(Photo: Chris Ratcliffe / Bloomberg via Getty Images)

(Photo: Chris Ratcliffe / Bloomberg via Getty Images) The rand this week began a fresh slide and remains at its lowest levels against the dollar in more than two years, when the economy was in full pandemic meltdown.

On Monday, it hit almost 17.80/$ at one point and was hovering around 17.75/$ in late Tuesday trade. If it went to 18/$ it would break what forex dealers call a “psychological level.” Such levels — typically round numbers — are also often “technical” as they represent a number that triggers buying or selling.

In fairness to the rand, it is not the only currency that has been losing ground to the greenback as the US Federal Reserve aggressively hikes interest rates to contain surging inflation in the world’s largest economy. As my colleague Tim Cohen noted in a recent column that also involved milkshakes, the UK pound, Japanese yen and Euro are all near multi-decade lows against a resurgent dollar.

Read more in Daily Maverick: “The rand and the very long straw milkshake theory of the US dollar”

This is in part because of the pace of “monetary normalisation” in the US, to use the current jargon. The US central bank’s Federal Open Market Committee (FOMC) hiked federal fund rates by 25 basis points in March this year, 50 basis points in May and 75 basis points at its June and July meetings. That took the benchmark federal fund rate from almost nothing to 2.25% to 2.50% and another 75 basis point hike is on the cards on Wednesday when the FOMC’s next meeting wraps up.

“Financial markets have started to factor in more than a 75 basis point hike in the US, which has negatively affected risk sentiment, causing the rand to weaken towards R18.00/USD on substantial US dollar strength, with the dollar breaching parity with the euro already in August,” Investec economist Annabel Bishop said in a note this week.

Among other things this is forcing the hand of the South African Reserve Bank (SARB), which has lifted its key repo rate by 200 basis points since November of last year from record lows to 5.5%, bringing the prime lending rate for consumers to 9.0%. The SARB is widely forecast to raise the repo again by 50 to 75 basis points when its Monetary Policy Committee (MPC) concludes its meeting on Thursday, 22 September.

Read more in Daily Maverick: “SA Reserve Bank to hike rates again this week to contain inflation, support rand”

Like the US Fed, the SARB has a hawk eye on inflation. And as of late, US inflation has been outpacing South Africa’s. The US consumer inflation rate in August was running at 8.3% compared with 7.8% for South Africa in July. South Africa’s August CPI number will be released Wednesday morning and will provide a better comparison.

Visit Daily Maverick's home page for more news, analysis and investigations

Some analysts would argue that in such a situation, the rand should be gaining ground on the greenback as inflation decreases the purchasing power of money. There is a reason why hyperinflation is linked to currencies with lots of zeros — look at Zimbabwe in recent years or Germany’s Weimar Republic in 1923.

But rand fragility is not just a consequence of contrasting interest and inflation rates. South Africa’s current account surplus unexpectedly slid into a deficit in the second quarter on cooling commodity prices and an upsurge in dividend outflows

Read more in Daily Maverick: “SA’s current account balance falls into the red, bad news for the rand”

That has removed a key base of support which was helping to prop up the currency as it signalled that more capital was flowing into South Africa than flowing out — a positive trend that has now been reversed.

