Sisa Ngebulana, will require a lot of energy in the next five weeks for crucial talks with shareholders, lenders and corporate fixers over a rescue plan for his debt-laden real estate company Rebosis Property Fund. (Photo: Gallo Images/Russell Roberts/Financial Mail/Getty Images)

Sisa Ngebulana, will require a lot of energy in the next five weeks for crucial talks with shareholders, lenders and corporate fixers over a rescue plan for his debt-laden real estate company Rebosis Property Fund. (Photo: Gallo Images/Russell Roberts/Financial Mail/Getty Images) Sisa Ngebulana, the businessman who founded one of three available black-owned and managed real estate companies on the JSE, has overhauled his eating habits by embracing a liquid diet.

The diet, which Ngebulana started on 27 January, usually involves a berry smoothie for breakfast, vegetable soup for lunch and a vegetable smoothie (with ginger and kale being the main ingredient) for supper – with the meals being washed down with a cup of hot water throughout the day. The liquid diet is not part of his 2020 New Year’s resolution but his general goal to detox, feel feather-light and replenish his energy to function optimally.

The start of the diet is well-timed because Ngebulana will require a lot of energy in the next five weeks as he will be in crucial talks with shareholders, lenders and corporate fixers to win them over to a plan to rescue his debt-laden real estate company Rebosis Property Fund.

“The next few weeks will be intense. I am confident we will get out of our problems. We are not giving up without a fight,” Ngebulana told Business Maverick.

In a few years, Ngebulana has turned Rebosis from being a company with only seven properties worth R3.3-billion when it listed on the JSE in May 2011 to one that is one of the bourse’s most consistent dividend payers, with more than 40 properties valued at R16.3-billion today.

Its portfolio of properties includes well-known shopping centres, including Baywest Mall in Port Elizabeth, Forest Hill in Centurion, and Hemingways Mall in the Eastern Cape and more than 30 office properties, most of which are let to government departments and agencies.

Underpinning the Rebosis rescue plan is its potential merger with Delta Property Fund, a JSE-listed real estate company co-founded by Sandile Nomvete that owns a portfolio of properties worth R11.3-billion, comprising 81 office properties tenanted by government departments.

If successful, the proposed merger could create an enlarged black-owned and managed entity with property assets that are worth more than R25-billion at a time when racial transformation in the sector remains woeful.

Ngebulana believes the enlarged entity would be able to ride out SA’s stalling economy and the resultant lack of demand for property space by tenants because institutional investors prefer investing in real estate companies with scale and liquidity to their shares, making it easier to raise capital to fund growth initiatives.

But some shareholders are vexed by the proposed merger, saying Rebosis and Delta are better off as standalone and competing companies, intensifying possibilities that that merger talks might collapse again – they were once aborted in 2014. In fact, about 80% of Rebosis’ ordinary shareholders voted against implementing the company’s remuneration policy on Monday 3 February – unprecedented for the real estate sector – a sign that shareholders are losing patience with the company’s lofty promise of a turnaround and recovery.

Asked what will become of Rebosis, which needs fresh capital to pay down its debt of R10.1-billion as of August 2019, which is more than 60% of the value of its properties (R16.3-billion), if the merger is not successful, Ngebulana said:

“We have been approached by a lot of private equity players, which would mean that if concluded, they would buy out Rebosis and will delist it from the JSE. The Rebosis board will consider the offers. But before doing this, we would first do a capital raise to fix the balance sheet.”

Since the proposed merger was announced in August 2019, Rebosis and Delta haven’t released terms of the merger including the valuation of the deal and how it will be structured. Because merger talks “have carried on for too long”, Rebosis and Delta have set a deadline of the first week of March for lenders and shareholders to complete their due diligence processes into both companies.

Cap in hand to shareholders

Rebosis plans to launch a capital raise among its shareholders of an undisclosed amount to reduce its uncomfortable debt load – something that shareholders are considering in their due diligence process. Delta will also approach its shareholders for fresh capital.

