(Image: Adobe Stock)

(Image: Adobe Stock) All eyes are on the medium-term budget this week, but it is a possible increase in South Africa’s repo rate next week that could have more profound implications for the domestic economy in the next three to five years if, like other emerging markets, it does take the first step on to an emerging market rate hiking cycle.

Emerging markets like Brazil, Argentina and, earlier in the pandemic, Turkey, have been aggressively hiking interest rates to thwart sharply rising inflation and others, including, it seems, South Africa, look set to join them if the financial market pricing is on the mark. Fixed-income investors are anticipating rate hikes in Asia and central bankers in eastern European countries recently shocked investors with the extent of the rate hikes they introduced.

Investec economist Annabel Bishop foresees the SA Reserve Bank (Sarb) raising the repo rate by 25 basis points at next week’s Monetary Policy Committee meeting, in line with what the fixed-income market is currently pricing in.

However, she adds: “Sarb has sent mixed signals on SA’s monetary policy, shifting with the tides of waxing and waning inflation, the impact of the July riots on confidence and growth and as monetary policy authorities’ tones shift globally.”

More worrying, Bishop says if Sarb wants to normalise monetary policy in line with its inflation target, SA’s repo rate would need to rise to 6.5% from its current 3.5%. It’s not surprising that the central bank is treading carefully. It has an extremely challenging job at a time when inflation is rising globally and the looting and riots and load shedding are taking their toll on an economy still bearing the scars of the pandemic .

However, SA Reserve Bank Governor Lesetja Kganyago has made it clear many times that it’s not the central bank’s job to revive the economy – which means he will do what needs to be done to contain inflation.

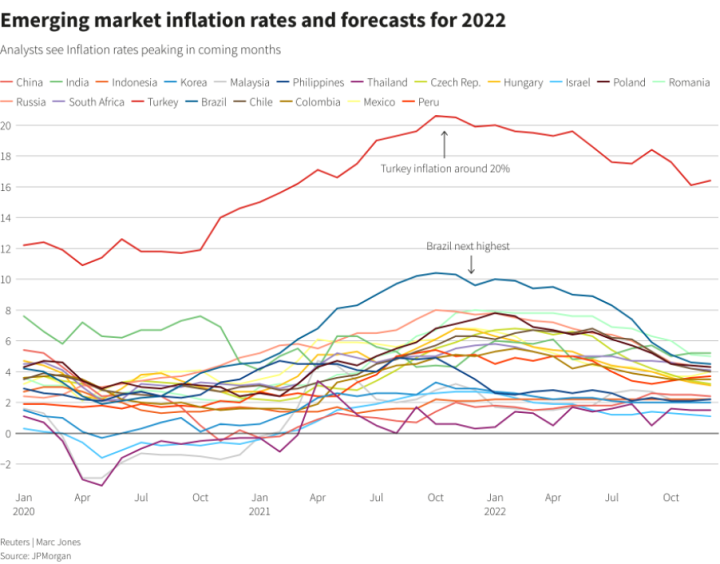

That’s not the case in Turkey, where President Recep Tayyip Erdogan has decisively turned his back on the prevailing macroeconomic wisdom that inflation can only be contained if central banks maintain their independence. On numerous occasions he has asserted his control over the bank, most recently firing three monetary policy committee members in October. He’s also orchestrated the reversal of previous interest rate hikes put in place to stem the tide of rising prices.

The country has paid the price for this, with the Turkish lira plummeting this year and the bank recently updating its 2021 year-end inflation rate forecast to 18.4%, substantially higher than 14.1% expected previously.

In the developed world, some central banks, barring the European Central Bank, have taken a mildly hawkish turn, but they are still likely to remain reticent in aggressively hiking interest rates, still convinced that higher inflation rates will prove transitory and dissipate by mid next year.

Last week, the Federal Reserve began its tapering programme as expected, but chair Jerome Powell emphasised that the required conditions for an interest rate hike would be more stringent than those that have facilitated the gradual withdrawal of quantitative easing.

Bishop aptly points out that global monetary policy is becoming unsynchronised, “led by some EM countries”. However, she adds that recent events show that, globally, easy money policy has begun to retreat. But it will be some time before we are likely to see any narrowing in the gap between the rate hiking trajectories of emerging markets and developed countries.

The graph below shows inflation rates in emerging markets since the beginning of 2020 and JP Morgan’s forecasts for emerging market inflation rates over the next year.

It’s little wonder that emerging markets are increasing interest rates at pace. AMP Capital analysis based on Bank of International Settlements data shows more than half (52%) of emerging market central banks hiking rates in October versus almost a third (31%) in developed markets (see graph below).

The firm expects the gap to rise even further in November after Poland shocked the world by announcing a 75 basis point increase, and the Czech National Bank by an even more aggressive 125 basis points.

/file/dailymaverick/wp-content/uploads/2021/11/image2-1.jpg "(Source: BIS, AMP Capital)")

Meanwhile, it could be some time before we see the end of this inflation and rate hiking cycle, if JP Morgan Asset Management’s expectations prove to be true.

In its 2022 Long-Term Capital Market Assumptions, the investment manager predicts that global inflation will “stick”, saying: “In the developed world, powerful long-term economic forces have suppressed inflation, and these forces have been supplemented in emerging markets by more responsible central bank policies. However, after the Covid-19 recession, we expect aggressive fiscal policy and a faster recovery to carve out a somewhat stronger path for inflation globally over the next 10 to 15 years.”

It identifies the following as forces likely to support inflation:

- Political populism resulting in more aggressive fiscal stimulus;

- Stalling globalisation;

- Higher minimum wages and more generous unemployment benefits;

- Climate change efforts if they include carbon taxes.

The most worrying aspect of the tide of rising interest rates in emerging markets is the impact this will have on governments’ funding rates after racking up huge government deficits in their efforts to quell the impact of the pandemic on their countries. Efforts to find their fiscal equilibriums will make it that much harder for these economies to achieve pre-pandemic growth rates.

McKinsey Global Institute’s October Global Economics Intelligence analysis says the cost of capital for governments has already been driven up by higher inflation over the last few weeks.

Brazil, weighed down by a mammoth fiscal deficit, is also having to contend with the aggressive rate hikes implemented by the central bank, the latest of which was the largest in two decades, according to McKinsey. The 150 basis point hike took the country’s official interest rate up to 7.75% – 50 basis points more than expected.

Fortunately, South Africa is nowhere near to being in the same situation as Latin America’s largest economy. But government and the Reserve Bank will be hard pressed to achieve a policy balance that sets South Africa on a sustainable growth path, allowing the country to recoup the economic losses inflicted on it by Covid-19 and achieve the sustainable growth that was out of reach even before the pandemic hit. BM/DM