(Image: iStock)

(Image: iStock) First National Bank chief economist Mamello Matikinca-Ngwenya says the hike was not unexpected but means the Monetary Policy Committee has now “unleashed 475 bps worth of hikes cumulatively over its 10 meetings since November 2021.

“Further intensification of load shedding this winter exacerbates upside risk to inflation, and the upward pressure on interest rates is not fully neutralised,” she says.

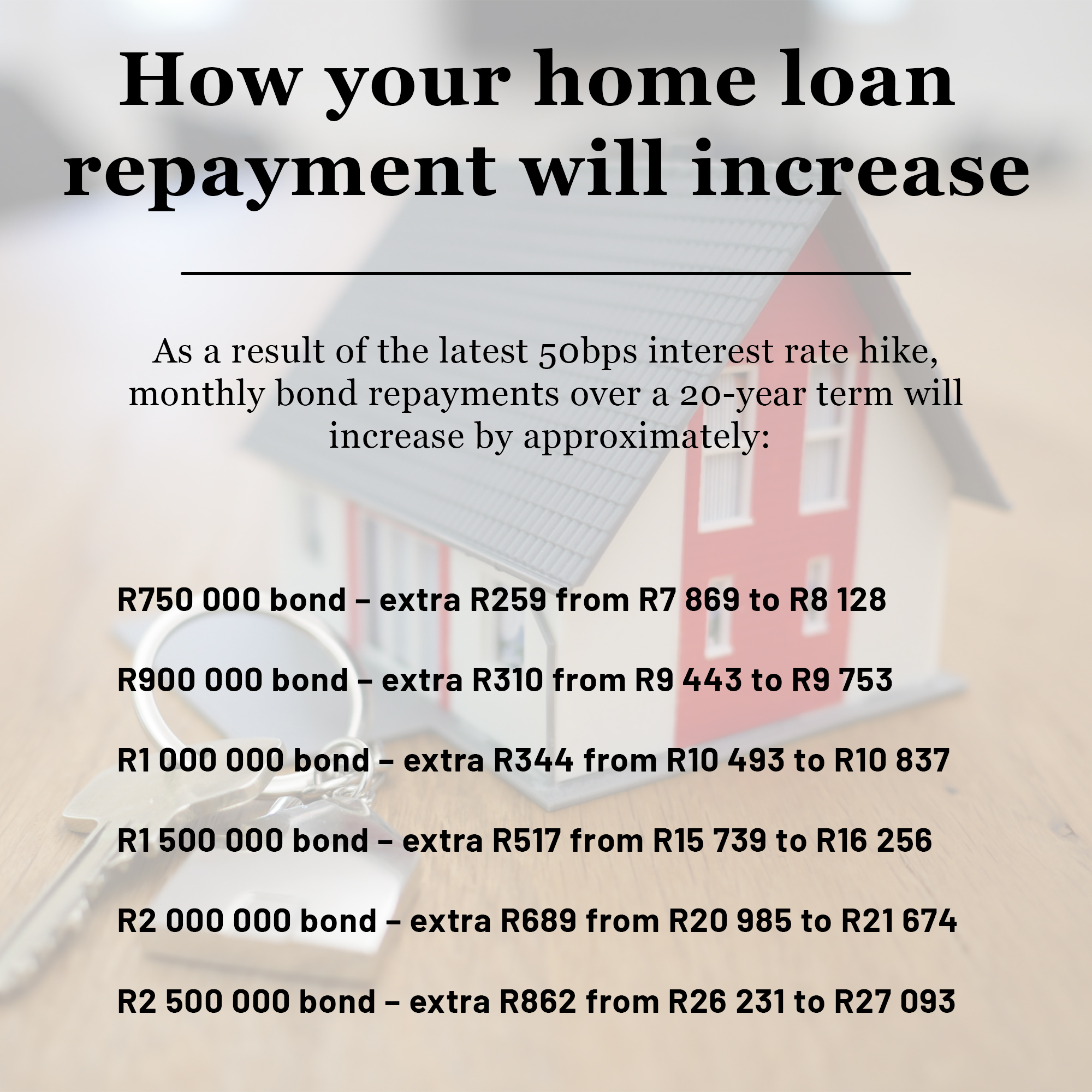

Homeowners with property bonds are also expected to absorb significant pain.

Samuel Seeff, chairman of the Seeff Property Group, says the rate hike is a killjoy for the struggling economy.

“The rapidly rising borrowing cost has put a dampener on the market. First-time homebuyers, many from the emerging middle class, are facing affordability challenges, and overall sales volumes have declined, more in some areas and to a lesser degree in other markets such as the Cape,” he says.

However, he notes that South Africans are still seeing the best lending conditions since 2007, with strong support from the banks.

“Approval rates are still at over 80%, deposit requirements still at around 8%-10%, and buyers can often find a rate concession,” he says.

Seefff advises potential buyers to apply for a “prequalification” so that they are in a better negotiating position, while sellers should note that house price growth has stalled, which means they need to price correctly if they are looking to sell right now.

John Loos, property sector strategist at FNB Commercial Property Finance, says the rate hike will directly impact consumers’ disposable income, along with the impact of the higher inflation that caused the rate hike.

