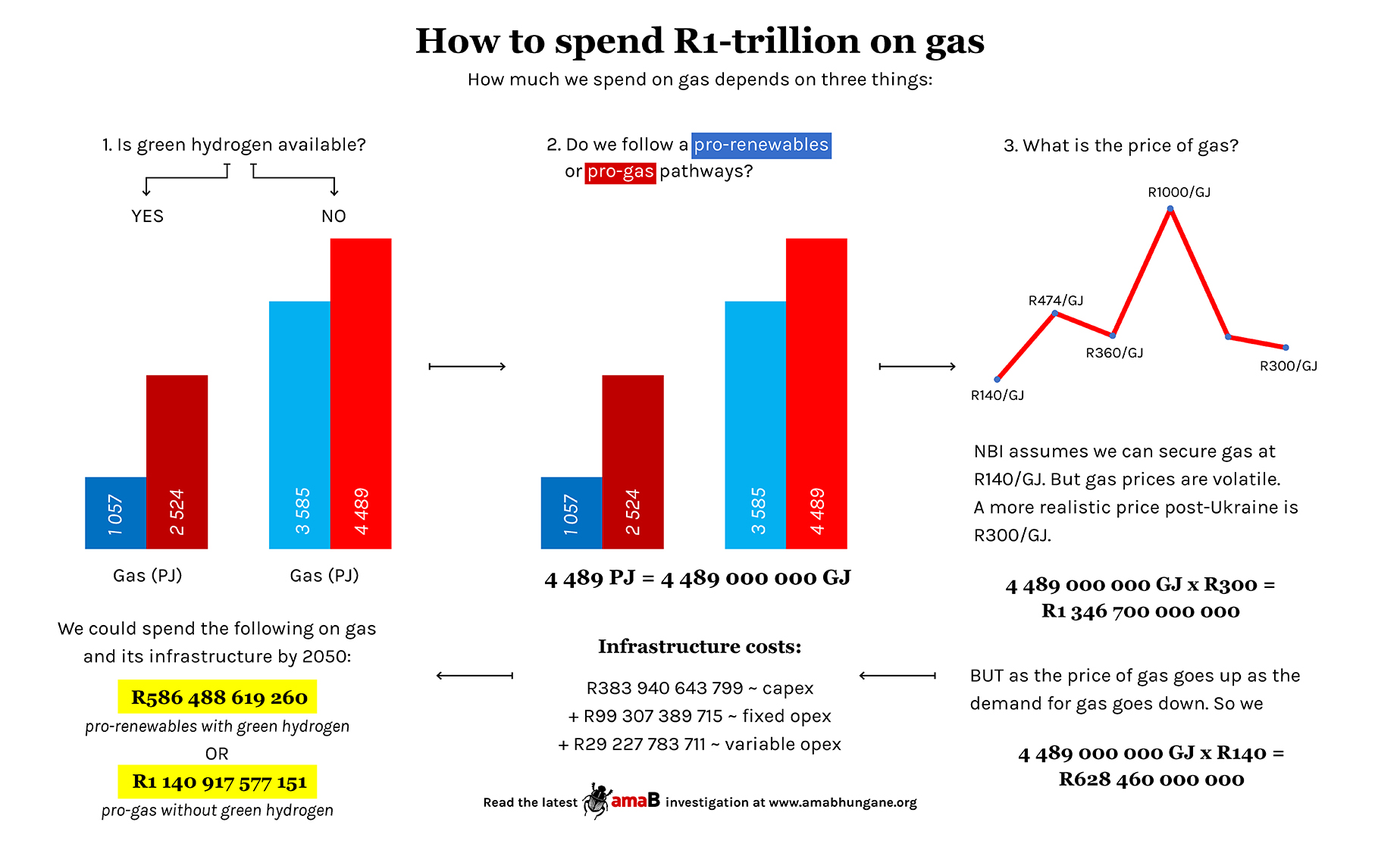

It would also potentially mean South Africa Inc would spend R628-billion – or perhaps as much as R1-trillion – on gas.

The question amaBhungane set out to answer is: how much gas does the electricity sector need? The answer that emerges: very little. This conclusion is not always obvious: in the case of NBI, their report comes across as bolstering the case for gas, while the numbers in their model tell a different story.

But numbers do not lie: adding more gas to the electricity sector would likely lead to higher costs and more energy insecurity, and would take up an extra gigatonne of our scarce carbon budget.

This is how we came to that conclusion.

How much gas do we actually need?

