Over the past three months, it has become evident that the anticipated strong recovery of the Chinese economy is unlikely to materialise, which has dampened the mood among many commodity exporters.

The headwinds facing the Chinese economy are mounting, with the country’s shrinking labour force standing out as a potential long-term obstacle to becoming the largest economy in the world.

China’s labour force has steadily declined since it peaked in 2014 at nearly a billion people.

In July last year, the United Nations announced a revision of its demographic forecasts for China, stating that the working-age population could decline by 25% in 2050 and continue declining to less than 400 million by the end of the century.

Combined with an ageing population, this poses significant problems for the world’s second-largest economy, which has relied heavily on an expanding and relatively inexpensive labour force for several decades.

Pressure will inevitably mount on the fiscal ability to maintain the pension system, which offers basic coverage to more than 1 billion people.

Another macroeconomic challenge, which is a rarity in most other emerging markets, is the decline in the country’s consumption propensity. Many people who are either unemployed or only hold temporary jobs have reduced their spending, resulting in a spike in savings, which is detrimental to economic growth in the short to medium term.

According to China’s central bank, household deposits increased by almost $2.6-trillion in 2022, a whopping 81% higher than the increase recorded in 2021.

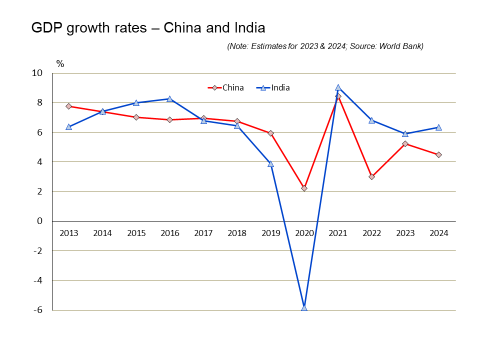

India, on the other hand, is on the rise. It has just replaced China as the most populous country in the world, and its economy is expected to outperform the Chinese economy in 2023 and 2024, at least.

A particular point of concern for Chinese policymakers is the weak performance of exports, with 2023 expected to be the second successive year of negative volume growth. In sharp contrast, India’s export volume growth averaged more than 12% per annum over the past two years and is forecast to also record positive growth in 2023.

The flaws of communism

Unfortunately for China, it seems that the inherent flaws of central economic planning that characterise communist regimes are finally taking their toll.

Although voluminous empirical research has been conducted that confirms the positive relationship between capital formation (fixed investment) and economic growth, a caveat is present in the form of the nature of the economic system.

It is impossible for a group of people composed of politicians, military leaders and bureaucrats to replicate the self-correcting mechanisms and tendency towards a market equilibrium that characterises free enterprise. State-owned banks are also inferior to private banks in allocating capital.

China’s government has overestimated the demand for housing and spent way too much on urban infrastructure, without consideration of the relative returns on capital. To make matters worse, the country’s current head of state has reverted to more autocratic policies, which have made investors nervous.

In recent weeks, one of the largest venture capital firms in the world, Sequoia, has divested from China.

The upshot of the significant lowering of China’s long-term growth prospects is the possibility that the US will retain its position as the largest economy in the world indefinitely.

In 2011, Goldman Sachs predicted that China’s GDP would become larger than that of the US by 2026 and become more than 50% larger than the US by 2050. This prediction has recently been revised, with China’s economy now only expected to surpass the US in 2035 and eventually peak at 15% higher.

Other research firms, including Capital Economics, do not expect China’s economy to ever overtake that of the US, instead peaking at around 90% of the US economy in 2035.

Depending on the assumptions for the future growth rates of the two countries, a realistic outcome is one that approximates economic parity in the next 15 years, which may be maintained well into the future.

Such a scenario could lead to a larger degree of geopolitical stability, as long as China resists invading Taiwan. DM