The Big Four banks. (Photos: Nadine Hutton/Bloomberg via Getty Images) / Gallo Images/ Papi Moake) / Gallo Images/Fani Mahuntsi) / Gallo Images/Papi Morake)

The Big Four banks. (Photos: Nadine Hutton/Bloomberg via Getty Images) / Gallo Images/ Papi Moake) / Gallo Images/Fani Mahuntsi) / Gallo Images/Papi Morake) The share prices of SA’s major banks have been moving upwards over the past weeks; not much, but some. You can almost hear the sigh of relief in the background.

The hurricane that has been a stunted economy in crisis has passed over and banks have come out on the other side battered and bruised, but still standing. And now a new narrative is emerging: can we foresee some big jumps in the near future?

Banks, especially big ones, are essentially an indication of the state of the economy – except for one crucial difference; they need to retain the confidence of their clients. This is because their essential business model is to borrow short and lend long, and that means they are always, and by definition, vulnerable.

In the situation of economic crisis, or even sometimes weirdly in times of economic boom, a nightmare scenario hovers like a vindictive ghost over the shoulders of commercial bankers.

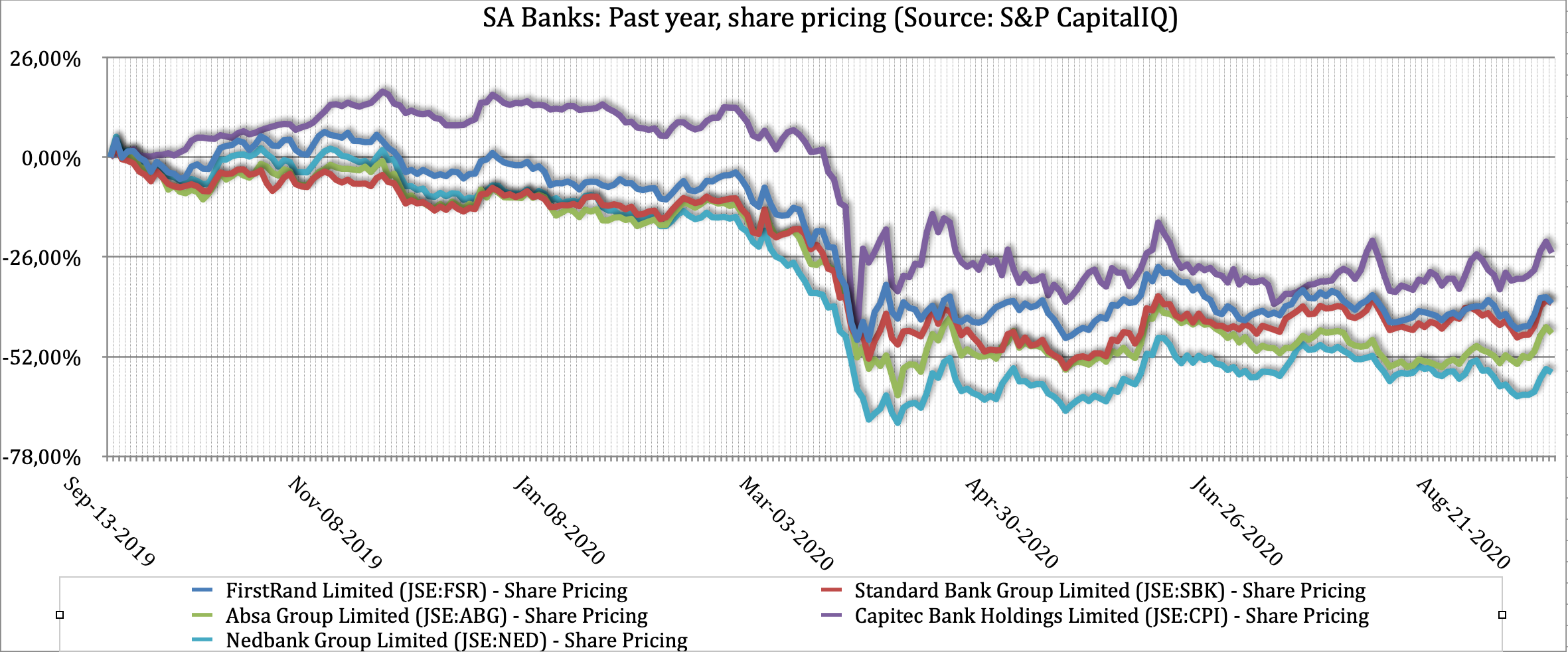

Yet, we have now seen the results either for the past six months or the whole financial year of all five of the major banks and although the scenario is not pretty, it’s not a disaster either. The share prices of banks are all between 20% and 35% down on their coronavirus trading positions.

But there has been a price: provisions for bad debts have skyrocketed, and headline earnings per share declined by between 44% for Standard Bank and 82% for Absa, with Nedbank sitting in the middle with 69%.

This bad debt provision is especially worrying. Take FirstRand’s results, issued on Thursday 10 September. Total impairment charges – that is, all the loans that did go bad or look as though they might go bad – jumped from R10.5-billioin last year to R24.3-billion this year.

That is breathtaking, but compared with the total loan book, non-performing loans are not a huge proportion, now sitting at about 4.4% of the total. And overall, tier one capital – the cash banks need to keep on hand in case of emergencies – is now at 14.5%, about a percentage point down on last year. The other banks are more or less in line with these numbers, give or take.

Ironically, we have the 2009 financial crisis to thank for this superprovisioning, which has created a big shock absorber in requiring higher levels of tier one capital, and other accounting measures. The crisis also sparked a redefined accounting standard which categorises more conservatively what constitutes a non-performing loan.

