New York Stock Exchange traders as the country awaits the results of the 2020 presidential elections. (Photo: EPA-EFE/COURTNEY CROW HANDOUT)

New York Stock Exchange traders as the country awaits the results of the 2020 presidential elections. (Photo: EPA-EFE/COURTNEY CROW HANDOUT) The roller coaster ride that has been 2020 is no better reflected than in the equity market, which has achieved record highs in the US but also plumbed bear market depths globally in March before mounting a steady recovery for the ensuing five months.

For much of the year, the prevailing concern has been the increasing divergence of the US stock market from the difficult economic realities as a result of the coronavirus crisis. In September, it appeared that reality was at last catching up but stock markets rebounded again into October when the S&P 500 Index almost reached its September record high again.

However, the rally was soon cut short by the new waves of Covid-19 infections, the devastating implications these could have on recovering, yet still extremely fragile, economies and pre-US election jitters.

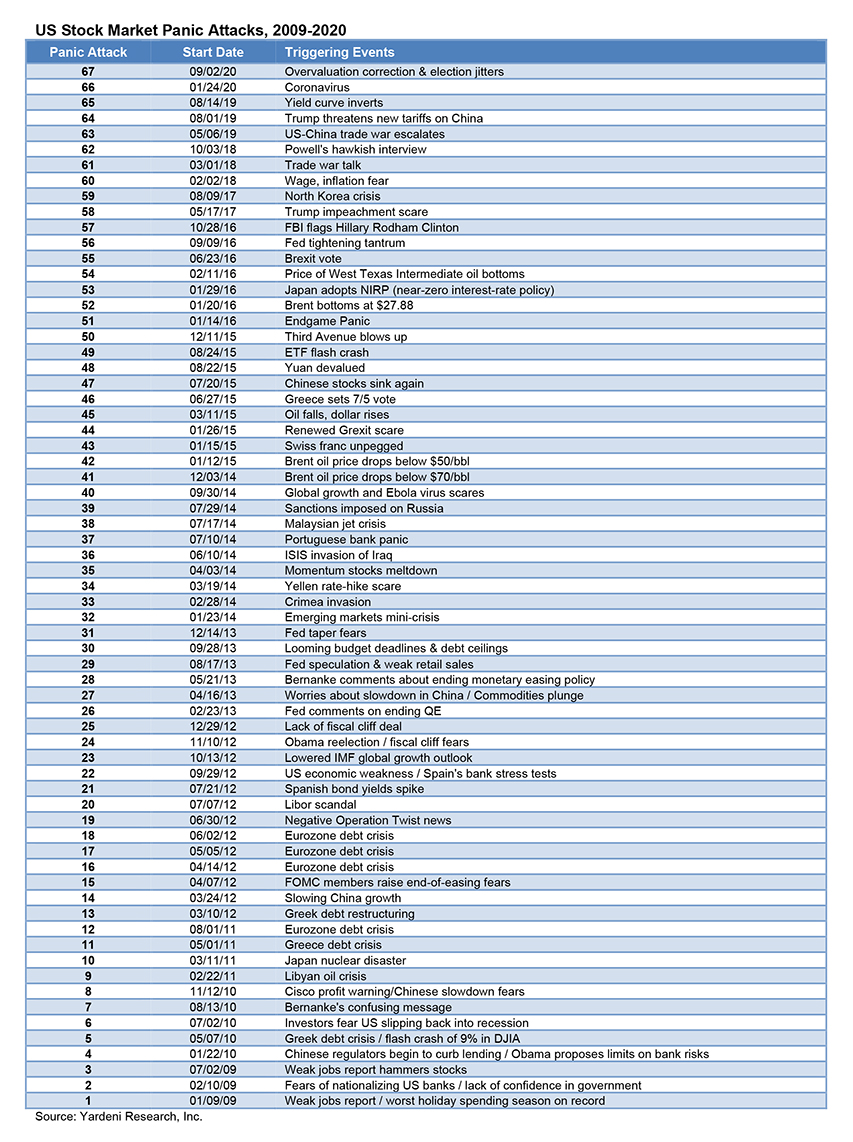

Ed Yardeni has tracked the path of the stock markets for decades and has identified the many “panic attacks” that have sent equities tumbling. He puts the number of panic attacks since the financial crisis at 67, of which there have been two this year, namely the onset of the coronavirus in the first quarter and then what he calls an overvaluation correction, combined with election jitters, in early September (see the table below).

Within the next week, we will know whether the US elections are the third panic attack of the year. It didn’t look like it the day of the election, as stocks rallied after pulling back into month-end. However, most institutional investors were still unwilling to take a bet on the outcome, given the 2016 shock election result, and maintained their wait-and-see approach.

There is an emerging view, however, that investors are gearing up for a rotation out of the big US tech stocks that have underpinned the surprisingly strong equity market performance this year and into other geographic and market segments that have more to offer.

