When it comes to compound interest, time is your secret weapon and tax-free is your best friend. (Image: Freepik)

When it comes to compound interest, time is your secret weapon and tax-free is your best friend. (Image: Freepik) Question: I’m a 74-year-old “financially illiterate” grandmother who is learning a great deal from your column. I have a newborn grandson and would like to start some sort of “fund” for his future. What would you advise?

Answer: The single most powerful advantage a newborn has over the rest of us is time. If you combine time with a tax-friendly investment, you can turn small monthly amounts into life-changing sums by the time he is an adult.

You have several options. The choices you make will be determined by how much you have available to invest, as well as your timeframe for your grandson to access these funds.

You can invest anything from R12,000 a year to R100,000 a year. Be aware that if you invest more than R100,000 per tax year, it will trigger a donations tax of about 20%. This amount is for all your donations, so if you have two grandchildren, you can only donate R50,000 a year to each.

Your options include:

Tax-free investment

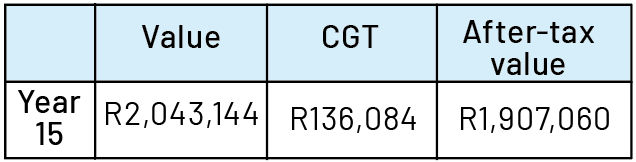

Any person, including a minor, may hold tax-free investments. A parent or legal guardian opens the investment in the child’s name. That’s good for both clarity and estate planning. Keep two limits in mind: the annual contribution cap is R36,000 and the lifetime cap is R500,000 per person.

The big advantage of a tax-free investment is in its name. You don’t pay any tax on the gains in the investment. The longer the investment runs, the greater the capital gains and the more capital gains tax (CGT) you will save. You should therefore use this tax-free investment option only for a long-term investment.

In the table below is an example of investing R3,000 a month until the maximum limit of R500,000 is reached (just short of 15 years). I assumed a return of 10% a year.

Flexible investment

If you’re looking for a shorter-term investment horizon, like giving your grandson a great 21st-birthday gift, then invest in a flexible investment.

By the age of 21, your grandson should not be paying much tax, so the CGT rate will be low.

Retirement annuity

If you want to take full advantage of the R100,000 donations tax, you can contribute an additional R64,000 a year into a retirement annuity (RA) in your grandson’s name. There is merit in doing so, as the growth in an RA is tax-free, and your grandson can’t touch the money before he is 55. This will unlock the full power of compound interest.

For example, if you were to invest R64,000 a year into an RA for your grandson, and only pay this for the 15 years in which you were paying for the tax-free investment, look at the table below to see how much your grandson would receive if the investment returned 10% PA.

Remember, you need to strip out inflation. If we assume an inflation rate of 5%, the value at age 65 would work out to be about R10-million in today’s money.

Remember to set up the investments in the child’s name. This keeps the money separate from your own assets and, in practice, avoids swelling your estate at death. DM

Kenny Meiring is an independent financial adviser. Contact him on 082 856 0348 or at financialwellnesscoach.co.za. Send your questions to kenny.meiring@sfpwealth.co.za

This story first appeared in our weekly Daily Maverick 168 newspaper, which is available countrywide for R35.