South Africa

Today’s loan shark feeding frenzy, tomorrow’s revolution

In Grahamstown, there’s a woman who only gets R120 from her monthly social grant of R1,200, because the rest is 'eaten up' by loan sharks. In a country where close on half of all credit-active people are impaired, the rampant growth in unsecured lending and illegal lenders is creating a real context for insurrection. By MANDY DE WAAL.

Hlomela Dlamini* has been working for the Makana Municipality in Grahamstown for some 15 years. He gets paid about R4,800** gross a month, but only nets little more than half of that. Each month he has the usual government deductions and there’s money that must be paid to his trade union, SAMWU. He also has repayments taken off his salary for Old Mutual, Sanlam and three funeral policies. The deductions off his municipal package total R2,270.00**, which means that after 15 years of working for government, his net pay is R2,530.00**.

But some two-and-a-half thousand rand is not what Dlamini takes home and uses to live off. When the money goes into his bank account the Mashonisas take their cut, and that cut is the cruellest.

The word Mashonisa means “to sink”, because these unscrupulous lenders sink the people who borrow money from them so deeply in debt that for the most part, the borrowers never fully recover. In places like Grahamstown, people know that once the Mashonisas have access to your bank account, you belong to them. These lenders are unregistered and illegal and can charge 100 or 200% a month on a debt. It is estimated that there are about 30,000 illegal credit providers in the country.

This is how that Mashonisas work. If you take home some R2,500, like Dlamini, after all your salary deductions you’ll probably be able to get R1,500 in credit from the unregistered loan sharks.

You run out of money towards the end of the month and there’s an unforeseen emergency, so you take your payslip to these people who promise quick and easy cash loans. The Mashonisas make you sign papers granting them access to your bank account to subtract the principal amount you’re borrowing, plus the exorbitant interest.

You need R1,500, so you are given the money in cash, then and there, at the time of applying for the loan. At the end of the month your salary is deposited and the Mashonisas take their principal amount of R1,500 back plus interest of about R700, which means you’re only left with R230 in the bank, and you’ve got a whole new month to get through. So what happens is that you’re back knocking on the Mashonisa’s door again, looking for the next loan. And so the credit trap rolls on from month to month, because marginalised people mostly don’t have the wherewithal to get out of this cruel debt trap.

Ayanda Kota of the Unemployed People’s Movement, who helped Daily Maverick set up the interview with Dlamini and acted as a translator for the conversation, opened the municipal worker’s “pantry” after receiving his permission. Inside there was some rice, sugar, tea bags, salt, Rajah spice, Rama margarine, peanut butter, polony and a five-litre bottle of cool drink.

“I am not feeling well. I have so much pain. But I must make sure that my child is all right. The peanut butter, polony and juice – they are for my son. I want to make sure he is all right when he goes to school.”

Dlamini’s son recently started school and leaves the small home they share in the mornings to go and learn. The father and son live in a one-roomed shack with one bed, a small stove with two plates, an old sofa and a piece of rope on which clothes hang.

Kota told Daily Maverick that along with many others in Grahamstown, where unemployment is set at some 70%, this man’s spirit is broken. “People drown themselves in liquor. Or they just adapt and get used to suffering. There are those who live in poverty and just accept this as normal, and that’s dangerous. There’s something very wrong with that.”

As the founder of the Unemployed People’s Movement, Kota says Dlamini’s story is the everyman-and-woman’s story of marginalised living Grahamstown, a university town where poverty is rife. “Because unemployment is so high, people who do work must provide for the unemployed extended family. The National Credit Act says that furniture shops and lenders are not allowed to tantalise these people by sending cards advertising loans and letters. But they do this despite of the National Credit Act.”

Advertisements enticing people struggling to make ends meet to take out cash loans are commonplace. The promise of easy cash loans are found in the post, in an SMS on mobile phones, in local newspapers and street advertising. Loan offices are mushrooming in cities and towns across the country. And when people can’t get loans going through a legal route, they go to the Mashonisas.

