Chinese banks in January extended a record amount of loans after the PBOC lowered borrowing costs for the first time since 2020 last month. The latest move, seen as a prelude by many to further easing, comes as the economy struggles with repeated Covid outbreaks, a slowdown in the property sector and signs of weak domestic demand.

“This sends the signal from the PBOC that it’s still willing to keep liquidity conditions quite ample and market rates at relatively low level to support credit demand,” said Xiaojia Zhi, economist at Credit Agricole CIB in Hong Kong. “There is room for further policy actions in 1H, including both RRR and policy rate cuts, as growth pressures remain, especially in the property sector and related to private consumption demand.”

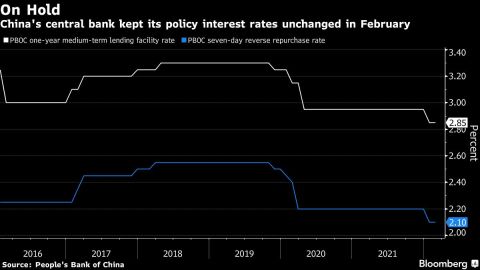

Sixteen of the 27 economists polled by Bloomberg saw the central bank keeping the interest rate on its one-year policy loans unchanged, with most saying the PBOC can afford to wait and see whether earlier easing measures are taking effect.

In January, the central bank cut the rate on its one-year policy loans by 10 basis points to 2.85%, the first reduction since April 2020.

Still, there’s a growing chorus of economists and investors calling for more support, with Citic Securities Co. saying that a cut in the reserve requirement ratio for banks could be seen as early as March. In its quarterly report last week, the PBOC pledged to keep its monetary action “ample, targeted and front-loaded.”

What Bloomberg Economics Says…

The People’s Bank of China is catching its breath after it cut the one-year medium-term lending facility rate last month — the pause won’t last long. The central bank has signaled it’s ready to deliver more support to prop up growth. We expect the next cut as soon as the second quarter, and see the PBOC delivering another one in 3Q — part of a broader array of easing measures to counter the slowdown.

–David Qu and Chang Shu, China economists

For the full report, click here

Despite the decision to hold the one-year policy loan rate steady Tuesday, the PBOC’s easing stance has set it apart from other major central banks including the Federal Reserve, which are tightening monetary policy to tame soaring inflation. The possibility that the Fed will accelerate the pace of rate hikes could restrict China’s room for further easing later this year as it could accelerate outflows.

Global demand for Chinese bonds has already slipped amid their shrinking yield premium. The yield gap on China’s 10-year sovereign bonds over similar-maturity Treasuries narrowed to 73 basis points last week, the least since 2019.

“Added liquidity in MLF with the rate unchanged is consistent with the easing signal released by the PBOC in its quarterly monetary policy report,” said Bruce Pang, head of macro and strategy research at China Renaissance Securities Hong Kong Ltd. “It’s still possible for the PBOC to cut interest rates and the RRR, but it may need some time before that to evaluate the effect of its previous actions.”

–With assistance from Shikhar Balwani and Jing Zhao.

Comments - Please login in order to comment.