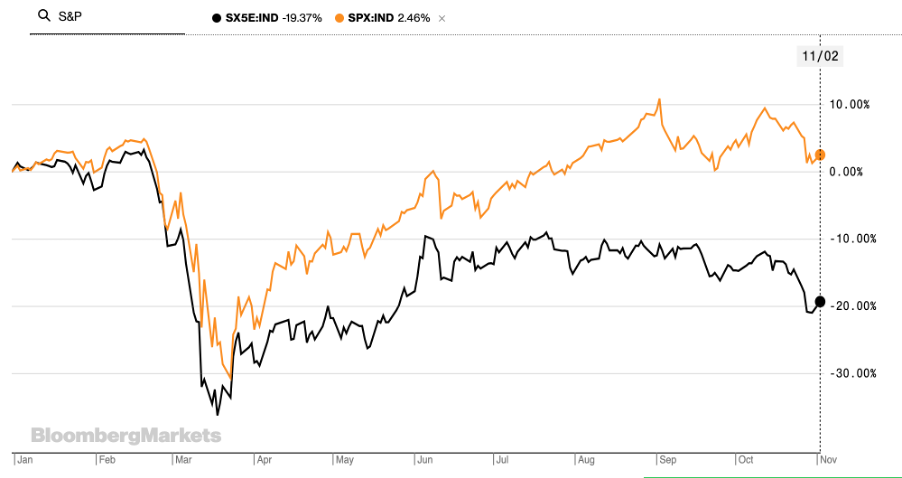

A lot of attention has been given to the bifurcation of the US tech stocks and the rest of the counters listed on the stock market. However, the divergent performance between the US and Europe has been extreme, as shown in the graph below. In fact, over a 12-month period, the MSCI North America Index has gained about 10% and the MSCI Europe Index has fallen 10%.

S&P 500 far outpaces the EuroStoxx Index

Schroders Quantitative Equity Product fund manager Daniel Woodbridge believes that after the extended outperformance of US growth stocks, this may be “not the worst time” to consider diversifying outside the US. Instead of trying to predict the future but remembering lessons from the past, Woodbridge says: “It may not seem like it right now but international equities have regularly outperformed the US for significant periods of time. They also offer diversification.”

Among the reasons for diversifying now are that US megacap tech stocks are “richly” valued and vulnerable to disappointment; something we saw in the latest earnings guidance of the big tech companies. Also international equities, particularly value stocks, “are offering record discounts to their benchmarks and appear to be in a zone that could be considered mispriced”.

It lists a variety of reasons to diversify internationally, including the usual suspects like getting broader regional and geopolitical exposure and access to faster-growing populations in Asia and other emerging markets.

Most compelling currently, however, are the following:

- Valuations are far more attractive, “even when adjusted for comparably lower growth rates”.

- International diversification comes with exposure to other currencies, particularly given the dollar seems to have reached a plateau and may weaken from here.

- Investors get exposure to less concentrated markets and greater opportunities for active investors.

JP Morgan Asset Management global head of equities Paul Quinsee agrees there is a good chance that there will be better returns from a wider range of stocks because valuations do vary so much. “As the perceived winners have gotten expensive, though still supported by strong growth, we think investors should balance their portfolios and look for opportunities elsewhere in less expensive companies poised to benefit from a rebound in economic activity.”

Quinsee adds that his investors think the best of the market recovery is behind us and that few of them “see supercharged returns from here”. But he notes that it is difficult to be too cautious because the stock market stands to benefit from the highly supportive monetary conditions and optimism about a medical solution to the virus. Against this backdrop, he says the big debate in his team is about stock selection rather than market direction.

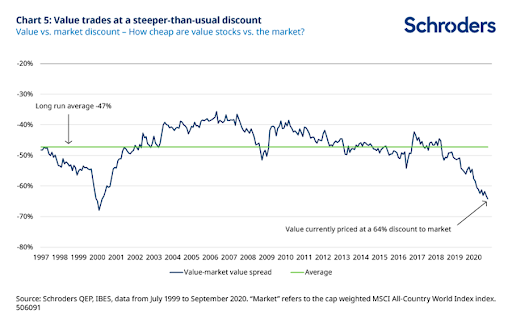

If stock selection is the way to go, Schroders says it may be the time to take advantage of the substantial valuation gap between value stocks and the overall market – and international value stocks not just US value stocks.

The graph below shows the extent of the discount of value stocks relative to the market (-64%) compared with the long-term average (-47%).

Schroders points out that the last time the discount was so significant was in late 1999/early 2000 during the height of the dotcom boom. “This isn’t to argue that value is necessarily poised for a multiyear rally as in the early 2000s, but the pattern is worth noting.”

The global wealth manager also claims that value investing works better in international markets, instead of choosing to buy value shares in the US. The graph below shows that while US value shares underperformed growth by almost 3% a year over the period, value shares outside the US outperformed growth by 0.6%.

Though the same experience may not be repeated, Schroders believes that ex-US equities “could be an interesting space to add exposure” and that considering international value-style equities would also allow you to “diversify away from the rich valuations of the US market and declining US dollar”.

While what lies ahead for us from a global political and health perspective may be unpredictable, there are certain underlying realities in stock markets that history has shown us they do eventually reassert themselves – often taking investors by surprise. With that in mind, the arguments in favour of international diversification and taking advantage of the compelling valuations offered by currently unfavoured shares are convincing ones. BM/DM