Business Maverick has asked the Eskom Pension and Provident Fund where higher-than-average costs to pensioners are going. (Photo: Daily Maverick)

Business Maverick has asked the Eskom Pension and Provident Fund where higher-than-average costs to pensioners are going. (Photo: Daily Maverick) The Eskom Pension and Provident Fund (EPPF or the Fund) notes the Business Maverick article “A very revealing analysis of Eskom Pension Fund’s investment and administration costs” dated 16 April 2020.

We would like to draw readers’ attention to a few aspects of how the EPPF views the concept of administration costs per member, in response to the flawed cost comparison in your article. Your rebuttal claims that:

- The investment fees of the EPPF are not competitive;

- The Pension Fund SA (Pen SA) comparison set comprises small funds that enjoy no economies of scale when negotiating asset management fees; and

- The costs of the Fund’s services per member are high relative to other pension funds.

We believe that these accusations follow analysis that lacks vital context and present incomplete arguments. Your article begs a number of questions. The EPPF could have offered clarity if it had been granted the opportunity to do so before the publication of the article.

The EPPF follows a sound long-term investment strategy, which is implemented at very competitive management fees, in order to retain its ability to honour the financial promises made to our members.

The insinuation that the Fund is more expensive than the industry average in terms of pension administration and investment costs is unfounded and baseless. We have provided the evidence to support these claims in detail below:

Cost per member

Your article draws a flawed comparison between the EPPF’s cost per member to that of other pension funds and fails to take into account some basic principles about the pension fund industry in South Africa. A meaningful comparison requires us to first consider the following:

- Whether the EPPF’s retirement benefit administration costs are being compared with defined benefit funds (DB) or defined contribution (DC) funds. The administration of DB funds is very complex compared to that of DC funds, and this ultimately has a bearing on costs;

- If one compares the EPPF’s retirement benefit administration costs to similar DB funds, then the proportion of active members to pensioners in those funds is relevant. This is because pensioner administration activities in a DB fund are significantly more than those of active members;

- Whether the funds being compared are self-administered, like the EPPF, or if they outsource any of the functions performed by the EPPF, including the investment, administration, payment and/or underwriting activities to third parties or insurers. If so, is the total cost of the value chain included in your cost per member comparative; and

- Do these comparative funds, like the EPPF, perform ancillary services such as medical aid and insurance administration, trust administration, ill-health retirement administration, and benefit investigation services? If so, are these costs included in the cost per member referred to? If not, then how much do the comparative funds charge for each of the ancillary services listed?

In short, are we comparing like with like?

Unfortunately, these omissions in your article mean that accurate comparisons regarding cost per member cannot be made.

Investment management

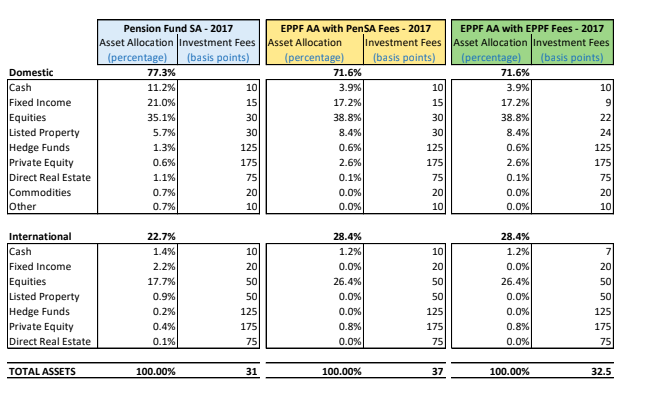

Comparison of the EPPF Investment Management Fees versus Pension Fund SA. When reviewing the investment management fees of a pension fund, there are five factors that must be considered before drawing any conclusions about their relative competitiveness:

- Split of assets between domestic and international mandates;

- Allocation of traditional assets between growth assets (equities and listed property) versus fixed income securities (bonds and cash);

- Split of assets between traditional and alternative asset classes;

- Exposure to sub-classes of alternative assets such as hedge funds, private equity, and direct real estate; and

- An independent and publicly available survey of asset management fees on a mandate-by-mandate basis.

This is simply because fees on international mandates are higher than those of locally managed assets, and fees on unlisted investments are greater than those of traditional asset classes. Typically, the more conservative the mandate the lower the fees, but also the lower the expected return.

The EPPF’s asset allocation is determined through a rigorous Asset-Liability Model (ALM) which is performed annually by actuaries and investment professionals. The EPPF therefore holds an asset allocation that optimises its assets relative to its liabilities, within the prescripts of Regulation 28.

Your article uses data from the Registrar of Pension Funds Annual Report to benchmark the investment management fees paid by the EPPF against other pension funds. Because a fund’s asset allocation influences the fees, we have analysed the asset allocation of the Pension Fund SA set, as reported in the Registrar of Pension Fund's annual report of 2017, which you refer to.

Our first observation is that the Pension Fund SA set has an 11.2% allocation to cash, compared to the EPPF’s nearly 4%. Cash is typically a low-risk and low-return asset class, and the fees charged on cash management are low. We also note that the EPPF has a higher allocation to private equity (2.6% vs. 0.6%), and a significantly higher allocation to international equity (26.4% vs 17.7%).

