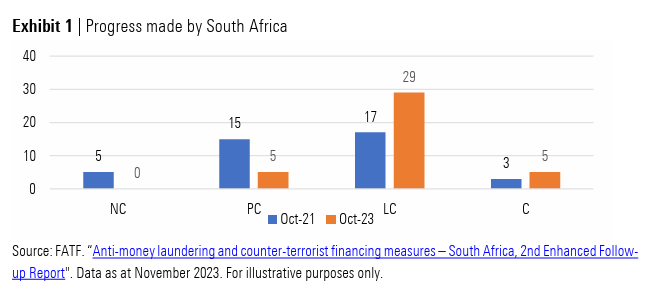

On 24 February 2023, South Africa was placed on the Financial Action Task Force (FATF) list of “jurisdictions under increased monitoring” (more commonly known as its “grey list”). This was based on the October 2021 County report that identified certain areas of non-compliance (NC) and partial compliance (PC). As a reminder, the FATF has a list of 40 recommendations1, where members are expected to achieve satisfactory levels of compliance. The other levels of compliance are largely compliant (LC) and compliant (C).

As per the October 2021 report, South Africa had five areas (out of 40) of non-compliance, 15 areas of partial compliance, 17 areas of being largely compliant and three areas of being fully compliant. South Africa was then given time to address these concerns, however, we couldn’t do so adequately in the time given and were subsequently added to the grey list on 24 February 2023.

Update and progress

During October 2023, the FAFT conducted an exercise to determine the progress we have made since being added to the grey list. These findings were subsequently published in November 2023. Based on this report, South Africa seems to have made significant progress in addressing most of the concerns. Most notably, no areas of non-compliance were identified, and the areas of partial compliance decreased from 15 in our previous report to only five in the latest progress report. The below graph provides a visual representation of the overall progress made. As can be seen in Exhibit 1 below, South Africa’s entire “distribution” has shifted to the right, which is where we want it to be.

This is very positive, however on two of the recommendations (R) — R.2 and R.32 — we have not made sufficient progress. Let’s delve a bit deeper into what still needs to happen.

Recommendation 2 (R.2) — currently rated partially compliant (PC)

The first two general recommendations (R.1 and R.2) of the FATF both focus on Anti Money Laundering and Combating the Financing of Terrorism (AML/CFT), with R.2 emphasising the importance of national cooperation and coordination. Specifically, the recommendation requires that countries should have AML/CFT/CPF policies in place which must be informed by a risk-based approach, regularly reviewed and that should designate an appropriate authority that coordinates such policies. Countries should also ensure that those responsible for policy creation, financial intelligence, law enforcement, supervisory actions and other relevant authorities can cooperate and coordinate their efforts as well as exchange information.

Read more in Daily Maverick: SA may have lengthy, perilous road to navigate in order to escape greylisting

From the feedback in the updated report, it seems that South Africa is still lacking in its coordination and holistic implementation of AML/CFT efforts across the major relevant and responsible parties. The inability to appropriately integrate our AML and CFT policies and coordinate amongst different parties ultimately constrains the effectiveness of the policies.

Recommendation 32 (R.32) – currently rated partially compliant (PC)

This recommendation is all about Bearer Negotiable Instruments (BNI) or “paper documents which have monetary value to the individual possessing them and are in a form where ownership or title passes upon delivery”3.

Before we delve into recommendation 32, it’s worth defining BNI’s a bit more simply. Those of you who might recall Bruce Willis running around barefoot in the Nakatomi building trying to save the day all by himself in the movie Die Hard might also remember that the bad guys were after negotiable bearer bonds.

Negotiable bearer bonds are basically untraceable paper bonds and whoever holds them in their hands becomes the owner. This is also one of the obvious reasons why they are so popular among criminals. Of course, the most popular BNI is simply cash.

R.32 deals with how we manage, monitor and restrict BNI (cash) coming into and out of South Africa. South Africa will therefore have to implement additional measures to effectively manage how cash enters and exits our country’s borders and address the notion that South Africa has become a very convenient hub for criminals and their various networks and syndicates to funnel their proceeds through.

While we have made some significant progress across the board, we need to urgently address these two recommendations along with those recommendations still classified as only partly compliant.

The hope is that we address this during 2024, however, it’s going to be a very busy year ahead. Legislators are nearing the end of their term in office, campaigning for reelection and will have to wait and see who will eventually end up in our new 28th Parliament.

In his State of the Nation Address on 8 February, President Cyril Ramaphosa stated that steps have been taken “including through new legislation, to strengthen our ability to prevent money laundering and fraud and secure our removal from the “grey list” of the Financial Action Task Force. According to the President, a digital forensic capability has been set up to support the NPA Investigating Directorate, which in due course will be expanded to support law enforcement more broadly. He further added that “legislation is currently before Parliament to establish the Investigating Directorate as a permanent entity with full investigating powers.”4

Thus far, it appears that greylisting has had a limited impact on our financial markets. Bond yields are trading at similar levels to where they were before the announcement. Although the current levels of the JSE ALSI are slightly off, when compared to the levels at the end of 2022, these are acceptable.

One could argue that should we not address the outstanding concerns timeously and therefore stay on the grey list longer than expected, capital markets might be inclined to demand a further increase in our risk premium. We have most certainly seen additional administration and operational difficulties when it comes to enhanced due diligence procedures which has led to increased overall time spent and transaction costs. DM

The ANC selling our foreign policy to Iran is not helpful in getting off the grey list

Recommendation 2 is the one which will cause problems in South Africa. Designating a responsible authority acceptable to international financial instituions in a government and bureaucracy riven by factions and corruption will be, shall we be polite, “a challenge.”