(Photo: Unsplash / Panyawat Auitpol)

(Photo: Unsplash / Panyawat Auitpol) A grudge purchase at the best of times, these policies kept many households from the brink of disaster during the worst of times.

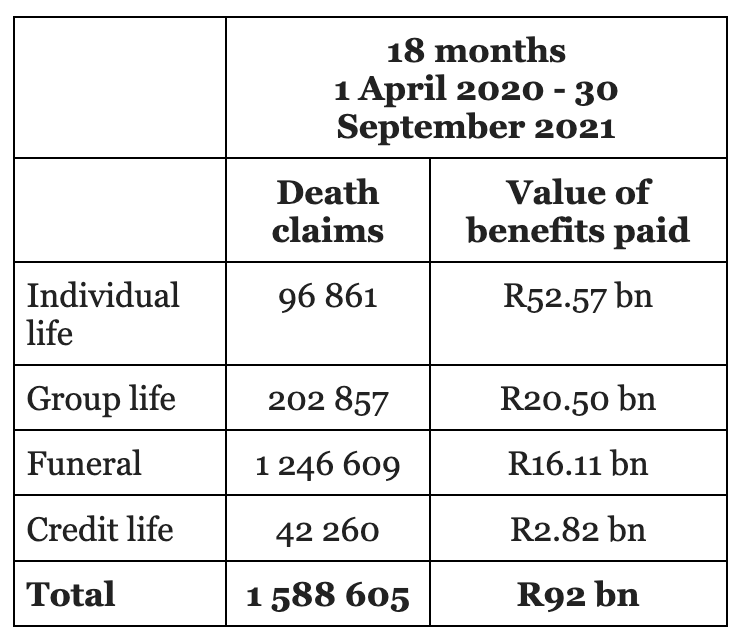

Statistics released by the Association for Savings and Investment SA (Asisa) reveal that in the 18 months between 1 April 2020 and 30 September 2021, 1,588,605 death claims, covering funeral, life, and credit insurance, were received by the life insurance industry. The value of the benefits paid out reached R92-billion in that period.

“These payments were made at a time when, aside from death and illness, families were battling with job losses and the SA economy was stuttering as a result of reduced retail spending and local and global restrictions that impacted on vital sectors like tourism,” says Hennie de Villiers, deputy chair of the Asisa Life and Risk Board Committee.

