A person flies a dragon shaped kite on the Bund in front of buildings in Pudong's Lujiazui Financial District in Shanghai, China, on Tuesday, 9 January 2024. (Photo: Qilai Shen/Bloomberg)

A person flies a dragon shaped kite on the Bund in front of buildings in Pudong's Lujiazui Financial District in Shanghai, China, on Tuesday, 9 January 2024. (Photo: Qilai Shen/Bloomberg) “RRR cuts will likely be more infrequent going forward, and only used as a signal tool when markets are performing particularly poorly,” said Ding Shuang, chief economist for Greater China and North Asia at Standard Chartered Plc. “Structural tools will play an even bigger role.”

Goldman Sachs Group Inc. economists said Wednesday evening that they see the PBOC lowering rates in the first and third quarters, and deepening RRR cuts in the second and fourth quarters.

Governor Pan Gongsheng’s decision to personally announce the RRR cut, instead of waiting for state agencies to publicize it, came after a similar move by Premier Li Qiang. Earlier this month, China’s No. 2 official took the unusual step of revealing China’s GDP figure for 2023 before the statistics bureau.

Both moves show the emphasis top Communist Party figures are putting on boosting confidence. That reflects the urgency facing President Xi Jinping’s government to respond to calls for more aggressive stimulus as the economy grapples with a real estate slump, lingering deflation, shattered confidence and a $6 trillion stock market rout.

Pan stressed policymakers will have more room to take action this year, citing signs of forthcoming easing by the Federal Reserve as one factor. The central bank chief also mapped out ways to deliver financial support to key sectors.

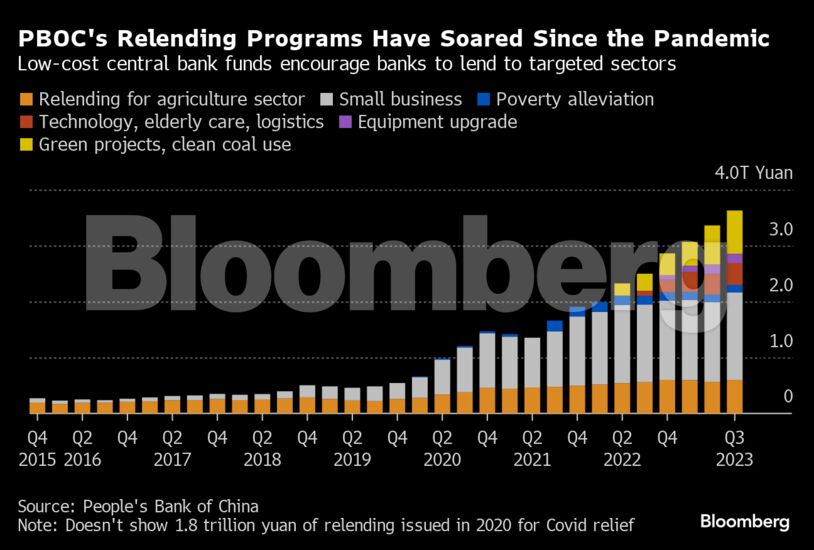

The PBOC will set up a new credit market department to promote financing to technology, green and other sectors, he said. It’s also cutting the interest rate on more than 2 trillion yuan ($279 billion) of low-cost funds for banks — a move intended to encourage more lending to agriculture and small firms.

“Setting up a new department is a signal that structural tools will guide funds into the real economy and key sectors that are given priorities to grow,” Ding said.

| Read More About China’s Economy: |

|---|

The PBOC has increasingly leaned on tools that steer credit to specific sectors since 2020, when the pandemic hit economic growth. That marks a departure from its former strategy of moving toward influencing borrowing costs via adjusting its policy rates, and largely letting investors determine where the money would go.

That kind of broad easing may be seen by the PBOC as carrying risk, said Larry Hu, head of China economics at Macquarie Group Ltd. Such policies allow money to flow into troubled areas, such as the property sector and indebted local governments, he added.

Pan’s continuation of that focus on structural tools indicates the central bank wants to make sure money is going to the areas it thinks will benefit the economy. The trade off is that price signals won’t play as large a role here.

What Bloomberg Economics Says ...

“There’s little doubt the People’s Bank of China will deliver more stimulus on top of the latest reduction in bank reserve requirements — Governor Pan Gongsheng made that clear when he laid out the PBOC’s price objectives, the economy’s challenges, and the central bank’s room for maneuver on Wednesday. We now expect more easing than we did in November. The extra effort is likely to take the form of deeper reductions in the RRR.”

— Chang Shu and David Qu, economists

Read the full report here.

Ding from Standard Chartered and others have said the PBOC may introduce more relending tools to ensure credit flows to channels in line with the ruling party’s broader objectives. The central bank has listed small businesses, the digital economy and elderly care as other favored sectors.

There’s also potential for the PBOC to dip further into its Pledged Supplemental Lending funds — a controversial tool that involves injecting low-cost funds into policy banks to support housing projects. Some economists have called this a form of “Chinese-style quantitative easing.”

In China, “structural tools indeed account for a larger portion than in advanced economies,” Macquarie’s Hu said. “It’s a monetary policy framework with Chinese characteristics.”