That there will be a transition away from coal is no longer up for debate: Eskom is scheduled to shut down 22 gigawatts (GW) of coal by 2035, and, plagued by breakdowns, our coal fleet is retiring itself ahead of schedule.

The question is, what replaces coal?

Energy system modelling is a complex exercise: it looks at the country’s future energy needs and how best to meet them with a mix of coal, nuclear, gas and renewables. Only a handful of organisations in South Africa have these skills, and they all largely agree that the cheapest option is to build a system dominated by renewable energy.

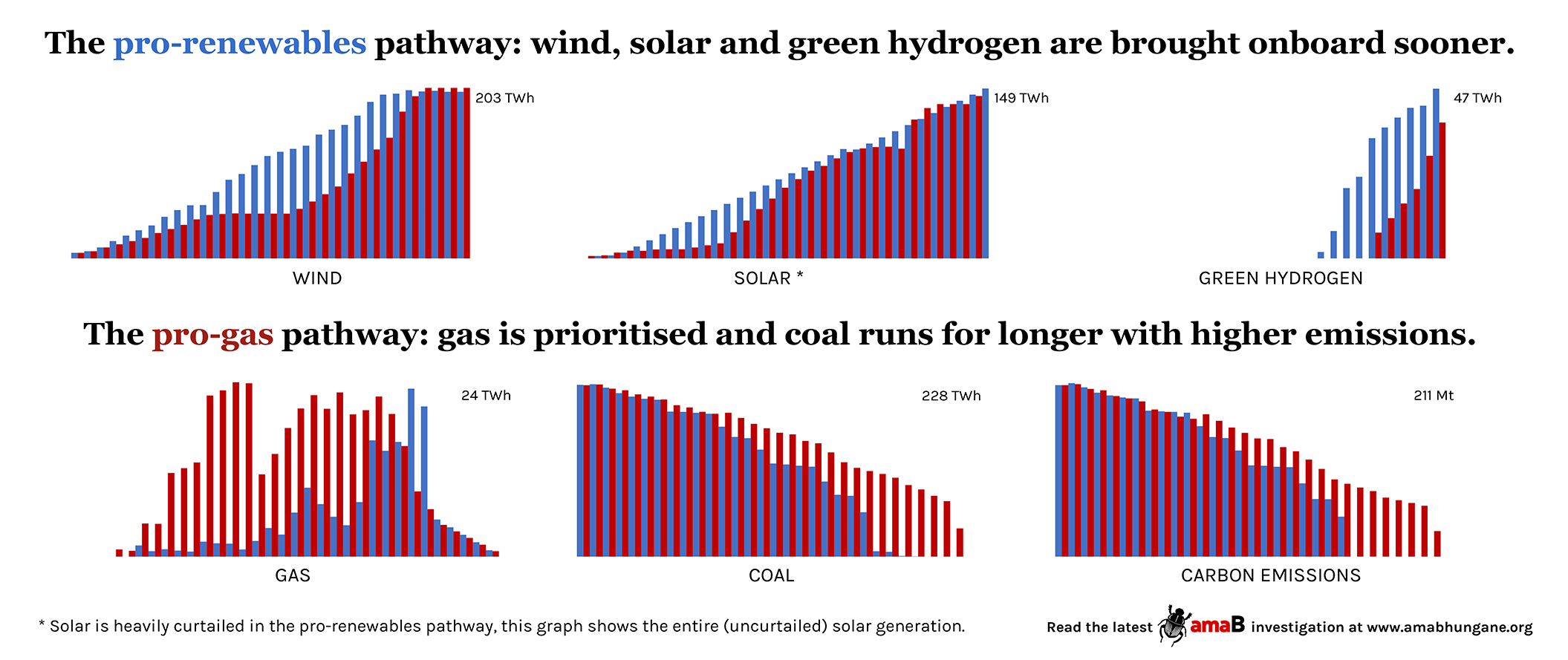

In 2020, Meridian and CSIR concluded that the “least-cost” option would be to build a system where 74% of power comes from renewable energy by 2050. The NBI model, released in February, recommends that 76% of power comes from renewables by 2050.

“There is remarkable agreement, even at a numerical level in terms of capacity, that we should be building a stack of renewables – solar and wind – and that we should not be building any new nuclear, hydro or coal. Coal, because of costs and emissions, and nuclear and hydro, essentially because of costs,” energy specialist Dave Collins of Mac Consulting, said during a recent webinar hosted by Chris Yelland on the role of gas.