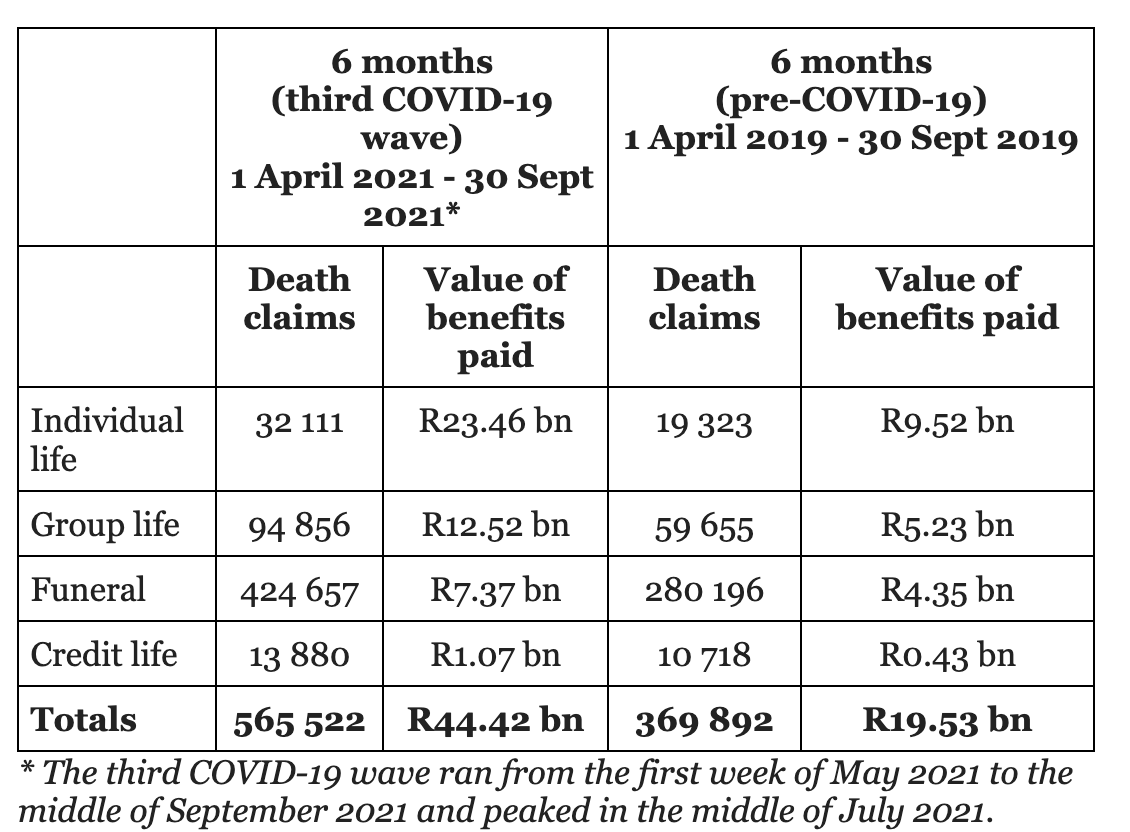

If one looks at the claims per time period, it is possible to track the growing severity of the pandemic. From 1 April 2020 to 30 March 2021, 1,023,083 claims worth R47.58-billion were paid out. The next six-month period, the peak of the third wave, shows that more than half a million claims (565,522) were received between 1 April 2021 and 30 September 2021 worth almost an equivalent R44.42-billion.

“The higher value of the payment demonstrates that the third wave hit the more affluent harder,” says De Villiers.

While the death rate has been lower during the fourth wave than in previous waves due to vaccinations and the emergence of the Omicron variant, death claims rates have not yet returned to pre-pandemic levels. “Less than 50% of our adult population has been vaccinated, which will remain an issue for insurers,” he says.

According to De Villiers, life insurers expect the relatively higher rate of death claims to continue until South Africans start embracing vaccinations as the new normal.

“There is overwhelming evidence that the risk of severe illness or death is lower in those who are fully vaccinated. A consistently higher claims experience will leave insurers with little choice but to adjust premiums in line with the higher risk presented by someone who is not vaccinated.”

De Villiers says that premiums have already increased in the group life insurance space, for example, but that employers that have implemented mandatory vaccination policies are starting to benefit from preferential premium rates.

During the various lockdowns, the government’s Covid-19 Temporary Employee/Employer Relief Scheme added a further R60-billion to the pockets of furloughed workers from inception in March 2020 to July 2021. However, this was not enough, and consumers have a new appreciation for risk insurance.

Life insurers noted a welcome drop in lapses on risk policy premiums in 2021 – after several years of an upwards trend of policyholders stopping their risk policy premiums.

“We now see consumers are prioritising their payments on these policies, ahead of other types of expenditure,” he says.

There has also been a notable uptick in the number of consumers opting into recurring premium risk policies (life, disability, dread disease and income protection cover).

“The reality is that most of us know at least one person who lost his or her life due to Covid-19,” De Villiers adds. “We also know of many more people who lost their income during the pandemic, highlighting the importance of having access to savings.”

Desperate times saw a higher number than usual of policyholders who surrendered their savings policies. While it’s not ideal, as it means that the policyholder has withdrawn the fund value before the savings policy has matured, it does show the value of a savings pot.

Death claims and benefits paid during the third Covid-19 wave

Asisa started tracking death claims against individual life, group life (offered by employers), credit life and funeral cover policies at the start of April 2020 to measure the impact of the pandemic on the long-term insurance industry.

Of course, not every death for which claims were submitted would have been caused by Covid-19, but there is no doubt that the pandemic has been responsible for many of the additional deaths, whether directly as a result of a person contracting the virus or because people were reluctant to seek medical attention for other serious conditions, says De Villiers.

Total death claims and benefits paid during the first 18 months of the Covid-19 pandemic

Despite the pandemic, SA’s life insurance industry remains resilient. The industry held assets of R3.71-trillion at the end of 2021, while liabilities amounted to R3.36-trillion. This left the industry with free assets of R350.5-billion, which is just under double the capital required by the solvency capital requirements. DM/BM