This implies that the EPPF has a higher allocation (driven by its well-considered ALM) to asset classes that attract higher fees. One should therefore not be surprised if the EPPF’s investment management fees, at 33 basis points (0.33%) are higher than those of Pension Fund SA at 31 basis points (0.31%), as quoted in your article. In this instance, the difference in total investment management fees is 2 basis points (i.e. 0.02%).

The fees paid by EPPF would be much higher if the Fund did not negotiate competitive fees with its asset managers.

A widely used and publicised reference point for fees charged by the investment industry to institutional pension fund mandates is the Alexander Forbes Fee Survey. We considered the December 2019 survey, which utilised data from 2015 to 2019.

We applied the lowest fee scale from the survey to each of the asset classes in which the EPPF invests, as well as a notional portfolio for the Pension Fund SA set.

Our analysis shows that if the asset allocations of the EPPF and Pension Fund SA were the same, Pension Fund SA would have paid 37 basis points in investment fees. The EPPF paid 32.5 basis points for that actual allocation. On a like-for-like basis, the EPPF’s fees were 4.5 basis points lower than those of Pension Fund SA.

This shows that the EPPF does negotiate lower fees with its external asset managers, and that the in-house investment management function helps the Fund to maintain lower than average industry fees.

Cynics will no doubt say that as a large investor, the EPPF should be paying even lower fees than 33 bps (0.33%) of assets under management. They may argue that the Pension Fund SA sample is a list of small and disparate pension funds that enjoy no economies of scale. This reasoning is misleading, because it does not account for the role that is played by the dominant asset consultants and the benefit administrators in driving the costs down for the largest pension funds.

Cynics will no doubt say that as a large investor, the EPPF should be paying even lower fees than 33 bps (0.33%) of assets under management. They may argue that the Pension Fund SA sample is a list of small and disparate pension funds that enjoy no economies of scale. This reasoning is misleading, because it does not account for the role that is played by the dominant asset consultants and the benefit administrators in driving the costs down for the largest pension funds.

The South African industry had 3,962 pension funds with approximately R2.42-trillion assets as at the end of December 2017. The largest 100 pension funds represent 2.5% of the number of funds, but account for two-thirds of the total assets (with an average size of R1.63-trillion). The fee scale of 31 basis points in 2017 is weighted in favour of these larger funds (average size R16.3-billion) who are able to negotiate more favourable investment management fees – directly or through their asset consultants and benefits administrators.

The financial health of the EPPF

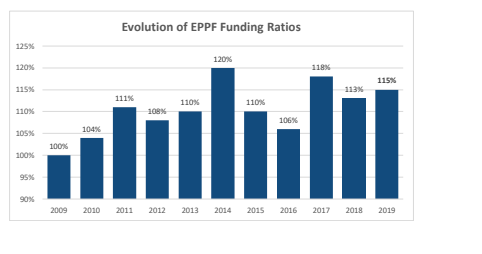

The EPPF remains one of the most well-funded pension funds in South Africa and internationally, standing head-and-shoulders above the US, UK, and some European (OECD) pension funds.

Business Maverick response to the EPPF’s right of reply

By Ruan Jooste

The Eskom Pension and Provident Fund (EPPF) wants the public and its members to believe the fund’s excessive operational cost structure and higher-than-average asset management fees are justified due to its complicated operational structure and convoluted investment portfolio. It also has to fund its in-house administration and money management capabilities, it says.

However, the fund’s response misses the main focus of the comparative analysis provided in Business Maverick’s previous article. To briefly recap, traditionally, investment fund costs are measured as a proportion of the value of the overall fund. This is the most logical and obvious measure, although what is included in overall costs and how those costs are calculated are matters of intense debate.

Broadly speaking, the overall costs of investing in investment funds of different types range from about 0.5% and 2.5% of funds under management, or between 50 to 250 basis points. Some funds, like tracker funds, cost less, and others like hedge funds cost more, but generally, that is the range.

A portion of those costs are administration costs, and these are the issue here mainly because they are costs in the direct control of the administrator, or at least the costs the administrator is able to negotiate with fund managers.

In the EPPF case, investment management fees, at 33 basis points (0.33%) are higher than those of the average South Africa pension fund, which we call Pension Fund SA, at 31 basis points (0.31%) and the EPPF has presented above its reasons why this is the case.

But what it has not addressed is, firstly, the absolute cost per member, and secondly, the trajectory of costs. The absolute costs per member are crucial here because as our analysis shows the EPPF is, by comparison, an extremely rich fund and its average member contribution is very high. It also has been rising fast, suggesting Eskom employees salaries have been rising fast too.

Since EPPF members are contributing on average just under R90,000 a year compared to the R10,000 of contributors to Pension Fund SA, even though as a proportion of investments, they are about the same, it still means in absolute terms, EPPF members are paying on average of R690 a year, while Pension Fund SA members are paying R333.

And crucially, these numbers are rising, whatever measure you use.