The role of gas is more contested. If a middle-of-the-road consensus exists, it says that we will need a limited amount of gas – or an alternative, like green hydrogen – to fill in the gaps, after we switch from a coal-dominated power system to one dominated by renewable energy.

Both models predict a likely renewables tipping point in the mid-2030s. At that point, some form of flexible power will need to be available as a back-up for when both wind and solar underperform for stretches of several days.

It is not a given that gas would play this role: green hydrogen produced from renewable energy or batteries would be a cleaner option, and we could continue burning diesel until green hydrogen is available, bypassing gas entirely.

- SIDEBOX: What is green hydrogen? Hydrogen is a gas that can be burnt like fuel. It is produced by using electricity to split water molecules into hydrogen and oxygen, and is colour-coded according to the type of energy used in its production. Brown hydrogen is produced using electricity from coal; grey and blue hydrogen uses electricity from gas; green hydrogen is produced using electricity from renewable energy. The advantage hydrogen offers is that it can be stored and burnt as needed.

If we go with gas, NBI’s model shows that gas would need to make up less than half a percent (0.4%) of our energy mix by 2030, and less than 2% of the energy mix in 2034, the year when renewable energy likely overtakes coal as the main source of power.

By 2042, when the last coal power plants retire (ahead of schedule), gas still only makes up 6% of the energy mix in NBI’s model. By 2050, flexible power makes up 11% of the energy mix, but green hydrogen will likely have replaced gas completely.

The understudy’s understudy

The reason for these modest volumes is that gas will increasingly not be the first choice to provide “peaking” power when demand surges in the morning or at night. Although battery storage has traditionally been more expensive than gas, prices are dropping. After 2030, NBI expects battery storage to be cheaper than gas.

This reduces gas to providing “balancing” power, especially after 2030. Balancing is the understudy’s understudy of the power system, a last resort when all of the cheaper or better options are unavailable.

As Darryl Hunt, a widely-respected gas consultant, puts it: “Gas is the insurance policy for when all other planning assumptions go wrong.” But Hunt believes “you need to have it”.

An obvious question is: if we take the view that South Africa will need a small amount of gas to support a renewable-dominant system, why not say yes to Karpowership?

The three gas-fired projects were selected as preferred bidders in the Risk Mitigation Independent Power Producer Procurement Programme (RMI4P) but have failed to secure environmental permits to operate. Find out more on amaBhungane’s Karpowership Special Projects page.

The problem is that the proposed contracts contain a punitive take-or-pay clause, meaning that Eskom has to take on average 12 hours of power a day for the next 20 years. But we don’t need Karpowership’s 1.2 GW to burn gas for 12 hours every day; we need a huge number of turbines – potentially between 10 and 25 GW – to stand idle for most of the year.

That sounds inefficient but is the nature of balancing power: only called on when renewables hit a low patch for several days, and there is not enough power to recharge batteries and replenish pumped storage.

Then, and only then, do we need gas – or an alternative fuel – to step up.

To ship or extract

This is unwelcome news to both a government, eyeing gas royalties, and an industry, eyeing untouched offshore gas reserves.

The 17 PJ of gas a year that NBI estimates we need until 2035, is the equivalent of roughly six deliveries a year from standard 150,000 m3 liquefied natural gas (LNG) carriers – far too little to justify a major investment in gas.

This is largely in line with Meridian’s latest findings, presented on Thursday, showing that we’d need between 25 to 40 PJ of gas by 2030 - the equivalent of 8 to 14 LNG deliveries a year - if we solely switch to gas to provide peaking power.

That number would rise if our demand for gas increases – potentially reaching a peak of 139 PJ in 2043 in NBI’s model – but that period of high demand is probably short-lived: gas demand will likely fall off a cliff as soon as green hydrogen becomes available. And it’s likely to happen sooner than the NBI model predicts.

The European Union has set a target of producing and importing 20 million tonnes of green hydrogen by 2030. In NBI’s model, green hydrogen is only introduced in 2041, with demand rising to 1.4 million tonnes in 2050.

If South Africa can secure affordable green hydrogen sooner, the case for gas begins to evaporate fast.

