A good option for retirees who have been affected by the downturn is to secure a portion of their income needs using a guaranteed annuity, particularly one linked to inflation. (Photos: Rawpixel / Adobestock)

A good option for retirees who have been affected by the downturn is to secure a portion of their income needs using a guaranteed annuity, particularly one linked to inflation. (Photos: Rawpixel / Adobestock) The big difference between the two generic types of pensions (annuities) is: with a guaranteed pension, you take no risk, but with an investment-linked living annuity (living annuity) you take all the risk.

There are advantages and disadvantages to both.

The big question remains: why do 90% of pensioners use living annuities in preference to guaranteed annuities when research undertaken by Sanlam and Just SA finds that between 81% and 87% of retirees want a secure income?

Actuary David Gluckman, chairman of the Sanlam Umbrella Fund and head of Sanlam Special Projects, says at the point of retirement the vast majority of members are not yet ready to make a binding commitment for the rest of their (and their spouse’s) life on their pension.

“There is a genuine need for optionality, and particularly because the vast majority have simply not accumulated sufficiently. Financial advisers might well consciously or unconsciously play on this need in promoting living annuities, but nonetheless it remains a genuine need.

“Until this is solved, I suspect it will be difficult to massively increase the take-up of guaranteed annuities (unless there is massive regulatory intervention). I also think the need for a living annuity diminishes a few years after retirement once pensioners are more in tune with the realities of retirement.

“If somehow in product design we can build in some flexibility in the first few years after retirement, I suspect the take-up of guaranteed annuities around the age of the early 70s could substantially increase. So, there is a human behaviour element to this puzzle. Theory and practice are somehow at odds.”

Deane Moore, chief executive of Just SA, a life assurance company that blends living and guaranteed annuities, says this question is often asked the wrong way as: “How soon will I die?” rather than as: “How long will I live?”

If you are well off, have a low drawdown rate and lower-risk investments, then you may only need a living annuity.

The mixed annuity products are called “hybrid” or “flexible” or “blended” pensions, allowing a more versatile and lower-risk approach to providing an income.

Moore sums it as the pensioner thinking of her retirement money being in two pots.

- Pot 1: Using a guaranteed annuity to sustain them financially for life, no matter how long they live. This is a “no regrets” decision in that it deals with the question of, “What happens if I live past tomorrow?”

- Pot 2: Using a living annuity for flexible spending; or to leave the residue capital for beneficiaries. In other words, it answers the questions of, “What happens if I die tomorrow?”

Some other differences you need to keep in mind in structuring your pension:

- You can always transfer out of a living annuity, either to another product provider, or to a guaranteed annuity.

- Once you have a guaranteed annuity you cannot transfer out of it either to another provider to switch back to a living annuity.

- Another major advantage of using a hybrid annuity is that as you get older you could start suffering from dementia. By that stage, if you are fully invested in a guaranteed annuity, you will have far less chance of being ripped off.

- You can use a hybrid annuity from the start of your pensionable years, or later on when the guarantee annuity rates are much higher.

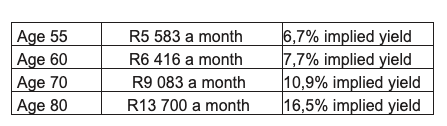

- The returns for a guaranteed annuity get better the older you are. Moore gives the example of a male pensioner who buys a profit annuity with R1-million, in a balanced portfolio that would increase at a rate equal to inflation at CPI+4% over the lifetime of the pensioner, with no guarantees or provisions for a spouse.

The implied yields (the pension divided by the capital expressed as a percentage) are as follows at the start of the guaranteed pension:

Actuary John Anderson, head of research at Alexander Forbes, says this table, indicating guaranteed annuity rates, shows that it is still possible for a large portion of pensioners to still achieve a sustainable income into the future by making use of guaranteed annuities.

With the big changes in investment markets following Covid-19 there has been a downturn in SA equity markets, but a significant improvement in bond markets. It has become one of the top-tipped investments.

The important thing about bond markets is the money that is lent to the government, its utilities and corporates makes up a major portion of guaranteed annuities.

