South African companies are facing domestic challenges to rail and port services, with logistics under duress from shipment delays. (Photo: EPA-EFE / Jim Lo Scalzo)

South African companies are facing domestic challenges to rail and port services, with logistics under duress from shipment delays. (Photo: EPA-EFE / Jim Lo Scalzo) The year 2021 could have been a breeze for the global economy, were it not for supply chain disruptions that saw everything from rubber and food to semiconductors and Christmas stocking fillers not only cost much more, but also take significantly longer to reach their destinations.

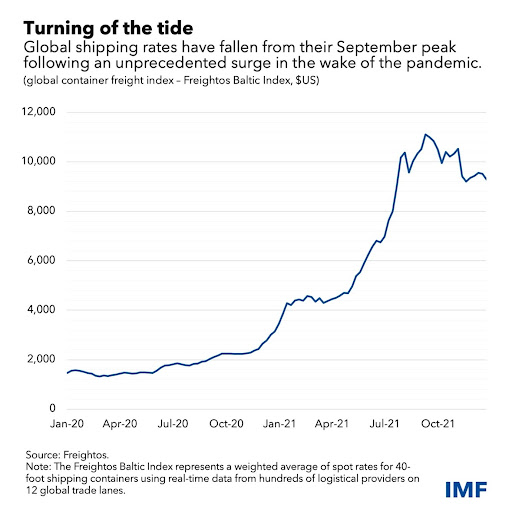

However, the good news is there are early indications that these supply constraints may be easing, with global shipping costs moderating by 16% late last year from their September peak, and the broader-based Federal Reserve Bank of New York’s gauge of global supply constraints slowing from its October high point.

But it’s worth noting that container costs remain four times their pre-pandemic rate.

For the first few weeks of January, all eyes have been narrowly focused on the interest rate trajectory that central banks in developed markets are likely to pursue, with as many as four interest rate hikes now expected in the US.

But it’s supply chain measures like these that deserve close watching, because, as the force behind last year’s inflation uprising, it is these dynamics that will largely determine the rapidity and extent of interest rate increases globally during 2022.

The IMF suggests there could be light at the end of the tunnel, but cautions that pressures do remain and that shipping rates could stay elevated through 2022.

In addition to backlogs and port delays, there are no quick fixes for labour shortages, supply chain disruptions moving inland and shipping industry challenges, such as slow capacity growth and a highly concentrated nature of the global market in carriers.

To solve what could otherwise remain long-term headwinds, the IMF says: “Returning to pre-pandemic shipping rates will require greater investment in infrastructure, digitalisation in the freight industry and implementation of trade facilitation measures.”

In the shorter term, the risks facing the global supply chain remain the usual suspects: Covid-19 and any new variants that may be in the offing, the state of the Chinese economy and the gap between consumer demand for goods and the supply capacity to meet these.

The emergence of the Omicron variant appears to be changing the trajectory of the pandemic, with debate over whether its fast spread, yet, fortunately, low mortality rates, is a precursor to achieving herd immunity or whether it marks the shift from a pandemic to a world in which Covid-19 becomes endemic.

Should the former be the case, the global economy could return to business as usual in the foreseeable future, with policymakers given the room to focus exclusively on unravelling the financial measures put in place to bolster the pandemic-racked global economy.

The alternative is that other virulent strains emerge, further disrupting supply chains and undermining economic recoveries. The World Bank has estimated possible downside risks for growth from Omicron (see graph below), with global growth adversely impacted by between 0.2 to 0.7 percentage points.

It adds: “The associated dislocations could also aggravate supply bottlenecks and exacerbate inflationary pressures.”

Possible Omicron-driven growth outcomes for 2022

/file/dailymaverick/wp-content/uploads/2022/01/BM-Sharon-analysis-SupplyChain-2.jpeg "Sources: Oxford Economics; World Bank. Note: AEs = advanced economies; EMDEs = emerging market and developing economies. Yellow lines denote the range of the downside scenario in which economies (18 advanced economies and 22 EMDEs) face a range of unanticipated pandemic shocks, scaled from about one-tenth to about two-tenths of the size of those from the first half of 2020.")

The latest World Economic Outlook paints a picture of a global economy already expected to slow from its 2021 rebound, with growth expected to be 4.1% in 2022 versus 5.5% last year. Its forecast factors in “continued Covid-19 flare-ups, diminished fiscal support and lingering supply bottlenecks”.

It explains: “The near-term outlook for global growth is somewhat weaker, and for global inflation notably higher than previously envisioned, owing to pandemic resurgence, higher food and energy prices and more pernicious supply disruptions.”

China to a large extent holds the key to the outlook for the rest of the world, given how much it imports and exports.

Robeco strategist Peter van der Welle positions the extent of China’s influence on the global economy: “In 2022, China will likely be top-of-mind for investors, even disregarding the Winter Olympics to be held in Beijing in February. China as a single country has determined around 30-40% of annual global GDP growth in the recent decade, and it led the global economic cycle into recovery in 2020.”

As one of the few remaining countries to still be pursuing a zero-Covid policy, its economy is most at risk of the spread of new variants, like Omicron, which is already seeing harsh shutdowns imposed to eradicate the strain.

After an eventful year — for many of the wrong reasons — China’s 2022 economic outcomes are arguably likely to be the most unpredictable of the largest countries. It is still trying to put out short-term fires like the fallout from the Evergrande property company default while steering the economy to its long-term target of achieving common prosperity. Economic growth for 2021 came in at 8.1%, ahead of its 6% target, but this year the World Bank expects it to achieve 5.1% — and in 2023, 5.3%.

This week the Chinese government moved quickly to buoy economic activity in 2022 amid the property industry fallout, reducing interest rates on its policy loans for the first time since April 2020 — shortly after the pandemic struck.

ING Greater China chief economist Iris Pang is confident that as the global economy recovers, stronger demand for goods will translate into stronger international trade for China. However, she notes that the challenges will continue to be freight delays and semiconductor shortages, because these cannot be solved instantly.

For now, however, 2022 seems to be getting off to a far gentler start than 2021. There may be some known unknowns that could prove disruptive — but at least they are known.

Also, after two years of uncertainty and challenges the likes of which we had never seen before, we’ve all paid our school fees, making it unlikely that there’s anything that could derail the economy as seriously as the pandemic did in 2020. BM/DM