(Photo: Getty Images / iStockphoto)

(Photo: Getty Images / iStockphoto) The system will allow you to access a portion (30%) of your retirement savings for emergencies, while ringfencing the remainder (70%) for your retirement. However, while draft legislation around this was widely expected to be released today, this did not happen. Instead, the Budget Review makes vague reference to “forthcoming draft legislation” later this year.

Retirement reform executive at Old Mutual Michelle Acton says that although the industry is doing all it can to prepare for implementation, (companies) cannot undertake any work on system development until the reforms are passed into law. She adds that the amount of work needed to ensure readiness is far-reaching, as entirely new and sophisticated automated systems will have to be developed to enable fund members to efficiently access the allowed accessible portion of their savings. Old Mutual estimates that the new level of accessibility will lead to a 300-400% increase in claims to be processed by administrators.

The new two-pot system would have to allow for member-initiated claim functionality because, for the first time, members will have to register their claims without going through their employer. This is likely to require member engagement through an automated digital platform; the retraining and capacitating of entire new call centres; fraud and risk prevention measures.

“The administrative changes will be the biggest ever seen in the retirement industry in South Africa and means the need for an entirely new processing and service model. We will have to build a brand-new system overlayed on the existing system. This will take a massive amount of budget and resources which requires at least 12 to 18 months to build,” Acton says.

Finance minister Enoch Godongwana flagged four areas of retirement reform that needed “additional work” — a proposal for seed capital, legislative mechanisms to include defined benefits funds in an equitable manner, legacy retirement annuity funds and withdrawals from the ringfenced retirement savings if you are retrenched and have no alternative income.

Visit Daily Maverick's home page for more news, analysis and investigations

Blessing Utete, managing executive of Old Mutual Corporate Consultants says the seeding relates to a portion of current savings being used to seed the accessible savings pot up to a regulated capped amount.

“The Minister would have to provide specific details on how this would work to ensure the stability of funds and protection of member retirement funds and protection of member retirement fund outcomes,” Utete says.

Withdrawals tax — two-pot system

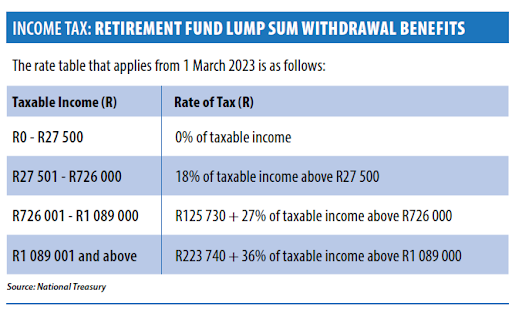

Withdrawals of any funds saved before 1 March 2024 will be taxed according to the retirement lump sum withdrawal tables. After 1 March 2024, any withdrawals from your “savings pot” will be taxed at marginal rates or the same rate at which you pay personal income tax. So, if your tax rate is 40%, you will pay a 40% tax on whatever you withdraw from your “savings pot”.

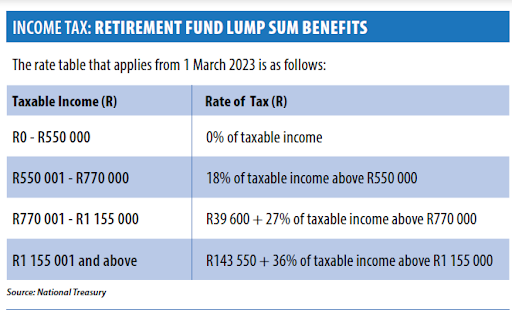

It’s another disincentive, which is great and is likely to make retirement fund members think twice before making that withdrawal. When you retire, any remaining amounts in your “savings pot” will be taxed according to the retirement lump sum table where you can access a lump sum of up to R550 000 tax-free.

Retirement fund contributions will remain deductible up to R350,000 or 27.5% of your taxable income a year, whichever is lower.

Withdrawals tax – 2023 inflation adjustments

The tax brackets for retirement fund lump sum benefits, and lump sum withdrawals have been adjusted upwards by 10% to compensate for inflation. This means that when you retire, the first R550,000 lump sum you withdraw from your benefits will be tax-free (up from R500,000). If you choose to make an early lump sum withdrawal before you retire, the initial tax-free amount is R27,500 (previously R25,000). DM/BM