“On the residential development side of the market, new building planning has already been declining and this latest rate hike will probably reinforce that declining trend. On the residential rental market side, earlier interest rate hikes gave some mild support to the rental market, as aspirant buyers postponed their home-buying and remained in the rental market for longer.

“But given the increasingly severe magnitude of interest rate hiking since late-2021, we believe that the earlier recovery in the rental market may now stall, with the tenant population beginning to experience increased financial pressure in a significantly weaker economic environment,” he says.

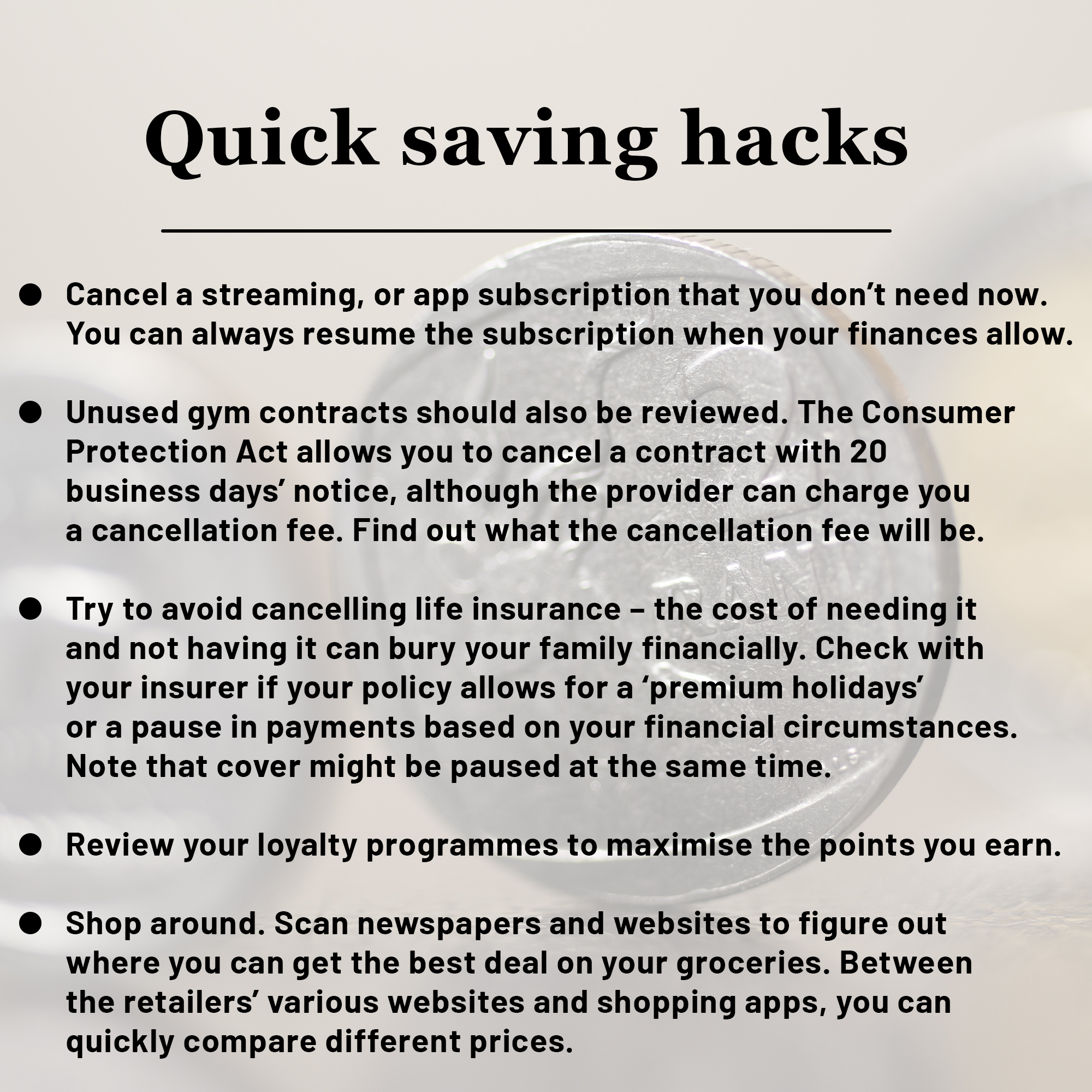

Lizl Budhram, head of advice at Old Mutual Personal Finance, advises consumers to carefully assess areas where they can safely cut expenses before cancelling or reducing insurance or savings policies, as these choices can have serious long-term financial consequences.

“At this stage of the fight, no household should be without a budget spreadsheet that is regularly revisited, as it is the only way of ensuring that you make informed, sensible and intentional decisions of where to continue spending and where to reduce or stop spending,” she says.

Budhram says consumers need to show a greater awareness of inflation risk on their plans. Inflation chips away at your savings by reducing the amount of goods and services you can buy with each rand over time.

For example, assuming a loaf of bread costs R20 and inflation is at 10% per annum: next year, your R20 buys nine-tenths of a loaf; less than two-thirds of a loaf in five years, and about two-fifths of a loaf in 10 years.

“You must work with your financial adviser to ensure that your investments are outpacing inflation by an adequate margin and that your asset allocation is suitable for both inflation and volatility risk,” she says. DM