From left: Tesla vehicles. (Photo: Justin Sullivan / Getty Images) | Facebook. (Photo: Photo illustration by Chesnot / Getty Images) | The Google logo is reflected a young man’s eye. (Photo: Leon Neal / Getty Images) | Nvidia. (Photo: Justin Sullivan / Getty Images) | Amazon. (Photo: Sean Gallup / Getty Images) | Apple. (Photo: Justin Sullivan / Getty Images) | Microsoft. (Photo: Justin Sullivan / Getty Images)

From left: Tesla vehicles. (Photo: Justin Sullivan / Getty Images) | Facebook. (Photo: Photo illustration by Chesnot / Getty Images) | The Google logo is reflected a young man’s eye. (Photo: Leon Neal / Getty Images) | Nvidia. (Photo: Justin Sullivan / Getty Images) | Amazon. (Photo: Sean Gallup / Getty Images) | Apple. (Photo: Justin Sullivan / Getty Images) | Microsoft. (Photo: Justin Sullivan / Getty Images) I saw my first Akira Kurosawa movie when I was at university. It was called Kagemusha and was fabulous: dramatic and beautifully filmed with a great plot, even if it was a bit hard to follow. Kagemusha is the Japanese term for a political decoy, literally a “shadow warrior”. The movie tells the story of a lower-class criminal who is taught to impersonate the dying lord Takeda Shingen to dissuade opposing lords from attacking the newly vulnerable clan during the Sengoku period of Japanese history.

What a great storyline — amazing that it hasn’t been taken up by Hollywood. But of course, it was Kurosawa’s movie Seven Samurai that Hollywood embraced with a vengeance. There have been two Hollywood blockbusters based on the story of seven warriors who accept a contract to defend a town about to be attacked by bandits.

The first Hollywood version of The Magnificent Seven included an extraordinary ensemble cast of Yul Brynner, Steve McQueen, Charles Bronson, Robert Vaughn, Brad Dexter, James Coburn and Horst Buchholz. The movie spawned three follow-ups and a TV series. The remake in 2016 featured an equally extraordinary cast, including Denzel Washington, Chris Pratt, Ethan Hawke and Peter Sarsgaard. The dialogue was notably better than the previous versions and featured the baddie saying, “Sooner or later, you must answer for every good deed.” One knows how that feels.

The thing about The Magnificent Seven is that it’s structured as both heroic and unlikely. The task is impossible and the seven question why they have taken it on. During a debate on the subject, Pratt’s character says, “You forget one thing. We took a contract.” His fellow warrior says, “It’s sure not the kind any court would enforce.” Pratt replies: “That’s just the kind you’ve got to keep”. Top stuff. He dies. Natch.

The position of the seven samurai is comparable in some ways to what is now being described as the “Magnificent Seven” stocks: Tesla, Meta, Alphabet, Amazon, Apple, Microsoft and Nvidia. They are heroically holding the fort, while the rest of the counters on the S&P 500 languish.