The second criticism of EPPF administration, which the organisation addresses at length, concerns the issue of whether as a huge fund, it ought to be negotiating a better deal with fund managers.

It is our criticism that members are funding inefficient operations and are not extracting any value from economies of scale pertaining to the large pool of assets under management.

Why should an EPPF member pay a vastly different amount for the same service offered by other administrators and asset managers in the local pension fund industry, especially when they are contributing to one of the largest and most influential funds in the country?

The EPPF manages the biggest pool of private funds in South Africa and, as such, must be achieving significant economies of scale, a well-known economic theory and exactly what other large section 13B (of the Pension Funds Act), administrators are achieving in a much more complex multiple-fund environment.

There is no evidence of such achievement in the information provided by the EPPF in administering a single legal entity fund with about 84,000 members.

The cost to the member is actually pretty simple.

Whether the fund is a defined benefit (DB) or a defined contribution (DC) fund, it will make very little difference to the administration costs of that fund and may only have a small impact on operational cost, and thus does not explain the significant difference in expense when comparing the EPPF with the rest of South Africa’s private retirement fraternity.

Receipt of and investment of contributions is required for both DB and DC funds, despite parts of the structure of DB funds being more complicated, and arguably a DC fund is more complex where there are more choices offered to members and investment records must be maintained at a member level – there is no significant difference where automated administration systems are concerned. They all manage the functions of the receipt of member data, validation, reconciliation and the investment of contributions the same way. The fund has, after all, claimed on many occasions that their systems are of a high standard and fully operational.

Furthermore, the administration of the high proportion of active members at the EPPF will only require a little additional work and on an ongoing basis, this is negligible as it only occurs when a new pensioner is set up on the administration system.

Once again, the fact that EPPF is a DB fund and has thousands of active members and pensioners cannot explain the substantial differential in administration costs to Pension Fund SA. It could be that they still run all their unclaimed benefits functions on physical spreadsheets, which does not form part of their automated process, but that is a story for another day.

In the experience of experts that Business Maverick has consulted, third-party administrators usually charge less for pensioner record-keeping and in some rare cases, the same that they would charge for that of an active member record.

“If there was a marked cost differential, the market would have jumped on this to explain why pensioner administration is more expensive than that of active membership and charged accordingly, yet that is not the case,” they say.

The Pension Funds Act specifically states that all the funds’ costs must be disclosed in the annual financial statements whether it’s self-administered, part of salaries or any other payments made to a third-party administrator.

It is for this very reason the Business Maverick analysis splits the total administration expense between fund costs for being a legal entity that simply exists with prescribed fixed costs like audit fees and the cost to administer it. A third-party provider system will encompass an administration fee, which a self-administered fund would not have, so the comparison is more than feasible.

The comparison in this regard was done on a line for line and constant basis, and therefore is highly comparable especially as the statutory format of annual financial statements are prescribed by the Financial Services Conduct Authority (FSCA), which the Business Maverick has a template of, and in which it populated the above-stipulated costs of all private pension funds in the exact same manner.

The EPPF further asks if the comparative funds, like the EPPF, perform ancillary services such as medical aid and insurance, administration and ill-health retirement administration, as well as benefit investigation services? Other funds perform the exact same function as the EPPF as their costs pertaining to that are reflected in their financial figures, just like that of the EPPF.

So, whether the fund is self-administered or outsources services, it still needs to operate, and the cost of these operations will be reflected in the annual financial statements either as an administration fee and/or a direct line cost, so once again it remains extremely comparable.

If the EPPF is implying they offer a better service than other funds in the industry, which justifies their higher operational expenses, the over 500 members the Business Maverick has had contact with, would disagree, especially because they are paying up to three times more for the exact same administration function that is provided by other retirement funds.

In addition, the EPPF cannot link the cost of administration to the range of benefits it offers its members, as that is specific to an individual fund in terms of its own rules, which differs across the spectrum of funds that operate in the country.

The point is that the EPPF’s expenses are excessive, which takes a significant amount of money away from being invested and contributes to better pension increases every year, which in the case of the EPPF has halved from 4% to 2% between 2019 and 2020.

As a matter of fact, the annual pension increases over the last few years don’t even match the net investment returns earned by the EPPF each year, which should be a grave concern for the board of trustees.

When it comes to the investment costs, the EPPF states that it’s based on the type of asset class and where it is located. While this might be a consideration, the mere size of the investment portfolio of R140-billion or so is a matter that cannot be ignored.

Business Maverick did not delve into the actual types of asset classes and whether it was based inland or offshore, but made a direct comparison between the total investment fees of local pension funds, which all invest in different asset classes and across borders, to that of the EPPF.

And of course, other funds are smaller and will be less diversified given the risk and cost involved for their tinier asset pools, and are more expensive to manage, yet the investment cost of the EPPF as a total remains in excess of every other privately managed pension fund in the country.

There are other aspects of the EPPF’s response we would dispute, including the proportion of cash that the average pension fund holds and the similar holding of the EPPF, and we will do so in future.

The crucial question is where are these higher-than-average costs to pensioners going? Business Maverick will answer this question in subsequent articles. DM/BM