Illustrative image | Sources: Rawpixel | iStock

Illustrative image | Sources: Rawpixel | iStock According to the Association for Savings and Investment South Africa (Asisa), while 293,423 new policies were sold during the six-month period to the end of June 2022, 319,318 policies were surrendered. A surrender occurs when the policyholder stops paying premiums and withdraws the fund value before maturity.

“This is not surprising, since consumers are far more likely to surrender their savings policies during tough times to access their savings to cope with financial hardship,” says Hennie de Villiers, the deputy chair of the Asisa Life and Risk Board Committee.

There were 34.3 million recurring premium risk policies (life policies, funeral policies, credit life policies, disability policies, severe illness policies and income protection policies) in force at the beginning of this year. However, while consumers bought 4.4 million new risk policies in the first six months of this year, 4.3 million risk policies have lapsed and claims against 199,023 policies were submitted. This resulted in a marginal drop of 0.1% to 34.2 million in recurring premium risk policies at the end of June 2022.

Visit Daily Maverick's home page for more news, analysis and investigations

De Villiers says although the number of claims dropped significantly in the first half of this year, there was a further marginal decline in the number of endowments and retirement annuities, from 5.75 million policies at the start of the year to 5.71 million by the end of June. This is also a significant year-on-year decrease, falling by 4% from 5.95 million policies at the end of June 2021.

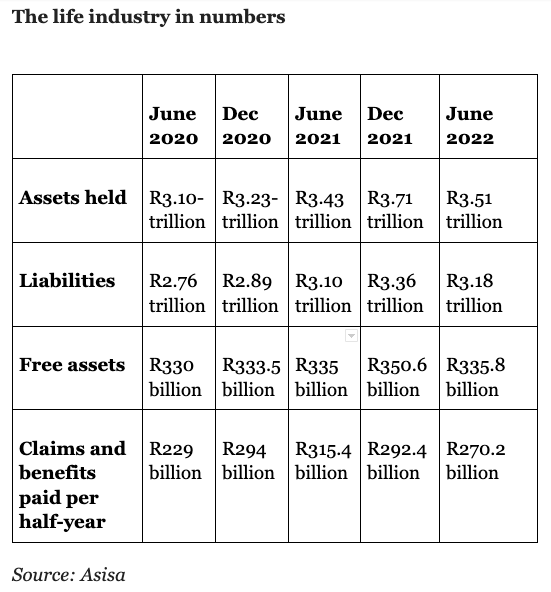

Asisa’s statistics show that the life insurance industry held assets of R3.51-trillion at the end of June 2022, while liabilities amounted to R3.18-trillion. This left the industry with free assets of R335.8-billion, more than double the reserve buffer required by the solvency capital requirement (SCR), for the first time since 2020. A healthy reserve buffer is of critical importance because it enables insurers to pay claims and policy benefits even in times of extreme market turmoil and/or unusually high claims.

Policyholders and beneficiaries received claims and benefit payments worth R270-billion in the first half of 2022. These payments included retirement annuity and endowment policy benefits as well as claims against life, disability, severe illness and income protection policies.

De Villiers points out that consumers have had to absorb unprecedented fuel price increases as well as higher food prices and rising interest rates in the first half of this year. At the same time, 64% of South Africans between the ages of 25 to 34 were unemployed, according to the Quarterly Labour Force Survey for the first quarter of 2022.

“South Africans in this age group are meant to be economically active and under normal circumstances be concerned with buying risk cover to offer financial protection to their growing families as well as cover credit purchases such as mortgage bonds,” says De Villiers. However, many are likely to be reluctant to commit to monthly premium payments while living costs are at an all-time high.

De Villiers notes that even credit life policies failed to achieve meaningful growth in the first half of 2022, which indicates that consumers were either struggling to access credit or practising greater restraint when buying on credit.

The DebtBusters’ Debt Index for the second quarter of this year shows that consumers applying for debt counselling had 34% less purchasing power. The head of DebtBusters, Benay Sagar, says although nominal incomes were the same as 2016 levels, purchasing power shrank by 34% once cumulative inflation growth of 34% is factored in for the same six-year period.

“Inflation in 2022 is significantly higher than previous years; coupled with successive interest rate hikes and no growth in incomes, consumers are really feeling the pinch,” he says.

The Debt Index also provides some evidence of restraint when it comes to accessing credit, with the average number of credit agreements per consumer at near historic low levels. DM/BM