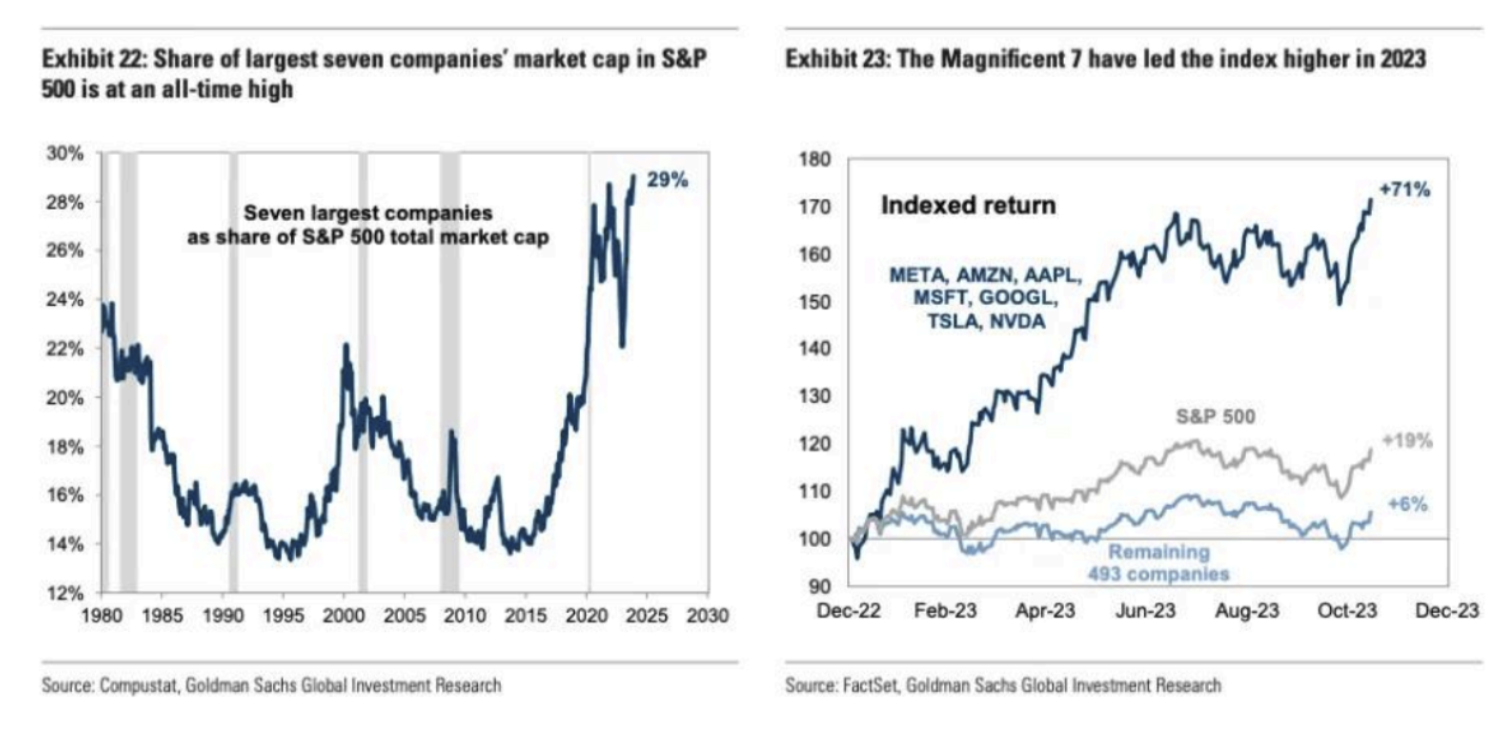

Late last year, the value of these seven stocks made up 29% of the S&P, a level never before reached by seven valuable stocks. At that point, Goldman Sachs research showed the seven had increased in value by 71% over the past year, compared to an 8% return of the remaining 493 companies. Their outperformance was the “defining feature of the equity market in 2023”, the research noted.

The question is, can they keep it up? When things get this out of kilter, they tend to revert to the mean. This past week, several of the Magnificent Seven reported their results, and you know what? They seem to be doing just fine, thank you.

The question is, can they keep it up? When things get this out of kilter, they tend to revert to the mean. This past week, several of the Magnificent Seven reported their results, and you know what? They seem to be doing just fine, thank you.

Microsoft reported $62-billion in revenue, up by 18% year-on-year, and net income of $21.9-billion, up by 33%, its highest profit growth since 2020. Meta jumped by 15% in late trade on strong earnings. The company is making so much money now that it did that shocking thing: it announced an inaugural dividend. Amazon increased by 9% after the bell because its result showed strong sales and it was left to the champion samurai, Apple, to disappoint slightly because of slowing iPhone sales in China.

Overall, the initial signs, at least, suggest that the Magnificent Seven’s story is intact. What’s interesting about the companies is how little they compete with each other; they do of course, but it’s not like the era of the oil companies in the early 2010s when all the oil giants did the same sort of thing. Microsoft is an enterprise software company, Meta is a social network, Amazon is a shop, Nvidia makes chips, Alphabet sells advertising, and so on.

This is good news for investors because it means there aren’t a lot of zero-sum games in the collection where the gains of one will necessarily lead to losses for another. Professional investors are supportive of this view: Mark Haefele, the chief investment officer of UBS Global Wealth Management, told me last week the groups could increase revenue by 50% this year.

“With AI set to remain the key theme driving global tech stocks again this year and likely the rest of the decade, we maintain our preference for the semiconductor and software sectors and see opportunities in those involved in memory and AI edge-computing,” Hafele said, adding there were “compelling disruptive trends”.

At the end of Seven Samurai and the Hollywood versions, some of the seven do die; it adds to the pathos. But generally, the idea is that songs get sung about them for decades to come. Ultimately, I suspect both will happen to these stocks, but in the meantime, don’t get off the horse. DM