Cyclists pass through an interchange in view of the Bank of England (BOE), left, and the Royal Exchange in the City of London, U.K., on Monday, July 20, 2020. Photographer: Jason Alden/Bloomberg

Cyclists pass through an interchange in view of the Bank of England (BOE), left, and the Royal Exchange in the City of London, U.K., on Monday, July 20, 2020. Photographer: Jason Alden/Bloomberg By contrast, most of Europe is set to benefit from the European Central Bank’s purchases and may offer the best shelter for investors worried about a potential surge in bond yields.

The debt deluge comes after a flurry of interest-rate cuts and expanded asset-purchase plans by central banks left investment playbooks in shreds. Of course, investors buy debt worth hundreds of billions of dollars every year. But in an era where some assume central banks’ support is all encompassing, the trillion-dollar gap between supply and policy-maker demand highlights just how important conventional investors still are for governments looking to fund record stimulus.

With a net surplus of $980 billion in expected issuance beyond central-bank purchases, here’s a look at the supply and demand dynamics in the world’s major markets in the second half of the year.

Treasury Tussle

The Treasuries market alone could see more than $1 trillion in net bond supply in the six months through Dec. 31, and strategists are predicting sales will comprise fewer bills and more longer-dated notes.

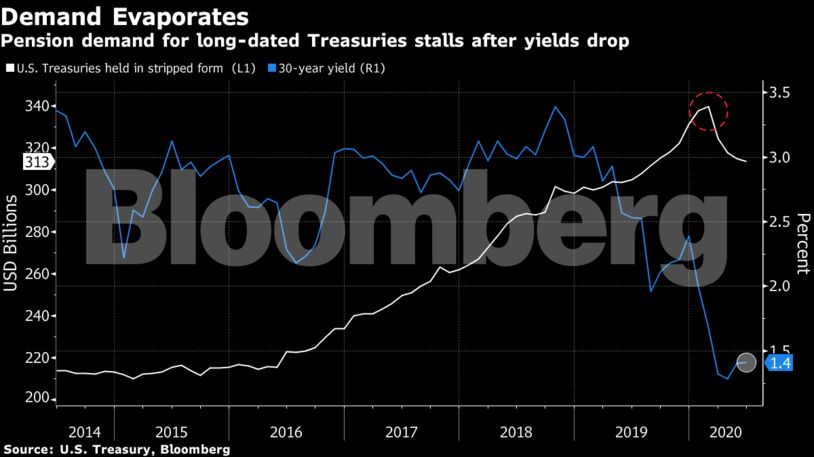

So far, domestic buyers have supported U.S. debt. But some of the market’s most loyal investors appear to be stepping away just when they’re needed most. Pension funds typically buy Treasuries to match their long-term liabilities, yet a proxy for their purchases of longer-maturity bonds -- holdings of so-called stripped Treasuries -- has fallen consistently since February.

With this in mind, positioning for a steeper yield curve -- when longer-maturity bond yields rise faster than their shorter-dated counterparts -- has become a popular trade.

Still, the latest 30-year bond auction was rock solid with a group of buyers that included foreign central banks bidding via the Federal Reserve Bank of New York taking 72%, a record.

Read More: American Investors Are Plugging the U.S.’s Record Budget Deficit

JPMorgan Chase & Co.’s Jay Barry projects a 35% increase in Treasuries supply over the second half, “along with a moderate demand gap,” and recommends investors consider steepener bets that benefit with the gap between yields on five- and 30-year bonds widen.

However, others on Wall Street warn that the curve is more likely to flatten, with longer-dated bond yields falling, given that the Federal Reserve could increase the pace of its Treasury purchases as early as this month, or even extend the duration of its purchases.

“The Fed’s main commitment is, was and will always be to the Treasury market,” said Mark Spindel, chief investment officer at Potomac River Capital. “The long end of the Treasury market has looked attractive and should remain so for a while.”