Wayne McCurrie, a portfolio manager at FNB Wealth & Investments, says this is where to look for the silver lining to the dark cloud. The level of provisions is probably at the maximum now, so there is a good chance they won’t increase over the next few years. There might even be some drawback, and the result would be a really thumping earnings bump.

Banks are also trading at very low valuations, partly because of the doubt which has surrounded the sector during the coronavirus picture. But more recently, we have seen these valuations improve somewhat.

Banks have other winds blowing at their back now too, and one includes the really startlingly lower interest rates. McCurrie says lower interest rates are a short-term problem for banks because they earn less on their cash holdings. But over the longer term, lower interest rates mean cheaper loans, which means there is more money available to loan out. Because it is more affordable, more people tend to take out loans, because they have a greater ability to pay them back.

One interesting measure is WesBank, McCurrie points out. There were very few cars sold over the past six months, but WesBank’s profit is only down about 7%. What that demonstrates, he says, is the power of annuity income. Because bank loans stretch over long periods, they are often able to withstand short-term knocks, like the one we have just seen.

The overall positivity of the banks is demonstrated by their obvious desire to pay dividends. The only reason they are not is that they have to comply with the Reserve Bank’s stipulation that they have to conserve capital.

Yet, this positive view of banks is far from being unanimous. Paul Theron of Vestact says there is likely to be a change in narrative from these levels, since it’s hard to see a situation where there isn’t some bounce-back.

However, more broadly, banks will be battling a poor economy for years to come. “We like to imagine we will be okay because we have always snatched victory from the jaws of defeat.”

But it’s far from clear where in fact the change in fortunes for SA’s economy will come from. “We don’t own bank stocks, even at these levels.”

Neelash Hansjee, Portfolio Manager at Old Mutual Equities at Old Mutual Investment Group, agrees with the general proposition that bank results are not as bad as it might seem.

“The whole system reacted proactively,” he said. Interest rates came down fast, and the Reserve Bank created liquidity when necessary. The response was in marked contrast to the 2009 crisis, and the result is that banks’ capital structures have held up.

But the overall economic context is still a worry. Although interest rates have come down it’s worth noting that banks earn less in a lower interest rate environment, somewhat reducing the effect of being able to loan more.

Banks will still need to demonstrate they are in fact able to leverage the lower interest rates, he says. BM/DM