Hidden costs (and benefits) of solar

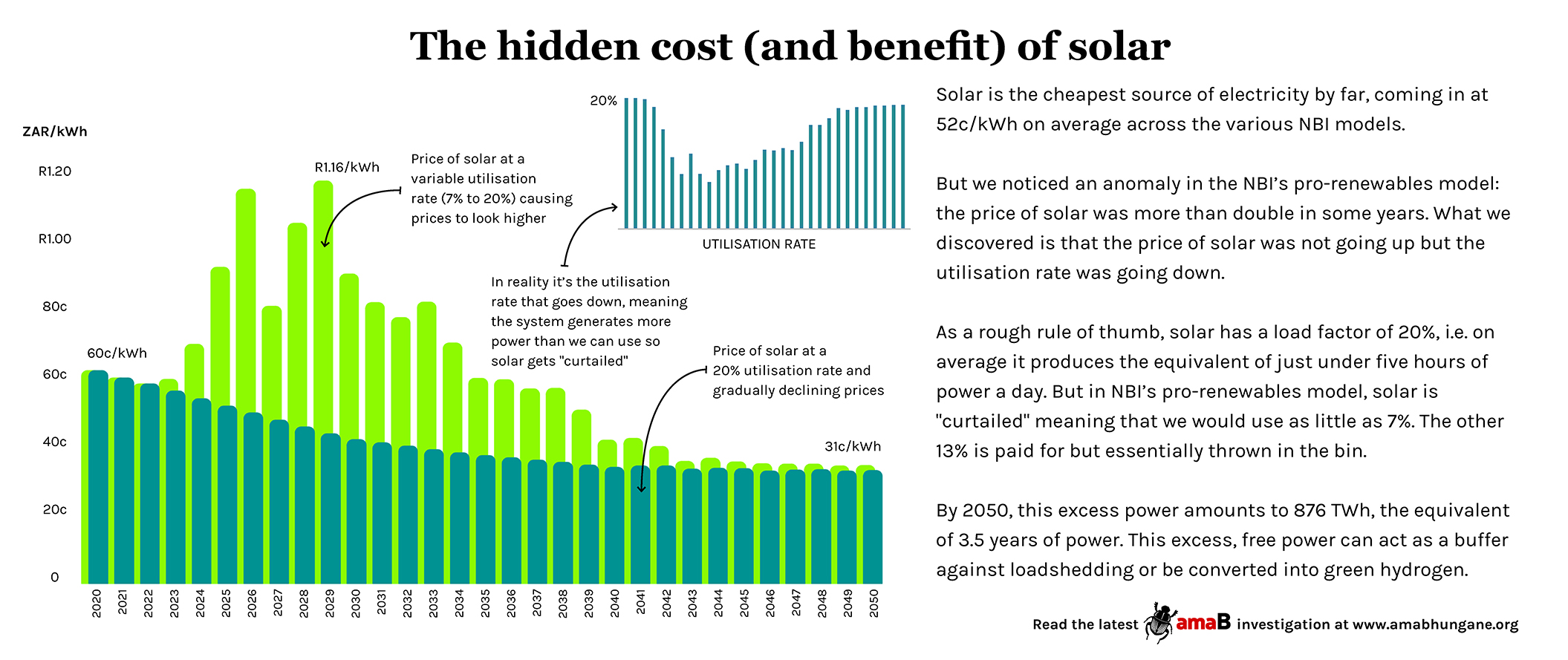

What the NBI report does not disclose is that pursuing a renewables pathway generates vast amounts of essentially free, excess electricity.

As a rule of thumb, solar has a load factor of 20%, meaning that it produces the equivalent of just less than five hours of power a day. But in NBI’s model, solar is heavily curtailed.

What this means is that we would pay for the full 20%, but in some years use as little as 7%. The other 13% is effectively written off in NBI’s model.

“[S]olar is curtailed more than wind because of the ‘useful hours’ not coinciding with peak demand times – hence solar load factors are lower than wind load factors,” Nicholls explained.

“You could also argue, why curtail renewable energy and not coal? The answer is that coal power stations are inherently inflexible … you cannot ‘swing’ load up and down continuously without fundamentally damaging the boiler.”

But this discarded power represents a major asset: by 2050, it would amount to 876 TWh or, on average, an additional 14% of electricity a year, which can act as a buffer against loadshedding, provide feedstock for green hydrogen, or be distributed to indigent households.

The NBI report mentions curtailed power only once, in a footnote.

“The incumbents, meaning Eskom and the system operator ... treat excess [electricity] as something that has to be curtailed – it's bad,” says energy specialist Clyde Mallinson. “And the whole real exciting bit is that this excess is the biggest opportunity in the last 100 years ... It’s low marginal cost, excess energy to electrify sectors.”

But if the writing is on the wall for big gas, government is studiously ignoring the message and instead is punting gas as an energy and industrial game-changer.

