(Photo: iStock)

(Photo: iStock) Question: My wife recently died and our daughter will be receiving a death benefit payout from her company provident fund. (This is in addition to the group life benefit she had.) We were told that this benefit would be taxable and that we have the option of taking it as a lump sum or as a living annuity. Which option will be the most tax-efficient?

Answer: There are two types of death benefits you can have as part of your company’s employee benefits structure.

The one is an approved death benefit, where you receive a tax break on the contributions but the proceeds would be taxable.

The other is called an unapproved benefit, where you receive no tax break on the contributions. However, the proceeds would not be taxed (apart from estate duty).

The benefit you are talking about here is an approved benefit and you would be liable for tax.

Lump sum option

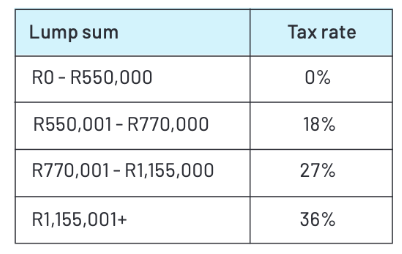

If you took a lump sum, it would be taxed according to the lump sum benefit scale. This would be as follows:

As these death benefit payouts are usually two or three times the person’s annual salary, the tax payable will be high. You could lose about one-third of the benefit in income tax if you take the full lump sum. Once you have the lump sum, however, you can invest it wherever you like.

Living annuity option

The other option is to consider using the proceeds to buy a living annuity in the name of your daughter. There will be no income tax payable on the lump sum that gets transferred to the living annuity. There will also be no estate duty payable.

The only tax payable will be on the income that your daughter receives. As your daughter is unlikely to be earning any money, the first R95,750 she receives each year will not attract any income tax.

The living annuity you would set up for your daughter should be invested in a portfolio that takes a long-term view. You should be looking for a return of inflation plus 5%, but without exposing the portfolio to too much short-term risk.

You should not be taking more than 4% out of the living annuity each year. This will result in your daughter having an income that increases with inflation and should last her for the rest of her life. This is a fantastic legacy from her mother.

If your daughter needs a higher income, you can increase the drawdown rate up to a maximum of 17.5%. This will, however, mean that the capital will become exhausted. I would recommend that you speak to a financial planner who can work out the optimum drawdown level for you to ensure that you do not run out of funds before your daughter becomes self-sufficient. DM

Kenny Meiring is an independent financial adviser. Contact him on 082 856 0348 or at financialwellnesscoach.co.za. Send your questions to kenny.meiring@sfpadvice.co.za.

This story first appeared in our weekly Daily Maverick 168 newspaper, which is available countrywide for R29.

Comments

Scroll down to load comments...