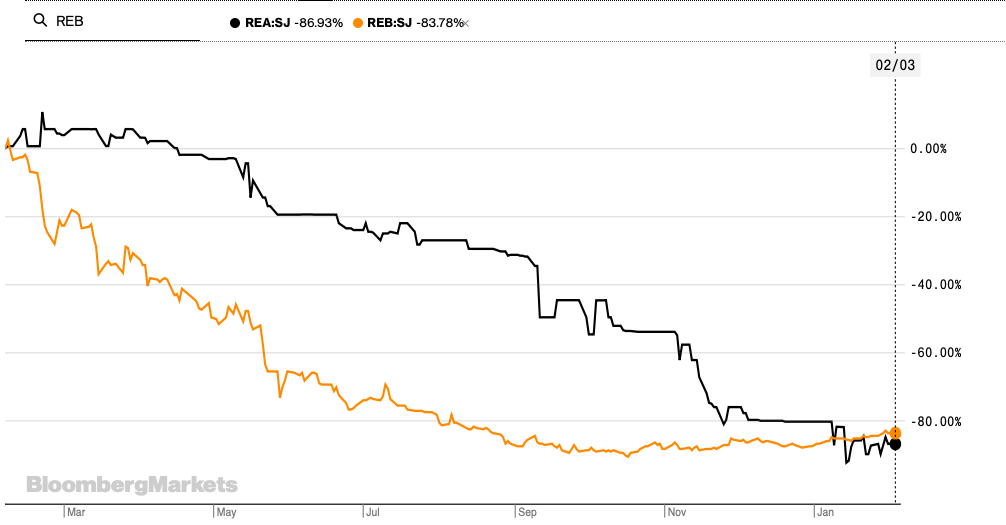

Whatever amount Rebosis is targeting through the capital raise, it might be higher than the market capitalisation of its A and B shares, which have a combined value of R460-million. Rebosis has an A and B share structure – shares that have each fallen by more than 80% over the past 12 months, wiping off a combined R2.6-billion in their market capitalisations.

The share structure is designed to cater to shareholders with different risk appetites, as shareholders owning A-shares have the first claim to outstanding dividends if Rebosis collapses and are guaranteed a capped 5% growth in dividend payments. Shareholders owning the B-shares are the last in line for dividends and there is no cap to the percentage growth in their dividends.

The share structure is designed to cater to shareholders with different risk appetites, as shareholders owning A-shares have the first claim to outstanding dividends if Rebosis collapses and are guaranteed a capped 5% growth in dividend payments. Shareholders owning the B-shares are the last in line for dividends and there is no cap to the percentage growth in their dividends.

Start of debt problems

But its debt problems have meant that Rebosis has suspended dividend payments to shareholders to preserve company funds. The source of Rebosis’ debt problems have been largely created by its ill-fated acquisition spree in the UK, when it paid R1.26-billion in 2015 for a stake in UK shopping centre owner New Frontier Properties (NFP) using cash and debt.

A year later, UK citizens voted in a referendum to leave the EU – a nearly four-year-long process called Brexit that resulted in a 30% write-down in the value of NFP’s properties in 2018. Real estate buyers and sellers held back because of the uncertainty caused by Brexit, affecting property valuations in the UK. Rebosis had to write down the entire value of its NFP investment – an investment that made up almost 40% of group earnings – by taking a R2.6-billion impairment. This left debt in its balance sheet associated with the investment. Rebosis cut its losses with NFP last year, selling its entire 49.35% stake in the company to Orion Hotels & Resorts, among others, for R700.

Underscoring its debt burden is a loan-to-value (LTV) ratio, a key metric used in the real estate sector to measure a company’s debt against the value of its assets. Rebosis’ LTV ratio sits at 64.5%, which is the highest in the real estate sector. Shareholders prefer a company to have a ratio of less than 40% because beyond this threshold, a company faces the risk of missing debt payments if lenders were to immediately call loan repayments.

Ngebulana wants the LTV ratio to drop to below 40% through the capital raise and possibly more asset sales. He was forced to sell one of Rebosis’ first shopping mall developments in 2019, the Mdantsane City Shopping Centre in East London, to Vukile Property Fund for R521-million, proceeds that were used to reduce the company’s debt.

Although he says Rebosis has so far received “in-principle support” for the capital raise from major shareholders, there are suggestions in the market that the proposed merger is a ruse to bail out troubled Rebosis. For one, Delta’s debt profile (LTV ratio of 44.3%) isn’t as extreme as Rebosis’ (64.5%).

Says Ian Anderson, the chief investment officer at Bridge Fund Managers, which has been party to some of the initial discussions around the proposed merger: “Those initial discussions and some of the higher-level proposals put forward to us did not convince us that a deal was in the best interests of Delta shareholders but that it could (and probably would) be beneficial for Rebosis shareholders.”

Redefine Properties, which was previously a shareholder in Delta until it sold its interest to a BEE consortium called Cornwall Crescent in June 2017 for R1.46-billion but still carries a loan risk that facilitated the sale, said it did not support the merger and would advise shareholders to vote against it.

Ngebulana has hit back at Redefine: “They [Redefine] are not a shareholder to Delta. It is interesting how they have announced their views when they are not even a shareholder.”

Anderson also questioned whether the capital raise would succeed, “given the quantum of new capital needed to restore the balance sheets of both companies in a single raise as well as the role Nedbank was prepared to play in helping the transaction succeed”.

Nedbank has a loan exposure to Rebosis (debt exposure to the company and its subsidiaries worth R8.6-billion) and Delta (more than R3-billion).

Market watchers have said Nedbank might support the capital raise by converting a portion of its loans in both companies for equity. Ngebulana said Nedbank is “supportive” of the proposed merger as it “sees the synergies and benefits of the merger and they think it is the right thing to do”. BM