Plan B

During Jacob Zuma’s presidency, gas sat on the backburner while 9.6 GW of nuclear, with its Russian backers, was presented as our energy future. When that deal failed and it became apparent that new coal would never be funded, attention turned to gas.

In December, the Department of Mineral Resources and Energy (DMRE) revived the long-shelved Gas Masterplan, giving a preliminary look at the bright, gas-fired future it envisages: gas will “rejuvenate an overburdened, out-dated energy infrastructure”, “reduce cyclical energy shortfalls” and “stimulate the economy,” the Gas Master Plan basecase report promised.

But the industry faced a catch-22: gas would not be supplied without demand, and demand would not materialise without supply. What is needed, the report concluded, is an anchor client, someone to buy enough gas to make gas infrastructure and possibly an offshore gas project bankable.

The obvious candidate, according to the DMRE, is our electricity sector.

“A challenge in developing the gas sector is to bring gas demand and supply on stream at the same time ... One way of breaking this impasse is to create significant ‘anchor’ gas demand through the development of a gas-to-power programme,” the report concluded.

The idea of using the electricity sector to anchor demand is not a novel one. In response to the Covid pandemic, Business for South Africa (B4SA), a spin-off of Business Unity South Africa, produced a plan to get the economy back on track.

The plan – developed by Boston Consulting Group, the same consultants who produced the NBI report – pushed the idea that government should prioritise gas-to-power projects “to create gas anchor demand via increasing utilisation of gas [for peaking] as well as mid-merit load”.

The DMRE appears to be on the same page: “The benefit of prioritising gas for power generation provides for large and concentrated volume of offtake,” the report noted, adding that the “financial viability” of the gas sector “must be secured in order to incentivise supply and new investment”.

This endowmentist view – that we cannot leave fossil fuels unexploited – has become the guiding ideology of energy policy under Mantashe, even as severe storms, fueled by climate change, decimate Kwazulu-Natal.

Mantashe has spent the past month bearing down on the Eastern Cape, which is emerging from a four-year drought, another spinoff from climate change.

Mantashe wants to persuade traditional leaders to support Shell’s attempt to restart its seismic survey off the Transkei Coast and has promised to make the province the “gas capital” of the country.

- Shell’s seismic survey to prospect for oil and gas was halted in December, after a judge found that it failed to consult with impacted communities. Shell is appealing the decision in the Gqeberha High Court, starting tomorrow.

As incendiary as Mantashe is, he appears to have his party’s support: “The growing opposition to oil and gas exploration needs to be confronted politically,” the ANC wrote in a recently published policy document. “[I]t is clear that South Africa’s endowments of oil and gas could be a source of wealth, as well as increase our energy security options.”

The ANC’s position spits in the face of both the Intergovernmental Panel on Climate Change and the International Energy Agency, which warned that the world must halt all new investments in fossil fuels this year if we want to avoid the most catastrophic effects of climate change.

Investments in new fossil fuel infrastructure would be “moral and economic madness”, United Nations secretary-general António Guterres warned last month.

Mantashe has called for the country’s energy roadmap – the Integrated Resource Plan (IRP) – to be updated to include more gas, but has so far not provided concrete figures.

But NBI has, and the numbers are terrifying.

The R1-trillion detour

When the NBI Role of Gas report was published in February, many people interpreted it as making the case for gas. It is easy to see why:

“[G]as will play a critical role in enabling the decarbonisation of South Africa’s electricity sector”, the report reads, and “gas can, if affordably supplied, play a key role as a transition fuel”. It says that gas would “enable the integration of renewable energy” into the power grid and “set the country on a net-zero trajectory”.

While this was in the context of endorsing a rapid shift to renewables, the report also controversially laid out a second (alternative) pathway that would still build a carbon-neutral, renewables-dominant system by 2050, but would first take a major detour into gas.

Nicholls refers to this as the IRP-adjusted pathway because it keeps us on some of the existing IRP’s constraints in place until 2030, like limits on solar and wind, even as critics charge that the 2019 IRP is already rendered obsolete by recent technical advances, cost changes and climate deterioration.

Although more progressive than the government’s current energy plan, under this pro-gas pathway, the electricity sector’s demand for gas would increase from 7 PJ to 170 PJ by 2030.

This pathway would not only incorporate the 1.2 GW Karpowership contracts in its current form – burning gas for 12 hours a day for 20 years – but would add another 38 GW of gas-to-power projects running for, on average, three hours a day, until 2049.

By 2050, this thirst for gas could burn through 4,489 PJ, costing anywhere from R628-billion to R1.35-trillion.