“Unsecured lending is a major problem in this country,” Stephen Logan, a credit law expert and authority on the National Credit Act, told Daily Maverick. “There are people who can’t get credit at even the highest interest rates, and they go to the Mashonisas, who lend credit without being registered as credit providers.”

Kota said that unregistered loan sharks had wreaked havoc with people in his family and the wider Grahamstown community. An elder member of Kota’s family gets R1,200 a month as an old-age grant from the government. The man experienced a difficulty and went to a Mashonisa to borrow money.

“He borrowed the money from that Mashonisa, and they deduct the repayment and the interest straight back from his account. He now gets R750 and the Mashonisas, they take R450 for themselves each month,” Kota added. The man is trapped in a vicious debt cycle with the Mashonisas, so he borrows R750 each month, and the loan sharks take their interest of R450, and so it goes on because he hasn’t got the means to get out of their clutches.

“I know another person in Grahamstown who gets R1,200 a month but now only draws R120 from the bank. She has had to go back again and again to borrow more money, and now she is trapped in debt. She is trapped in poverty. There is nothing she can do.” The problem, Kota believes, is that people finance the basic cost of living, and then need to borrow more and more to survive.

This woman has borrowed to such a degree that now she doesn’t even get a survival amount and is dependent on others for her well-being. Over time her ongoing lending from these informal loan sharks has eroded her grant to literally nothing.

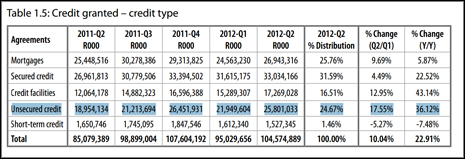

Figures issued by the National Credit Regulator (NCR) show that the financial health of consumers is deteriorating, while unsecured lending has grown significantly. Data released in September for the second quarter of 2012 showed that the value of new unsecured credit granted during the period increased by 17.55% when compared to the previous quarter. Looking at the year-on-year picture in the NCR’s data (see table below) the value of unsecured loans increased by 36.12%.

Credit granted by credit type (Source – NCR):

“The problem that we have is severe. Forty-seven per cent of all credit-active people are credit impaired, which means that nine million people are at least three months behind on their payments on one account, or worse. At the same time there’s this big growth in unsecured lending. The sustainability of the credit market is in question, because we are in a very low interest rate cycle, and as interest rates pick up, that level of indebtedness will become totally unsustainable,” says Logan.

Speaking to Business Day recently, the CEO of the National Credit Regulator, Nomsa Motshegare, said the rise of consumer debt, the increase in unsecured lending and the upsurge of what she called “unscrupulous lenders” could lead to civil unrest.

“Unsecured loans are not a bad product, but the rate at which it is being extended, especially in an environment where there are already high levels of consumer indebtedness, is of major concern to us,” Motshegare said. “The point is that totality of debt is increasing. While unsecured loans are only 9.1% of the total loans, people have cell phone accounts, they have to pay their municipal rates and taxes while coping with rising food and fuel prices,” she said.

Kota said that social unrest had been brewing for some time, and that the prevalence of protest and civil insurrection is increasing. “Unrest is building from the bottom up. People are losing confidence in the government, and everywhere you go, people talk about Nkandla.” Kota added that government excess and corruption fuelled anger amongst people who were struggling to make ends meet and losing their livelihood to loan sharks. “So many people are talking about the looting of governments. Revolution doesn’t have a blueprint. But you can see that it is building bottom-up.”

“There are so many instances where people aren’t getting paid because of garnishee orders. As prices increase people bear the brunt of this crisis. In the mines, on the shop floor and on the street you see working people prepared to go on unprotected strikes which shows there is major discontent in this country that’s coming from the bottom up,” he added.

Logan said that a stagnant economy meant salaried employees were seeing their spending power eroded. “With the rising cost of food, energy, and even the cost of water, people are struggling. Everything has become much more expensive over time, and it has become so expensive to live in South Africa that people are borrowing to finance their life or lifestyle,” Logan said.

