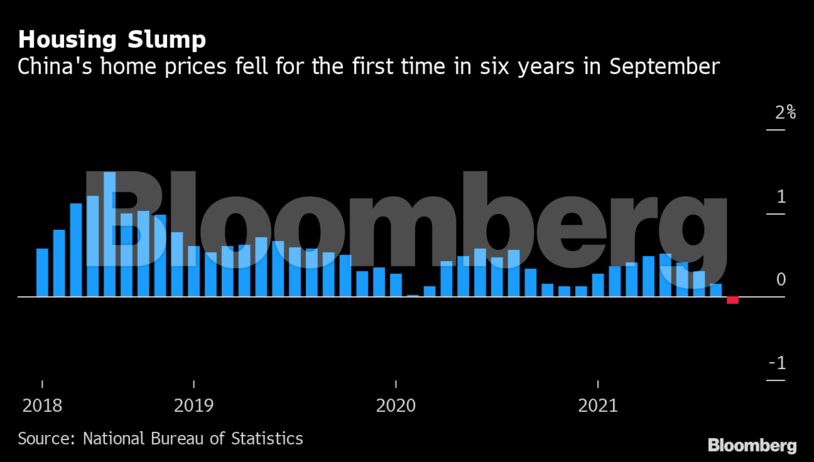

The slowdown in the home market is becoming more evident as debt-laden developers including China Evergrande Group struggle to raise cash and sentiment among homebuyers evaporates. That’s clouding the outlook for the economy, which depends on the broader property industry for almost a quarter of its output.

Falling home prices may fuel a vicious cycle by further weakening demand, worsening the cash shortage at builders and forcing them to offer bigger discounts. China’s economic growth slowed in the third quarter as the property and construction industries contracted for the first time since the start of the pandemic.

“The sector has clearly entered a downward cycle,” said Yan Yuejin, research director at Shanghai-based E-House China Research and Development Institute. “Usually a home market decline would persist for about eight months in China. Now the priority is to prevent a state of panic.”

September is traditionally a peak season for the home market. Yet residential sales tumbled 17%, investments slid for the first time since early 2020, and the rate of failed land auctions climbed to the highest since at least 2018.

China’s developers are dealing with a series of government measures to cool the property market, under the slogan that homes are for living in rather than speculation.

Smaller cities, where the economy is weaker, were hit the most last month. Existing-home values slid 0.21% in 35 so-called tier-3 cities, the most since early 2015. Zhanjiang, which houses about 7 million residents in southern Guangdong province, saw values slump 1%.

Even in the four biggest cities including Shanghai and Shenzhen, existing-home prices declined across the board.

About three-quarters of cities saw second-hand home values fall from a month earlier. A price war is set to intensify in the coming months as landlords in wait-and-see mode surrender to the cooling trend, Yan said.

The downturn has continued into this month. Existing-home sales plunged 63% from a year earlier in the first 17 days of October, according to a Nomura Holdings Inc. note Monday.

“The effects of developers’ price discounts are waning,” Yang Kewei, a research director at China Real Estate Information Corp., said before the figures were released.

Fears of contagion from the crisis at Evergrande have intensified. Sinic Holdings Group Co. became the latest Chinese real estate firm to default as investors wait to see whether Evergrande will meet overdue interest payments on dollar bonds this week.

Yields on Chinese high-yield dollar bonds, which are dominated by builders, have climbed to their highest in about a decade, hurting a key funding channel for the sector.

That will have a knock-on effect on the broader economy, since Goldman Sachs Group Inc. estimates the property sector and related industries make up about 23% of gross domestic product.

Still, China’s central bank has said risks posed to the domestic economy by Evergrande can be contained. The property firm’s trouble “casts a little bit of concern,” People’s Bank of China Governor Yi Gang said at a virtual meeting of the Group of 30 on Sunday.

Comments - Please login in order to comment.