Buoyant Europe

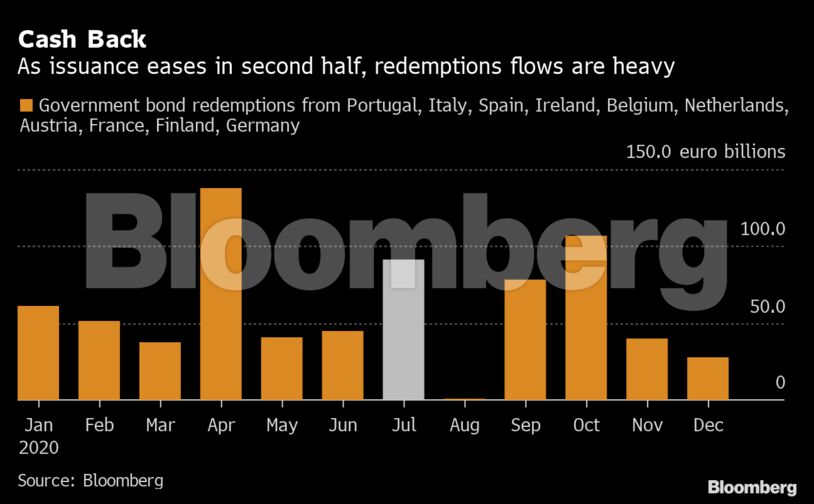

It’s a different story in Europe. Government bond sales in the euro area look set to fall short of the European Central Bank’s purchase plans and investor redemptions by 222 billion euros ($251 billion) from June 30 through year-end, according to Bank of America strategist Erjon Satko.

That’s a positive backdrop for European bond markets and should allow for some outperformance versus peers, he wrote in a recent note.

But Germany is bucking the positive trend, with 150 billion euros of supply due in the second half, more than any of its regional peers, according to Jorge Garayo, a rates strategist at Societe Generale SA. The bulk of sales is expected in maturities beyond seven years, which could push up yields on longer-maturity debt, he said.

“Germany is probably the country that is furthest behind in its issuance need for the year,” wrote NatWest Markets strategist Giles Gale in a note to clients. He sees 10-year bund yields climbing into positive territory in the second half, up from current levels of around minus 0.45%.

Japan Steepening Storm

Meanwhile, Japan has seen an almost perfect backdrop for curve steepening. Buoyant risk assets, low currency-hedging costs that are driving money overseas, record sized 10- and 30-year bond auctions, and the central bank buying increased amounts of shorter-dated bonds have all combined to widen the yield gap between short- and longer-maturity bonds.

The spread between five- and 30-year bond yields hit the highest in almost a year on July 2, just before the 30-year sale. Despite concerns, the auction was very well received and kicked Japan’s notoriously yield-hungry insurance companies and pension funds back into action.

“Life insurers may continue to buy super-long bonds regularly, but there are few reasons for them to front-load purchases or quicken the pace of buying,” said Eiichiro Miura, general manager of the fixed-income department at Nissay Asset Management.

Bank of Japan Governor Haruhiko Kuroda’s latest comments would support that. At last week’s policy meeting, he reiterated a need to keep the yield curve stable and said excessively low yields on the super-long bonds would cause problems.

Canada Supply Pop

Canada’s long-dated bonds have swung in recent weeks as the government announced a flood of new issuance. The nation is lining up as much as C$106 billion ($78 billion) of 10- and 30-year bond sales in the fiscal year to March, according to budget documents. In total, it expects gross bond issuance of C$409 billion.

With less than C$100 billion in redemptions due over the same period and the central bank on track for C$120 billion in purchases through December -- assuming it continues at the current C$5 billion a week rate -- that’s a lot of excess supply that could pressure bond yields higher.

“Higher duration supply and a well-anchored front-end argues for continued CAD curve steepening, absent an offsetting increase in Bank of Canada purchases at the long end,” wrote Goldman Sachs Group Inc. strategist William Marshall, in a note to clients.

