History offers us a powerful perspective in this process. Atul Gawande, a surgeon, author and science writer for the New York Times, provides fascinating insights in his seminal book, Being Mortal, into how the social fabric of the United States changed irrevocably on the heels of a trifecta of crises in the early 1900s. In quick succession, the US experienced World War I, the Spanish Influenza, and then a final blow with the long, drawn-out Great Depression.

Gawande argues, among other things, that while the Spanish flu accounted for more lives lost than in the war, the real casualty of that era was the American multi-generational family. This fragmentation took place as the young and able moved away from their homes – either to fight or find employment in the cities.

One of the lingering consequences of the fragmented family was that the elderly, left alone, started to fill up “poor houses” or, in today’s terms, homeless shelters.

In response to this worrying development, the US government passed the Social Security Act of 1935. The concept was simple: use a portion of one generation’s income to fund a safety net for the previous generation that could support them in old age. However, an interesting thing happened. Even with funds now flowing into the hands of those who needed to be cared for, this still didn’t result in getting the elderly out of the poor houses. The reason was simple: there was nowhere else for them to go. Funding the building of infrastructure to support the elderly was not part of the investment mandate.

It’s a story familiar to South Africans. Historically, under apartheid, migrant labour forced young men and women to move to cities and frayed the threads of the family fabric. But, 20 years later, we still haven’t got it right – just look at the recent case of Life Esidimeni where 145 lives were lost because South Africa does not provide proper facilities for those incapable of caring for themselves.

We don’t need a pandemic to recognise that the inexorable change in social dynamics that has been quietly building up in this country will lead to a far more serious problem than either cash in hand, or a CPI + 5% return from a pension or social security fund can address.

Time to focus on where the money is coming from

Consider the crises of the moment. We have locked our doors against a pandemic that threatens not just lives, but the livelihoods of an entire population. At the same time, we are witnessing a global financial meltdown which suggests that any retirement savings we have accumulated are now in jeopardy. If we look at these dilemmas through a narrow lens, our first priority will be to focus on one issue only: Where will we get the money to live?

Apply a broader lens to the problem and we begin to see that there is a far more concerning issue which has evolved over the last few decades. The fact is that our systems of social protection will be inadequate for these crises. The harsh reality is that they were probably not suited to the South African or African priorities in the first place.

Before the current financial crisis, compulsory savings in South Africa represented over R1-trillion; prudent fiduciary guidelines ensured that the bulk of that money was channelled into listed assets. But what we should have been paying closer attention to was the fact that listed capital markets for most developed economies were evolving to the point where they were no longer the economic growth engines or catalysts for job creation they once were.

A cynical view might suggest that they had almost become the playthings of what Thomas Piketty described as the rentier elite – that small segment of society that had learned it was far more profitable to create money out of other people’s money than it was to actually produce things. Divested, by Ken Hou-Lin and Megan Tobias Neely, goes so far as to suggest that rising inequality, particularly in the world’s most powerful capital market, the US, is less about being a “natural” result of apolitical technological advancement and globalisation, or the necessary price we have to pay for economic growth. “Instead, the widening economic divide reflects a deeper transformation of how the economy is organised and how resources are distributed.”

More growth engine, less self-interest

Why should we care about these points in our economy? Because our listed capital markets, specifically our stock market, which we have often lauded as being of the same order as the most developed markets in the world, has become exactly that: Less about being a growth engine for the kind of South African economic development that is desperately needed and more about being a platform for companies whose economic interests are focused elsewhere.

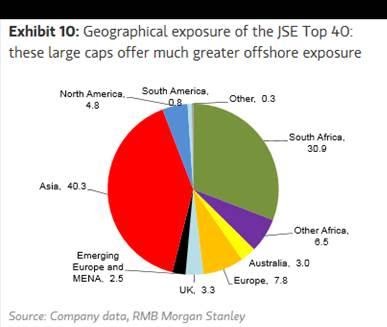

As the pie chart highlights, perhaps the question that fiduciaries should be asking is: Does investing in the JSE actually fuel the kind of economic growth that will address South Africa’s sustainable development goals?

Perhaps it’s time we become clear about what the real liabilities are for members of our compulsory savings funds. As Gawande points out, getting a financial return on a social security safety net isn’t enough if those contributions haven’t been deployed to ensure that the infrastructure exists to assist people in their time of need. It means absolutely nothing to achieve a return in excess of local inflation from our investments if South Africans are faced with a world where they might have to buy the air they breathe or the water they drink. What use is a CPI + 5% return if we are forced to rebuild our homes every three years because of the increase of veld fires due to climate change? Or if we are unable to address the ever-escalating rate of increased costs in healthcare, or continue to fail to provide meaningful education, affordable housing, or food security?

Grappling with the issues post-lockdown

When South Africa went into lockdown on 27 March, a small group of us started tackling exactly that question. We represent a collaborating cross-section of investment specialists, academics, and international agents who believe there is a far more meaningful way forward for us to fund the social safety net that South Africa desperately needs – and still provide a financial return to members of these funds.

Achieving that end will demand that we completely rethink how we use the funding mechanisms and capital markets at our disposal. Our modelling for the optimal investment portfolio for the future will have to consider not just the trade-off between risk and return, but the impact of every R100 that our members entrust to us. It means that we will have to use the funding mechanisms of both the listed and unlisted capital markets. But this can only happen if we change our current mindsets regarding the right business models for investing, and the right regulatory framework to capitalise on this requirement.

It also means that for us to get the ultimate leverage from this opportunity, the world of pension fund management will have to become less focused on competing with each other for the highest returns and far more collaborative on how we can create the right investable vehicles to create targeted outcomes for South Africa. We will have to come together and agree upon the right metrics and governance criteria to assure those members that their assets are being responsibly deployed.

It means that we will have to carefully map out exactly what South Africa’s funding needs are to measure up as a minimum viable sustainable economy.

So, let us end with this provocative question: Do you actually know what sort of impact your invested savings are having on creating a better world for you to live in? Perhaps it’s time we start thinking of our social protection models from that perspective. BM