PRIVATE HEALTHCARE COSTS

How much more will you pay for your medical scheme next year?

In previous years, schemes have typically exceeded the Council for Medical Schemes’ increase guidelines by about 4%.

Despite recommendations from the Council for Medical Schemes (CMS) to limit increases to 4.2%, most medical schemes have announced higher contribution increases for the 2022 year. However, some schemes have chosen to defer contribution increases by several months and even up to September 2022, in a bid to buy members some relief.

Jill Larkan, head of healthcare consulting at leading financial and wealth advisory business GTC, says that in previous years schemes typically exceeded the CMS increase guidelines by about 4%.

The CMS’s annual set guidelines for medical scheme contribution increases are based on a review of national and global macro-economic outlooks. This year the regulatory body has also taken into account the significant effects of the coronavirus pandemic on medical scheme reserves and member hospitalisation trends.

Larkan had anticipated that increases might be in line with the CMS recommendations based on consumers’ financial constraints, record reserves held by the medical schemes and lower-than-usual usage of medical scheme benefits over the past two years. She says combined medical scheme reserves have grown to a record R73.29-billion.

However, she warns that this behavioural pattern could reverse if Covid-19 vaccinations and infections combine to confer herd immunity on the population. In that case, members could flock back to doctors to catch up on delayed procedures and treat conditions that could have been worsened after a year of delayed care.

Larkan says medical schemes have a precarious balancing act ahead of them so as not to overburden struggling members on the one hand and ensure adequate reserves for their future care on the other.

However, the CMS is confident that medical schemes with adequate reserves should be “well insulated” against such a spike. The CMS guidelines also included a specific warning for medical schemes whose financial sustainability was already questionable pre-pandemic, advising them to consider “interventions such as amalgamating with other schemes”.

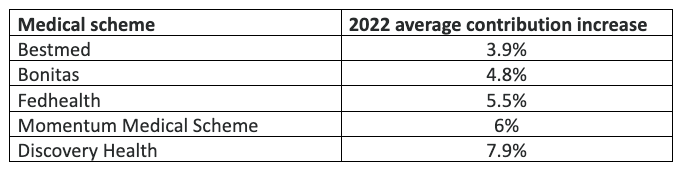

The country’s largest open medical scheme, Discovery Health, has chosen to defer increases for the second year in a row, with an average contribution increase of 7.9% kicking in from 1 May next year.

The scheme maintains that the increase is in line with medical inflation, estimated at 7.9% for 2022 and that a lower increase will place the scheme’s sustainability at risk.

Dr Ryan Noach, CEO of Discovery Health, the administrator of Discovery Health Medical Scheme (DHMS), says the deferral of the increases for 2021 and 2022 means that members will have an actual effective increase in total contributions of 2.9% in 2021 and 5.3% during 2022.

“At the same time, the scheme’s contributions are keeping pace with the medical inflation anticipated once Covid-19 becomes endemic in the healthcare system and avoids the need for increase ‘shocks’ at that time,” he says.

The scheme’s membership has grown by more than 27,000 over the past year and Noach says it is vital that contribution increases be priced correctly to allow for expected future healthcare utilisation.

“Setting contributions lower than medical inflation will result in contributions falling behind claims and lead to ongoing medical scheme losses, ultimately resulting in future contribution ‘shocks’ to maintain sustainability,” he says.

The Discovery Health Medical Scheme claims experience for 2021 shows that healthcare claims between Covid-19 waves are higher than pre-pandemic levels. For example, between waves of Covid-19 infection:

- Elective surgical admissions such as major joint replacements and cataract surgery increased to 113% and 120% of pre-Covid-19 levels respectively.

- New healthcare services required to diagnose and treat Covid-19 infections remain high.

“The claims experience of DHMS provides guidance on the expected future cost of healthcare claims between Covid-19 waves and once Covid-19 becomes endemic. The trends imply that medical inflation has persisted at a rate of 3% to 4% above consumer price inflation since 1 January 2020, and that we will be well positioned with contributions at the level of anticipated claims before considering contribution increases for 2023,” Noach says.

Momentum Medical Scheme has also chosen to defer increases and the scheme’s average contribution increase of 6% will kick in from 1 September next year.

Lee Callakoppen, principal officer of Bonitas, says the scheme trustees made a strategic decision to use about R600-million of reserves to ensure that 82% of members receive a below-CPI contribution increase for the 2022 benefit year.

The average contribution increase Bonitas announced for 2022 is 4.8%, with the premium for the lower-end Bonstart option actually decreasing by 7.9%, which Callakoppen attributes to the low cost versus benefits ratio and the younger membership profile on the plan.

“The CMS recommendation of increases of 4.2% carried the caveat that financial stability and sustainability of schemes must remain a priority. We feel that the use of part of our reserves to cushion members against increasing costs is an appropriate strategy,” he says.

Fedhealth followed suit by deferring contribution increases to April next year and will be using R105-million of its reserves to fund the difference. Fedhealth’s principal officer, Jeremy Yatt, says members face a 5.5% annualised increase next year and the scheme does not foresee any double-digit average increase for any benefit option, or any big swings in future contribution increases over the next few years.

Bestmed has managed to keep its 2022 contribution increase to 3.9% across all options.

Medical scheme loyalty likely to drop

Overall customer satisfaction of members of South Africa’s largest medical schemes has sharply declined this year, with some schemes recording their lowest customer loyalty scores over a six-year period.

The 2021 South African Customer Satisfaction Index for medical schemes, conducted by Consulta, covers the largest open medical schemes in the country — Bestmed, Bonitas, Discovery Health Medical Scheme, Medihelp and Momentum Medical Scheme. Bestmed emerges as the leader on overall customer satisfaction, with all other schemes performing on or below industry par.

Ineke Prinsloo, head of customer insights at Consulta, says the index findings are particularly significant right now with medical schemes announcing benefit changes and premium increases for 2022. Prinsloo says there are likely to be significant shifts of members to lower cost-benefit plans and between medical schemes as customers try to balance value, quality, necessity and affordability.

However, she says that while members will look for cheaper options, they are not likely to “buy down” on their expectations. “The impact of the pandemic on household income looms larger than ever, and as reluctant as members are to cut their medical scheme contributions, many have no other recourse,” she says.

Prinsloo adds that the industry could see more significant numbers of people opting out entirely or downgrading their benefits to basic core plans in the coming months, as they don’t perceive their current use as meeting their requirements or being reliable in their time of need.

“This trend of downgrading (or opting out) is already putting the funding model of medical schemes under pressure.

“Medical schemes operate on the principle of ‘social solidarity’ where all members within a scheme contribute equally to a pool of funds, whether young and healthy or elderly and sickly, expecting that they will all derive equal utility value from the scheme.

“The latest index shows that the healthy and younger members with lower or even minimal benefit utilisation are the least satisfied and loyal. Without focused intervention from medical schemes to address the drivers of customer satisfaction in this key demographic, medical schemes will soon find that the pool of funds to subsidise older, less healthy, higher utilisation members is shrinking, bringing the sustainability of the entire private healthcare funding model into question,” she says. DM/BM

Comments - Please login in order to comment.