Stock market information displayed on a TV at the Nasdaq MarketSite in New York, US, on Wednesday, 15 June 2022. (Photo: Michael Nagle / Bloomberg via Getty Images)

Stock market information displayed on a TV at the Nasdaq MarketSite in New York, US, on Wednesday, 15 June 2022. (Photo: Michael Nagle / Bloomberg via Getty Images) “The Fed may have attempted to jolt the financial landscape with an aggressive attack on inflation, but stocks stuck to their 2022 playbook last week, falling to new lows amid volatile day-to-day trading,” said Chris Larkin, managing director of trading at E*TRADE from Morgan Stanley. “Investors are likely hoping for a bounce amid a short trading week and to snap the S&P’s weekly losing streak. That said, Fed watchers don’t have to wait long for more from Chairman Powell -- with testimony on deck, traders will continue to look for signs of a shift in sentiment.”

After unexpectedly accelerating to a fresh 40-year high in May, US consumer price growth is seen slowing, with a Bloomberg survey of economists predicting 6.5% by the fourth quarter and to 3.5% by the middle of next year.

Yet fears are rampant that Federal Reserve policy makers intent on cooling price pressures will go too far and trigger an economic slowdown. Strategists at Morgan Stanley and Goldman Sachs Group Inc. warned equities may have further to fall to fully price in the risk of recession, reflecting wider skepticism about Tuesday’s rebound.

“Investors are increasingly worried that sticky high inflation and a Fed that is clearly committed to reducing price pressures will result in a recession,” Dennis DeBusschere, founder of 22V Research, said in a note. “The bear market will end when the inflation/recession outlook becomes clear. Until then, bear market rallies and declines will remain the norm.”

Crude oil gained. Bitcoin scaled $21,000 as cryptocurrencies got a reprieve from recent turbulence. The dollar dipped and the yen hovered near a 24-year low, sapped by the contrast between a super-dovish Bank of Japan and a hawkish Fed.

European stocks extended a second day of gains, with automakers leading the advance in the benchmark Stoxx 600 Index.

How will the second half of this year play out for major asset classes? We are re-running MLIV’s 2022 asset survey from December to see how street views have evolved amid the turmoil and volatility in the past few months. Click here to participate anonymously.

What to watch this week:

- Fed Chair Jerome Powell semi-annual Senate testimony, Wednesday

- Bank of Japan April minutes, Wednesday

- Powell US House testimony, Thursday

- US initial jobless claims, Thursday

- PMIs for Eurozone, France, Germany, UK, Australia, Thursday

- ECB economic bulletin, Thursday

- US University of Michigan consumer sentiment, Friday

- RBA’s Lowe speaks on panel, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 2.5% as of 10:31 a.m. New York time

- The Nasdaq 100 rose 3%

- The Dow Jones Industrial Average rose 1.8%

- The Stoxx Europe 600 rose 0.4%

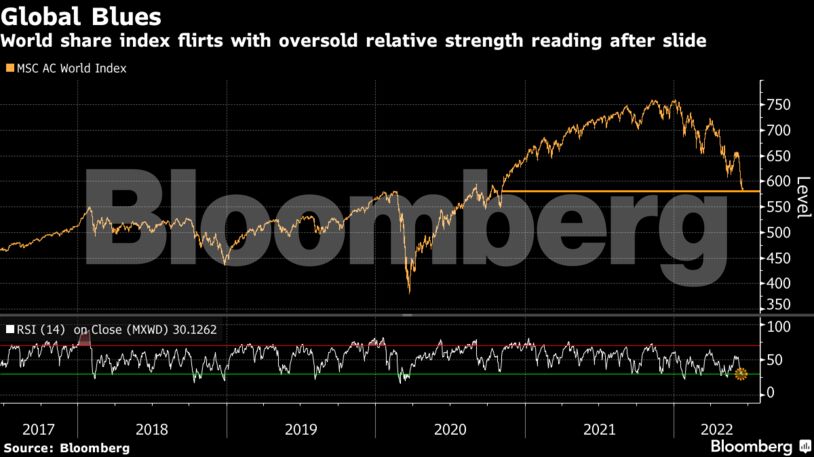

- The MSCI World index rose 2%

Currencies

- The Bloomberg Dollar Spot Index fell 0.1%

- The euro rose 0.4% to $1.0549

- The British pound was little changed at $1.2259

- The Japanese yen fell 0.8% to 136.19 per dollar

Bonds

- The yield on 10-year Treasuries advanced six basis points to 3.28%

- Germany’s 10-year yield advanced two basis points to 1.76%

- Britain’s 10-year yield advanced three basis points to 2.64%

Commodities

- West Texas Intermediate crude rose 1.6% to $111.28 a barrel

- Gold futures rose 0.1% to $1,842.60 an ounce

--With assistance from Robert Brand, Michael Msika, Denitsa Tsekova, Tugce Ozsoy and Andreea Papuc.