So, a good option for retirees who have been affected by the downturn is to secure a portion of their income needs using a guaranteed annuity, particularly one linked to inflation.

It is also possible to receive some of the benefits of living annuities by using a guaranteed annuity depending on the underlying structure of the living annuity. The two main methods:

- You buy a guaranteed annuity. Guaranteed annuities come in different forms. They include a level annuity, which pays you the same amount for life but takes no account of inflation, or one linked to inflation, such as one that increases every year at 5% or is directly linked to inflation.

- A with-profit annuity gives you a more aggressive stance in investments markets, although you do not select the underlying investments. The big advantage is that with these annuities your returns are smoothed out. In other words, in good years some of the excess profits are held back and paid out in bad years. Here you share the risk with the life assurance company that the returns made will give you a pension increase at least equal to inflation.

With all annuities, including the with-profit, you get all the bells and whistles such as:

- A guarantee on payment for a certain number of years. If you die before the period is completed it will continue to be paid out to your beneficiaries.

- A pension for a spouse or partner.

The favoured annuity with the hybrid options is a with-profit annuity. There are a number of reasons for this and being exposed to equity markets is the main reason. With other annuities, you are mainly exposed to interest-earning investments like cash and bonds.

The problem with equities is they give the best returns over time, but they are the most volatile. The smoothing helps resolve the volatility.

When you purchase a with-profit guaranteed annuity you need to take account of the following:

- The Solvency Capital Reserves: This amount is set by the prudential regulator of insurance companies, namely the Reserve Bank, in terms of the new Twin Peaks control of financial institutions. The reserves to be held are meant to cover a one in 200 years disaster. All the pension companies in South Africa have reserves in excess of the required minimum. For example, the reserves of Just SA are 214%. Anderson says a very important part of any financial system is that the underlying insurance company must have sound risk management, which includes sound reserves. A lot of time is spent by Alexander Forbes in checking reserves. And the work is redone regularly.

- The initial pension rate: Anderson says life assurance companies are no longer getting away with quoting cheap initial annuity rates while taking very little risk for themselves. All life assurance companies now have to think a lot more carefully about their initial quote rates. A lot of this has been brought about by the requirements for default annuities where the government will not accept the total lack of disclosure.

- The initial discount rate or the post-retirement interest rate. You can in most cases select the initial discount rate. It works like this: if you have a high rate of, say, 6% on your first payment, your future increases will be discounted by 6%. So if the profit is 10% you will only receive a 4% increase. The lower the initial discount rate the better as you will be better able to handle inflation in the future. The best bet is an initial discount rate of between 3% and 4%. Moore says 3% is best as you also have to allow for costs. So if the portfolio achieves CPI plus 4% less the initial discount rate of 3% and the charges of 1% you will have an increase equal to inflation.

Moore says this is “a nice clear transparent benchmark”. He says there are different ways of calculating your returns. An example using an investment return is 10% and inflation 5%:

- Investment participation rate (IPR) 75% and post-retirement interest rate (PRI) 2%: increase would be 75% (10%) - 2% - 1% charges = 4.5% (slightly below inflation).

- IPR 100%, PRI 3%: increase would be 10% - 3% - 1% = 6% (above inflation).

- In lower return environments, the two formulae give similar increases. If you put in a return of 6%, the two increases are 1.5% and 2% respectively. It also means that initial discount interest rates are not directly comparable, because it depends on the investment participation rate as well.

- The bonus declaration. Traditionally, once a year the life company will declare a bonus rate from what is called in bonus reserves. If the reserves are nil or lower you may not get any increase that year. However, even if the reserves are negative you will not receive less than you are already receiving. What then happens is that future increases will be less than market returns while the bonus reserves build up. In the past, a view was taken by the chief actuary of a company about what the increase should be.

Next week: The structures of hybrid annuities. DM/BM

A series of reports written by Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, that cover the effects of Covid-19 on pensioners including research undertaken by Alexander Forbes on retirement income in South Africa. Bruce Cameron is co-author of the best-selling book, The Ultimate Guide to Retirement in South Africa.