Overall, PGM producers expect the cycle to eventually turn in their favour amid signs that demand for hybrid vehicles is overtaking pure electric vehicles. (Photo: supplied)

Overall, PGM producers expect the cycle to eventually turn in their favour amid signs that demand for hybrid vehicles is overtaking pure electric vehicles. (Photo: supplied) To wit, Amplats said it expected headline earnings for the six months to the end of 30 June to fall by 65% to 75% compared to the corresponding period last year. This means they are expected to range between R6.7 billion and R9.4 billion versus R26.7-billion in 2022.

That's a steep fall, and to put it into broader perspective, last year's earnings were also down from the previous year. But 2021 saw record earnings across the platinum group metals (PGM) sector, largely because of record prices.

In commodities, the laws of economic gravity hold that what goes up must come down.

Amplats said the main reasons for its expected fall in earnings were declines “in rhodium and palladium US$ prices, which were 47% and 29% lower respectively”.

“Furthermore, sales volumes from own production (excluding trading) were 12% lower compared to H1 2022. This reflected lower refined production as a result of the Polokwane smelter needing to ramp-up in January following its rebuild; scheduled annual maintenance and asset integrity work at the processing operations; and the impact of Eskom load-curtailment, which resulted in deferred production of 66,400 PGM ounces,” the company said.

This points to the headwinds that have confronted the sector in the wake of its sizzling performances in 2020 and 2021.

Let's start with prices. In March/April of 2021, rhodium’s price reached record highs of almost $30,000 an ounce, making it the most valuable precious metal in recorded history. Palladium at the time was near $3,000 an ounce. It was a combination that flowed to the bottom lines of PGM producers, especially those with decent exposure to rhodium and palladium.

Both are crucial catalysts to cap emissions generated by petrol engines, and in 2021 there were concerns about widespread shortages especially as Chinese demand was seen ramping up. Emissions regulations in key markets such as the European Union had also been tightening.

Rhodium has long since fallen back to Earth, fetching just over $4,000 an ounce, while palladium is below $1,300 an ounce. Among other things, an uneven rebound in the global economy from the pandemic meltdown, overblown (in hindsight) concerns about shortages, and question marks about the role PGMs will play in the green energy transition have all taken the shine off rhodium and its peers.

South African platinum producers as a result have seen earnings and their share prices fall. Amplats share price is down almost 40% in the year to date (YTD), and lost over 3% on Monday alone at one point after its trading statement came out.

Impala Platinum’s share price so far in 2023 has also lost almost 40%, Northam Platinum’s is around 28% lower, and that of Sibanye-Stillwater (which has a more diversified production profile, including gold) is down around 32%.

One of the perplexing things about this state of affairs is that PGM production in South Africa over the past 12 months or so has been steadily declining. South Africa remains by far the largest producer of PGMs as a basket, and is second only to Russia when it comes to palladium. (A Russian product that is not subject to sanctions).

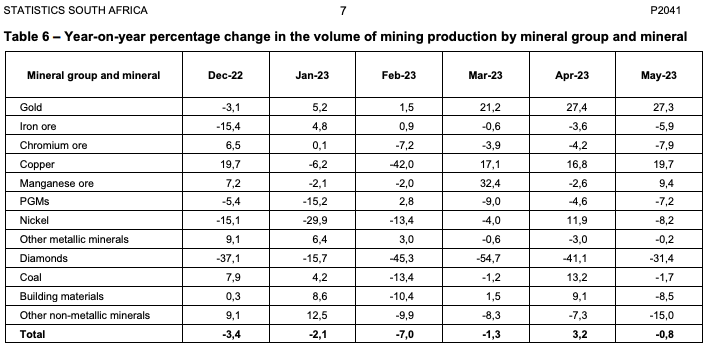

According to Statistics South Africa (Stats SA) data, mining production in South Africa fell for 14 consecutive months on a year-on-year basis until April this year when it rose 3.2%. And PGMs have generally been leading this downward trajectory.

In the first five months of 2023, PGM production in South Africa fell on an annual basis every month except for February, when it grew 2.8%. In January it fell 15.2%.

Last year was also a tale of PGM production decline. In October it fell almost 34% on an annual basis, and it only had mild annual expansions in 2022 in May of 3.3% and January of 1.3%.

Which begs a couple of questions. The first is why the falling production and second, why are prices not perking up as a result?

Amplats provided some details in its trading system about falling output: the ramp up at the Polokwane smelter, scheduled maintenance, and of course the impact of surging power cuts which it says cost it over 66,000 ounces in production.

A couple of factors are pointedly not in the mix. One is the labour ructions that undermined the sector from just over a decade ago when the Association of Mineworkers and Construction Union (Amcu) exploded onto the scene. All the major PGM producers in South Africa have multi-year wage deals in hand that were reached without any tools being downed.

Another is social unrest and criminality, which according to industry insiders has declined markedly with improved cooperation between the companies and the police. So production is being hampered by technical factors and Eskom.

So, why are prices not responding to production which has been steadily falling for over a year?

Well, in 2021 — looking at the archived Stats SA data — production began soaring in March on an annual basis, though of course that was from a low base because of the initial closing down of operations in 2020 under the hard lockdowns to contain the Covid pandemic.

In April 2021, PGM output in South Africa soared 276% year-on-year and for most of 2021 production grew robustly each month on an annual basis — and that was in a high price environment, the best of both worlds as it were. So the production decline since early 2022 has been off a relatively high base.

And the global economy is still not shooting the lights out. The initial doom and gloom forecasts for 2023 by the IMF have not come to pass, but global economic growth is still seen slowing to 2.8% this year from 3.4% in 2022. That is simply not good for most commodities with industrial applications, unless there is a really severe shortage.

The bottom line is that South Africa's PGM sector is now in a situation where both prices and production have been falling, and that is going to hurt bottom lines. But at least it does not appear to face the prospect of fresh labour turmoil.

And the price/earnings ratios of South Africa’s main PGM producers are all below 5.0, which certainly suggests there is value to be had in the sector. There is a silver lining in these trends and South Africa’s PGM sector may yet regain its mojo.

Good Investing.

Ed