(Photo: Dwayne Senior / Bloomberg via Getty Images) | Adobe Stock)

(Photo: Dwayne Senior / Bloomberg via Getty Images) | Adobe Stock) The eyes of pensioners are watering as the rout of JSE giants Naspers and Prosus accelerates into an epic free fall.

A year ago the high-flying tech stocks tipped R3,834.86 and R1,856.33, respectively. Today Naspers is priced at R1,414.20 and Prosus R683.53, a 63% decline on both counts. In the process, Naspers’ infamous discount to underlying assets has widened to about 60%. And it’s not clear that the stocks have reached their floor.

What has accelerated the fall in recent days is a perfect storm of bad news, almost all of it related to China and Chinese tech stocks overall. Tencent, in which Prosus holds a 28.9% stake, has been caught in the storm and has fallen by 37% in the last month and 52% in the last year.

Triggering the rout was the Wall Street Journal report that Tencent is facing a potential fine for non-compliance with know-your-customer rules, and because users were able to transfer funds on its WeChat platform for illicit purposes. This makes it just the latest victim in China’s year-long regulatory crackdown on its tech sector.

“The market reaction wiped billions off Tencent’s market cap, which is out of proportion to the size of any potential fine,” says Peter Armitage, CEO of Anchor Capital.

“Even though the news out of China is concerning, what we are seeing is a delinking of share prices and fundamentals,” Armitage adds.

The country is experiencing an Omicron outbreak, and therefore the government has locked down several key cities, including technology hub Shenzhen, a move that is likely to slow an already slowing Chinese economy.

Investors are also nervous about China’s ties to Russia, and the possibility that closer ties between the two countries could trigger US sanctions, impacting many high-flying Chinese tech stocks.

The Golden Dragon Index, which tracks Chinese American Depository Receipts, is down over 70% over the last year, but 24% over the last five days, which is unheard of. This Chinese tech rout has been described as the worst since the global financial crisis, says Andrew Dittberner, CIO at Old Mutual Wealth Private Client Securities.

Fuelling the rout was the Securities and Exchange Commission (SEC) identification of five companies that are at risk of being delisted if they fail to comply with certain auditing requirements.

“This is despite the Chinese securities regulator saying it will cooperate with the SEC,” he says.

The second reason was JPMorgan downgrading the target prices of 28 Chinese tech companies (including Tencent). JPMorgan believes investors should avoid Chinese tech stocks on a 6-12 month view, given that sentiment and technical trading are driving the market. However, Dittberner argues that sanity should prevail.

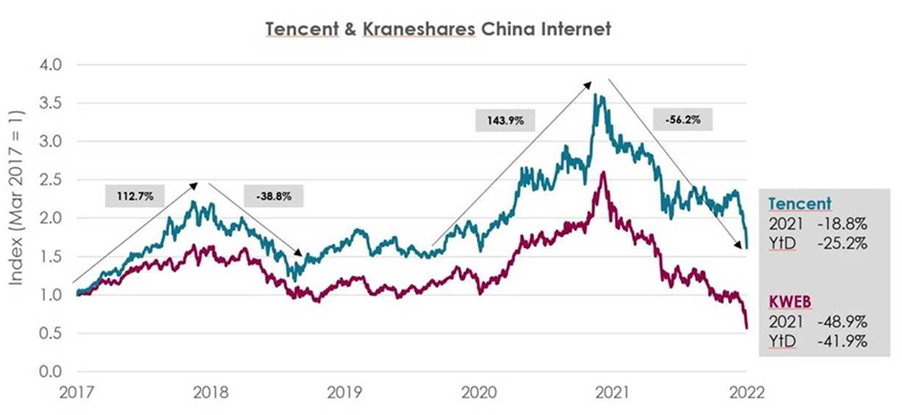

“We have been here before,” he says. “Through the course of 2018, Tencent sold off significantly due to the regulatory body not granting licences. After an extended period of drawdowns that lasted just short of a year, Tencent did recover.”

The graph below maps Tencent against its peer group, Kraneshares CSI China Internet ETF, and depicts this point.

“While acknowledging the risks from a regulatory and geopolitical perspective, we do not believe that Tencent should be trading on such depressed multiples, nor do we believe that Tencent is going to zero,” he says.

There is significant balance sheet headroom at both Tencent and Prosus to weather the current risk-off sentiment. However, given the current global environment, it is unlikely to be a smooth ride.

And that is exactly what worries some investors. Is the fall in the price of Tencent, Naspers and Prosus simply a case of tech companies being caught in a tsunami of bad news, or is that a convenient cover-up for a more fundamental problem?

Pieter Hundersmarck, Global Multi-Asset Portfolio Manager at Flagship Asset Management, believes the problems at Naspers go beyond the current geopolitical tensions and Chinese regulatory zeal – although neither are to be ignored.

In fact, he says the problem lies with a management team that believes it can play in a highly competitive internet environment and replicate what was an enormously prescient investment made by the previous management when, actually, the facts on the table suggest they cannot.

“What began as a scrappy emerging markets technology investor, leveraging a South African asset base by making bets on the future of the internet in emerging markets, has mutated into a tortured hybrid holding company that seemingly exists largely to provide ‘turf’ and enrichment for management at the expense of shareholders,” he says bluntly.

Pushed out of the bigger markets occupied by the largest and most connected venture capital firms, Naspers has been forced to concentrate its bets in peripheral – and higher risk – areas like emerging markets’ classifieds and food delivery, he says.

And while some sectors, like classifieds, have matured into a profitable sector, Hundersmarck questions whether the company’s enormous bet on food delivery will ever deliver? The problem is that food delivery isn’t obviously scalable. Also, it’s essentially a commodity, enjoying little to no brand loyalty. And, alarmingly, while grocery delivery is being touted as the new add-on to this business, the economics are worse.

“In hindsight, the risks in Naspers were always high, but we just got more accustomed to them as time went by.”

These extend from the assets – the funding thereof – to the discount that never narrows, and a management team that is unable to act in the best interest of shareholders. More recently, concerns about the Chinese government’s rumbles about foreign shareholding have rung alarm bells.

“The probability of Tencent no longer being a commercially directed enterprise, or being able to have non-Chinese ownership, are becoming less remote.

“They are now most certainly a non-zero probability and there is serious fear in the share price as investors have now woken up to that non-zero possibility. This mindset change is likely structural.” BM/DM

[hearken id="daily-maverick/9284"]