Although NBI has several oil and gas companies among its members, it maintains it is not trying to steer government towards gas, but rather provide a roadmap to get to net-zero.

“[T]o some degree we find this debate on gas really frustrating, because the key finding of our work is that we have to fundamentally invest in renewables and that the future for South Africa is a renewables-based grid,” Nicholls told amaBhungane.

“[T]his is still a decarbonisation scenario,” Nicholls explained in a follow-up interview, referring to the pro-gas pathway, “because you're still getting to net-zero by 2050. It just deviates less from the existing IRP”.

The NBI is influential: its CEO Joanne Yawitch is a commissioner on the Presidential Climate Change Coordinating Commission, while Nicholls serves as the commission’s head of mitigation. Yet, NBI also seems to be between a rock and a hard place: unpopular with everyone, from government to its own members.

For instance, the report recommends that the 20-year term of the Karpowership contracts be renegotiated “to avoid higher costs, from the pass-through of sub-optimal LNG prices to consumers, and unnecessarily high load factors (> 50%) for an extended period of time”.

Nicholls says they have also dismissed government’s wish for baseload gas: “[T]he lots and lots of gas scenario is clearly off the table, it’s not logical, it costs too much money, etc.”

He adds, “I've had lots of very complicated board conversations with companies, our message to them was: ‘Coal will definitely not persist in the economy post-2050, it's unlikely to persist in the economy post-2040. Gas will not be in the economy post-2045. These are the parameters within which you have to work.’”

In the spirit of transparency, NBI provided the data from their model, participated in two on-the-record interviews and responded to written questions.

What we concluded was that NBI’s proposed detour into gas offers no financial benefit, provides less energy security and would push South Africa deeper into the climate crisis than NBI’s own proposed alternative.