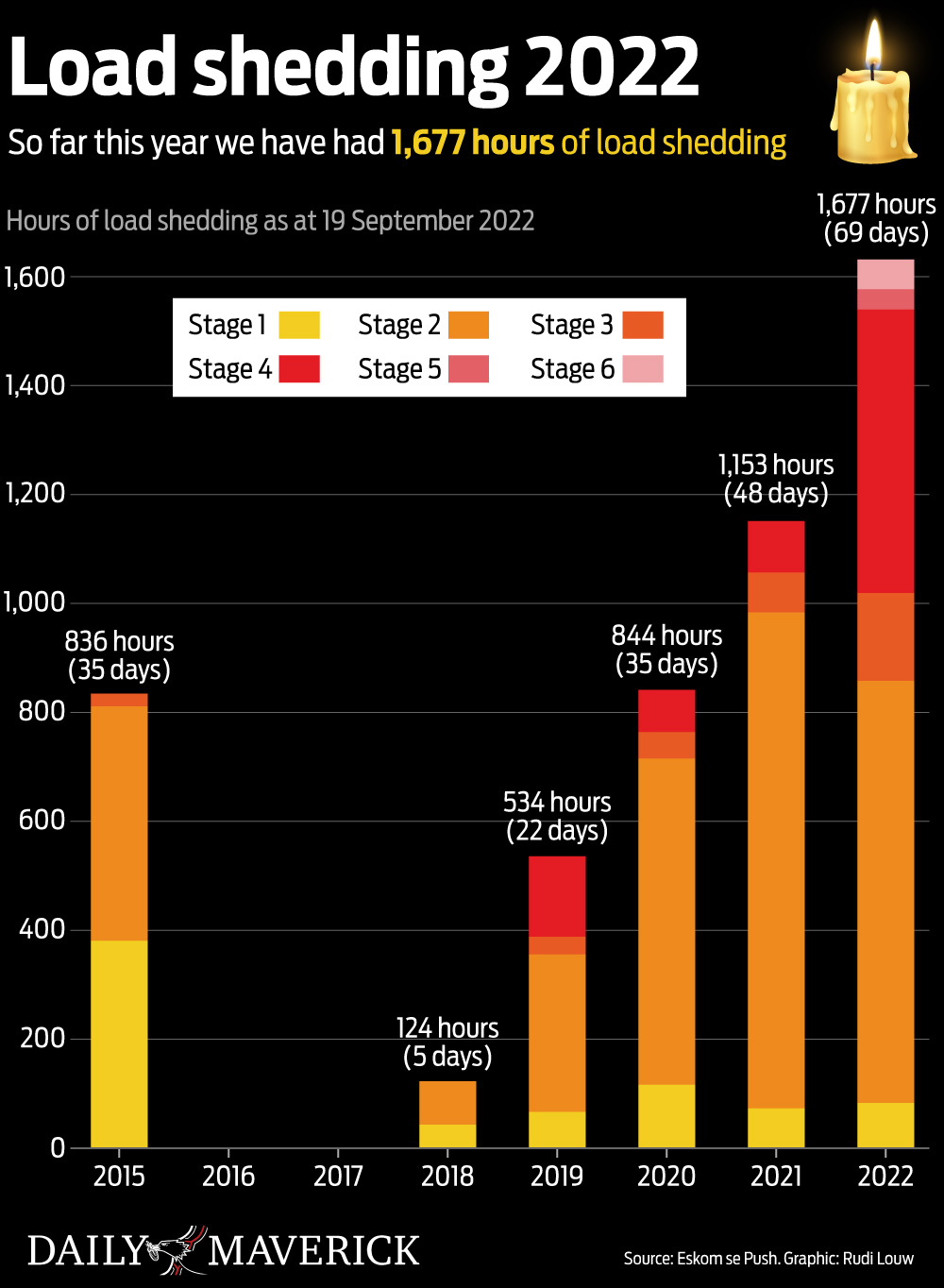

Ultimately, the rand is a reflection of investor confidence — or lack thereof — in the economy, and its moves early this week were also triggered by Stage 6 rolling blackouts. And the currency’s long-term trajectory has simply been dire: in 1995 it was fetching under 4/$. The yen, the pound, and the euro have all been depreciating against the dollar of late, but few currencies have had a long-term decline on that kind of scale. Examples would include the worthless currency north of the Limpopo which should serve as a stark warning to the economic populists — or fabulists — in the ANC.

Rolling blackouts are one of the trends lighting the way to the rand’s demise over the ANC’s pot-holed road to economic ruin. Africa’s most industrialised economy is now probably its most rapidly de-industrialising economy. The rand’s performance over the past couple of decades has been emblematic of this state of affairs.

There had been hopes that South Africa’s economy might dodge a recession after contracting 0.7% in Q2 — which pushed gross domestic product back below pre-pandemic levels — with some signs of tepid growth this quarter. But the current round of rolling blackouts in the final fortnight of this quarter increases the prospects of a second consecutive quarterly economic contraction, which would mean yet another recession.

One of the depressing things at play here is that rolling blackouts also seem to intensify when there are signs of economic growth. The grid simply cannot cope with a bigger economy, which in turn puts paid to prospects for growth, in a vicious cycle. When Eskom actually keeps the lights on these days it’s probably a signal that the economy is tanking — a lose-lose situation.

So the rand at the moment does not have a lot going for it. It might survive this week without plunging and may not be staring into the abyss over the short run, but the long-term trend is downhill. And that mirrors the dimming state of an economy which cannot keep the lights on. DM/BM