U.K. Supply Pressure

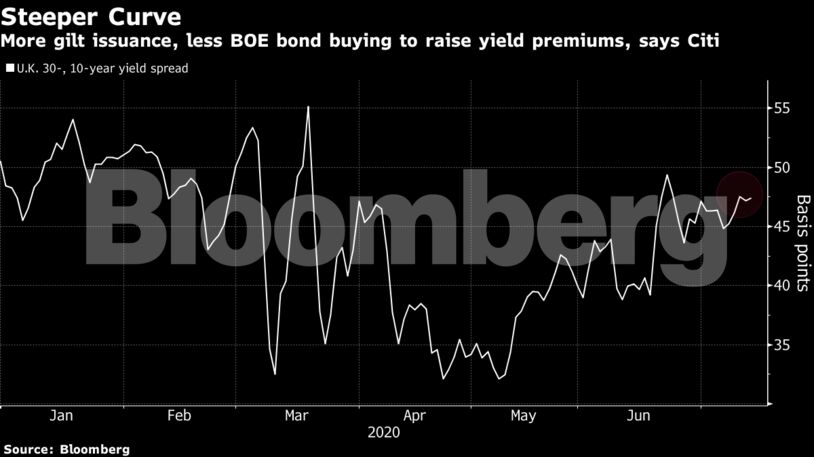

The weight of record gilt sales is expected to push the yield premium on the U.K.’s 30-year bond over its 10-year equivalent to a four-month high of 55 basis points, according to Citigroup Inc. It was as low as 32 basis points in May. The Debt Management Office announced 110 billion pounds ($138 billion) of bond sales between September and November on Thursday. That would significantly outweigh Bank of England purchases for the rest of the fiscal year, according to rates strategist Jamie Searle.

New Zealand Story

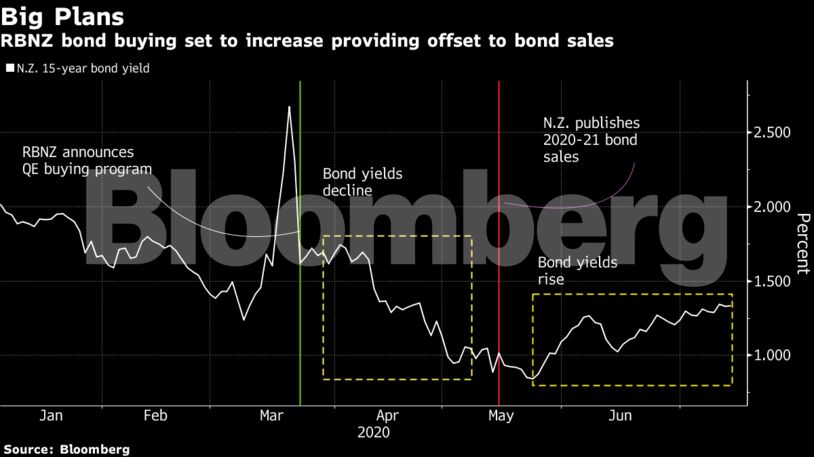

The next fiscal year has just begun in New Zealand and the Debt Management Office forecasts NZ$49 billion ($32 billion) of net issuance over the period. And there’s around NZ$40 billion of central-bank asset purchases to go before policy makers hit their cap. At the current pace, that will take until May, but the central bank is expected to expand asset purchases in August.

So far, the announcement of big government spending plans has sent bond yields edging higher.

“We continue to expect a further top-up in the RBNZ’s large scale asset purchase program at its August meeting,” Morgan Stanley’s Andrew Watrous wrote in a note, continuing to recommend curve flatteners, which benefit when short- and long-term yields converge.

Australian Autopilot

There’s less uncertainty in Australia where the pace of issuance is running at around A$4-5 billion ($2.8-3.5 billion) per week, and the central bank’s yield-targeting program is on autopilot with no purchases since May 6. Reserve Bank of Australia Governor Philip Lowe signaled on Tuesday there is little chance of any imminent bond buying, saying yields need to be sustainably higher.

That suggests about A$100 billion in gross bond sales remaining in 2020, up against almost A$22 billion in redemptions.