“We have already seen social instability because of garnishee orders. This was part of the problem at Marikana, because the miners had these loans that they were paying back, and were left with so little to live on. This is a countrywide problem, and something we could see more of. The growing debt impairment will lead to more debt collection,” the credit expert said.

“South Africa’s population will be taking home less and less money, and this will lead to more civil unrest. There is a credit bubble that is coalescing and this is exactly what we don’t want to see happening. We don’t want to see greater and greater rates of impairment. We want to rather see it stabilising and reducing. The government and others are trying to fix this, but it is really very late in the day.”

As industry experts and media pundits pointed to the merging of a credit bubble, the Banking Association of South Africa (BASA) and the Ministry of Finance issued a statement at the beginning of November, in which both recognised SA was facing a problem.

“Representatives of major retail banks, the Banking Association of South Africa (BASA), the National Treasury, the South African Reserve Bank and the Financial Services Board have reached an agreement to improve responsible lending and prevent households from being caught in a debt spiral,” the statement, under the names of Pravin Gordhan and BASA CEO Sim Tshabalala, read. “The accord calls for several measures to be taken, including a review of loan affordability assessments, appropriate relief measures for distressed borrowers, reviewing the use of debit orders and limiting the use of garnishee orders.”

Logan told Daily Maverick that there were three key contributors to the “credit bubble”, namely reckless borrowing, reckless lending and the recessionary environment. A fourth contributor, he said, were the materialist values driving people to secure credit for cars, mobile phones and other items at very high interest rates.

“We need to get people to stop buying cars using unsecured personal loans. The banks are giving loans to people for cars, home improvements or home loans that are at 31% or 26% or 28% … This rate is ridiculous and totally unaffordable. The cost of the credit is mad,” Logan said, adding that people needed to look at the total cost of credit they were paying.

Logan said the high rate of credit impairment and unsecured loans was damaging for both the credit market and the consumers caught up in it. “It is very important that the credit system works well so that people can get access to credit, and get credit in a legal format where there are rights and obligations and protections. That people aren’t forced to go to Mashonisas which is undermining our society, and damaging people’s lives.”

“We have to ensure that credit providers implement the National Credit Act because we have one of the best acts in the world. The role of the regulator is really crucial in terms of trying to get this done, and it has been promising for a while now to do this.”

While the credit industry needs work, another problem is the financial literacy of consumers. Thandiwe Zulu, the provincial director Gauteng of the Black Sash, which helps counsel consumers with credit problems, said education was crucial to forging a sustainable solution to this country’s credit crisis. “There have been talks of credit amnesties, and this could remove the problem, but what needs to be tackled is the cause. The cause could be that people don’t know how to budget or manage their income, and then they succumb to debt and land in an even bigger problem. We need financial literacy and education that causes a change in people’s behaviour. We need to deal with the causes so that people manage their finances in an adequate way so that they don’t land in difficult situations that make survival impossible,” Zulu said.

But like most of this country’s problems, the challenge of the credit crisis is extremely complex. The high unemployment rate has created households where extended families are dependent on one or two people’s salaries; inflation and the high cost of living makes survival difficult; and those already caught in the debt trap seem to be falling through the floor.

Add the frustrations of incompetent local municipalities, and a national government that’s over-promising and under-delivering in spectacular fashion and you don’t need a political scientist to tell you South Africa’s become a pressure cooker on a very hot stove. And that all the loan sharks are doing is turning up the heat. DM

Read more:

- Rising risk of a credit bubble approaching bursting point in Business Day

- SA banks in pact on unsecured lending on BDLive

- Unsecured lending: Are we starting a bubble? on BDLive

- We’re drowning in debt… and sinking deeper on IOL

* Hlomela Dlamini is not this person’s real name. His name is known to Daily Maverick but has been changed to protect his privacy.

** The numbers given have been rounded up marginally so that this person cannot be traced or victimised by his employer.

Photo by Reuters.