Price of silver and Russian gas

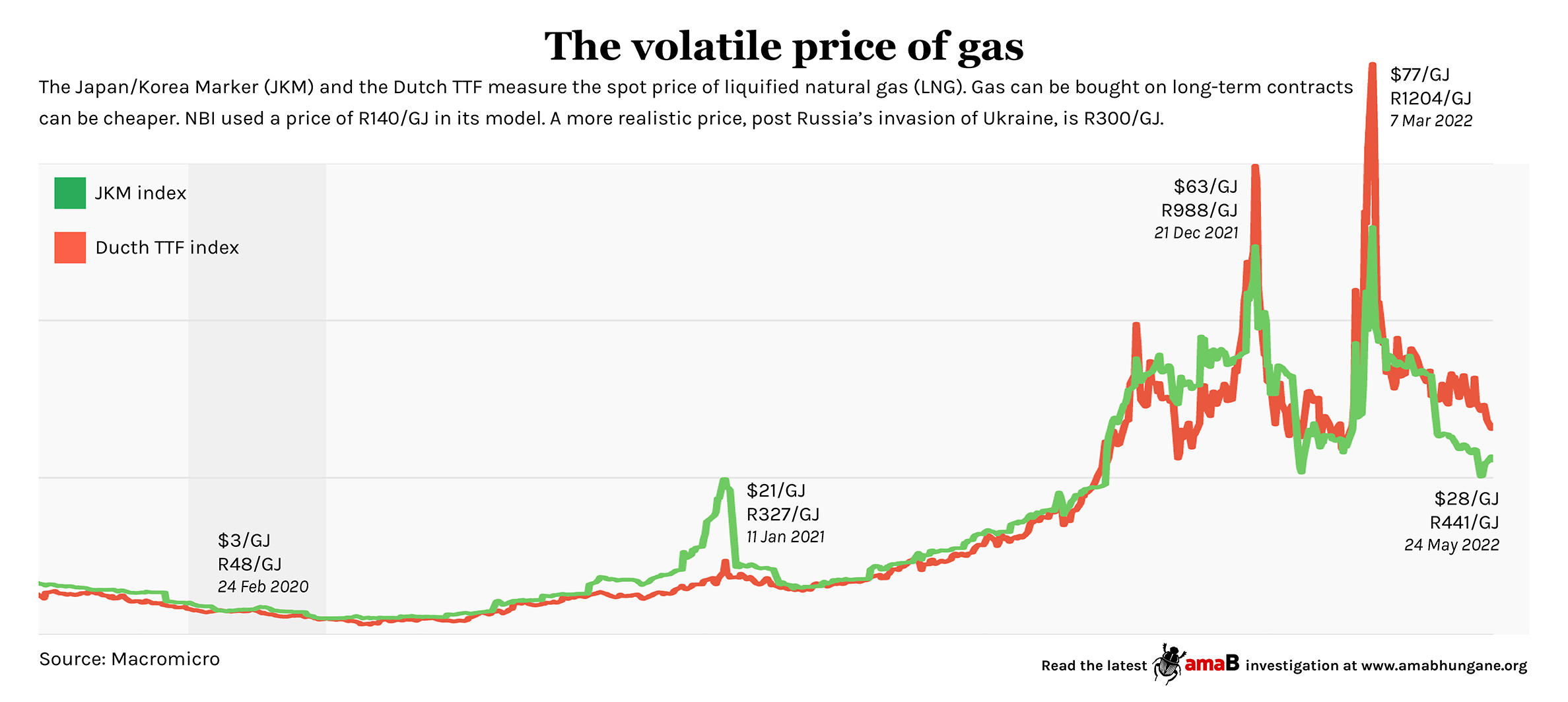

The biggest selling point of the NBI’s pro-gas model is the price: it comes in at, on average, 2c/kWh cheaper than the pro-renewables model. At least on paper.

When NBI started its research in 2020, gas was at record-low prices. Despite being exposed to the rand-dollar exchange rate, gas at $2/GJ (R30/GJ) looked like a sure bet.

But by the time NBI published its first report on the power sector in November 2021, the spot price of LNG had risen to around $31/GJ (R474/GJ). The NBI modelling team believed that gas could be sourced more cheaply on long-term contracts, and used a price of R140/GJ ($9) to build its model.

By February, the spot price of LNG had dropped to $24/GJ (R360/GJ) and NBI confidently predicted again that “gas can, if affordably supplied, play a key role as a transition fuel”.

But nine days later, Russia invaded Ukraine and everything changed.

There’s a story that energy specialist Clyde Mallinson likes to tell: in the 1980s, the Hunts – billionaire brothers from Texas – tried to capture the silver market, believing that they could manipulate the market and turn silver into a safe-haven commodity, like gold.

Within months, the price of silver had increased eight-fold, as the Hunts had planned, but they had also sown the seeds of their own demise: “[W]hen metal prices rise too rapidly, alternatives are quickly found, and the shiny metal of the moment becomes the forgotten cousin in the future,” Mallinson explains.

At the time, camera film was one of the largest consumers of silver. The price shock the Hunts caused became an incentive to develop digital alternatives. “[T]hey unwittingly set the scene for the transition to digital photography.”

Vladimir Putin’s invasion of Ukraine is doing something similar to gas.

At the beginning of March, LNG skyrocketed to more than R1,000/GJ. Prices have come back to R300/GJ levels, but these price shocks, combined with Putin’s willingness to wield gas as a geopolitical weapon, is causing a rethink.

And whereas gas was once prized for providing energy security, it is increasingly avoided for its instability.

In a bid to wean Europe off Russian gas, the European Commission has set a target of securing 20 million tonnes of green hydrogen a year by 2030, half produced from renewable energy in Europe and half imported from countries such as Australia. Under the same plan, Europe will increase its use of renewables to 45% of its energy mix by 2030.

In South Africa, ArcelorMittal recently announced that it will likely leapfrog gas and move straight to green hydrogen as a feedstock for its Saldanha steel plant.

Sasol is also eyeing green hydrogen and plans to start exporting within the next five years.

Sasol, currently the country’s biggest gas user, recently abandoned plans to invest in a pipeline to secure gas from the Rovuma basin in Northern Mozambique, fearing it would become a stranded asset. Instead, Sasol will import LNG, but told shareholders it will “monitor the green hydrogen and low-carbon technology development landscape” in order to avoid “infrastructure lock-in”.

“Gas in the long term is also a fossil fuel and we said we want to get to net zero,” Sasol CEO Fleetwood Grobler recently told Bloomberg. “You need to bridge 10 or 15 years and then you need to go out.”

Part of NBI’s justification for the pro-gas pathways is that its report looks at the role of gas across all sectors – including the electricity sector, but also Sasol’s synfuels business, industrial gas users and transport – and concludes that an anchor buyer, like the electricity sector, could help to secure gas for other industries, allowing them to switch from coal to gas.

While there are obvious decarbonisation benefits in switching the synfuels industry from coal to gas, the case for using more gas in the electricity sector is not there. And if Sasol does not want to be the anchor client for gas, why should the electricity sector – which needs far less gas – pick up the tab?

