Russia President Vladimir Putin arrives to participate in the BRICS Summit dome session in Brasilia, Brazil, 14 November 2019. (Photo: EPA-EFE / Andre Coelho)

Russia President Vladimir Putin arrives to participate in the BRICS Summit dome session in Brasilia, Brazil, 14 November 2019. (Photo: EPA-EFE / Andre Coelho) Most discussions about South Africa’s Russia-leaning, “neutral” stance on the invasion of Ukraine considers in a perambulatory kind of way the potential dangers of alienating the West in favour of an aggressive imperialist — even if that imperialist is allied for the moment with China. There are two points most people seem to be missing.

First, how much the act of leaning toward Russia has affected SA’s economic position right now, today. We are not talking about potential outcomes in the future, we are talking about what is already happening.

Second, the government doesn’t appear to fully appreciate the extent of the dangers constituted by the hand grenade with which it is now playing chicken.

Two reports came out recently that put this all very graphically. The first is the SA Reserve Bank’s financial stability report, which was released last Friday. The report is designed to look at things from a dark point of view to prepare for the worst, but even taking that bias into account, what it suggests really sends shivers down your spine.

For example, it says, if secondary sanctions are imposed on SA, that would “make it impossible to finance any trade or investment flows, or to make or receive any payments from correspondent banks in US dollars”.

Okay, that’s bad enough, but the report goes on to say, “There is also the risk that such sanctions could be expanded to include payments in EUR or GBP. This will be catastrophic for the South African economy and has the undeniable potential to trigger a financial crisis.”

It goes on to discuss various problems, but also points out that SA, “is already plagued by foreign investment outflows as a result of its weak economic conditions and the recent FATF greylisting. Jeopardising remaining investment inflows, which come predominantly from the US, EU, and UK, could therefore lead to financial instability.”

And all of that is only one aspect of the financial stability issue. It also mentions trade, as many reports have already discussed, but there are other potential problems too, including term finance, SA’s foreign reserves and foreign direct investment. The report points out that as at 31 December 2022, 82.5% of foreign direct investment into South Africa originated from the US, EU, and UK, compared to 0.003% from Russia.

It’s plainly obvious if you read the report that the Reserve Bank, no less, is freaked out by the direction SA is taking by cuddling up with the bear. I suspect that SA’s politicians might think, well, sanctions have been imposed on Russia, and they don’t look that bad.

But the problem is that SA’s economic position and Russia’s economic position are not really comparable, because Russia’s oil and gas exports underpin its economy in a way that SA’s mineral wealth does not.

Russia’s pre-invasion income from oil and gas was about $132-billion, and because the world needs this resource so badly, Russia has managed to maintain this economic underpin somewhat, albeit at a lower rate. SA’s total mineral exports, by comparison, are less than a quarter of that, and really don’t constitute resources that the world needs in the same way it needs oil and gas. As for the rest of SA’s exports, alternatives abound.

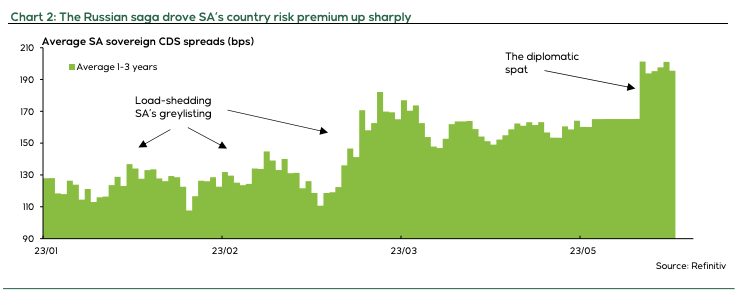

The immediate, financial effect of SA’s diplomatic gamesmanship was illustrated by a report Nedbank issued this week called The Cost of the Russia Saga. It’s difficult to separate SA’s continuing Eskom woes, rising interest rates, and the “Russia Saga” from each other, but one thing the Nedbank report notes is the sudden increase in the average SA sovereign credit default swap spreads.

Credit default swaps are essentially the cost of insurance debt investors have to pay to insure their bond investments against the potential of default. In the same way that you would have to pay more for your car insurance if you have the completely understandable tendency to drink and drive, so the measure of insurance cost is a good indicator of risk.

The interesting thing about these credit default swaps is that they jumped — I mean really jumped — not in unison now with the rand decline or the interest rate increases, but with the Lady R allegations and revelations.

Of course, once things like that get into the market, further pieces of incremental bad news have a disproportionate effect — hence the rand’s continuing decline, for one thing. There has been some retraction by the SA government in its bear cuddling, as the Nedbank report points out. But the vocal concerns of the International Criminal Court have kept the issue at the front of the news — not just here — and the confusing approach is not helping.

All in all, a more ill-considered, ham-fisted, bungled approach is hard to imagine. DM