The door is closing

On Thursday, Meridian presented new figures about the potential role of gas in the power sector. “The spoiler alert here is that we found that the actual use of gas is a fraction of what appears to be envisaged in the Gas Master Plan,” Meridian’s Adam Roff said.

Summarising their findings, Meridian said: “Gas is no longer a transition fuel in the power sector ... There is insufficient demand for gas in the power sector to anchor lower demand in other sectors [and] forcing in large-scale gas will displace renewables, increase emissions and the cost of electricity.”

Dave Collins, who presented at the same webinar, also pointed out that all the studies so far have excluded the cost of carbon. While gas emits less carbon than coal and marginally less than diesel, it is still a fossil fuel. When one takes the entire gas value chain into consideration, emissions from methane – a potent greenhouse gas – increases enormously.

“I think we have to be careful about carbon pricing,” Collins said. “Carbon pricing is going to play a role ... the current effective rate is about $2 - $3/tonne. All the studies used either a zero carbon price or a very low one ... Treasury has said we can expect at least $30 by 2030 and upwards of $120 beyond 2050.”

Following NBI’s pro-renewables pathway – and not its pro-gas IRP-adjusted scenario – would save an extra gigatonne (one billion tonnes) of carbon emissions by 2050. And in so doing, help to avoid some of these costs.

On Thursday, NBI offered a more limited vision of the role of gas: “Our analysis concludes that gas is required in limited volumes with flexible and short payback LNG infrastructure (for example, floating storage) ... with a plan to replace gas with batteries (for short-term balancing) and green hydrogen (for seasonal balancing) from 2030 onwards. Or as soon as reasonable cost parity can be achieved with these green alternatives.”

Kill your darlings

Mineral Resources and Energy Minister Gwede Mantashe believes that gas will be a “game-changer” for the economy. “If we are going to fully develop, we cannot kill the prospects of oil and gas before it has even begun,” he told Parliament in his budget speech last week.

But killing the gas industry before it has begun may actually be the smart choice.

In January, Transport Minister Fikile Mbalula announced that the Strategic Fuel Fund would build a $1.5-billion (R24-billion) onshore regasification plant in Coega in the Eastern Cape. His department later said he was still considering their application for port access rights.

But as with Karpowership, projects like these rely on large volumes of gas and multi-year contracts to recover their costs, and committing to major gas infrastructure projects now carries the risk that these will either become stranded assets, or worse, that we will continue burning gas long after it is useful to subsidise those companies that gambled on gas.

“With the peaking and balancing functions of gas being squeezed out by other technologies, the length of time that unsubsidised gas could compete to provide these roles is decreasing, meaning assets could easily be stranded before reaching a break-even point,” the IISD report explains.

Instead of committing to gas now, the IISD suggests that South Africa hits pause on all gas-to-power projects until 2030, to see how this “disruptive phase” of the energy sector plays out: “[W]e do not need to solve the details of the 2050 energy mix now, though we do need to avoid costly blind alleys.”

A recent study estimated that half the world’s fossil fuel assets could become stranded by 2036, as countries rush to decarbonise as the effects of climate change become more acute. Estimates vary – $990-billion or $3.3-trillion – but there is an undeniable trend already of writing off fossil fuel projects that can no longer generate enough money to recover their costs.

Government is hoping that gas extracted from local, offshore wells will be cheaper, and has proposed that a strategic stock clause be inserted into the Upstream Petroleum Resources Development Bill to force companies extracting gas offshore to sell a portion to the Central Energy Fund’s new National Petroleum Company.

But this would be sold at “prevailing market conditions”, which does nothing to guarantee access to cheap, rand-denominated gas, and would likely take 10 years to reach production, by which point the trickle will likely have turned to a stampede towards the exit sign.

The NBI report proposes that one way around the stranded assets dilemma is to ensure that all gas assets built now – with a capex cost of between R200-billion and R450-billion – can be repurposed for green hydrogen.

“All ... infrastructure needs to be assessed with a lens to minimise the risk of carbon lock-in and stranded assets. All investments considered should be financially resilient to ... costs related to potential repurposing of gas infrastructure ... to enable a substitution of gas with green H2,” the report notes.

But do we really want to spend R1-trillion on an industry that is already writing its obituary – and, in doing so, raise the risk of writing our own? DM

This story was updated on Sunday, 29 May 2022, to more accurately reflect Meridian’s findings.

The amaBhungane Centre for Investigative Journalism is an independent non-profit organisation. We co-publish our investigations, which are free to access, to news sites like Daily Maverick. For more, visit us on www.amaB.org.

Comments

Scroll down to load comments...