Photo: Karpowership

Photo: Karpowership The RMIPPP is the first step in the government’s plan to procure more than 13 800 megawatts (MW) of new energy over the next decade, as set out in the Integrated Resource Plan (IRP 2019) that was updated in October 2019.

Although we view the RMIPPP as positive in terms of the urgency needed to address the ongoing energy supply deficit, we are less positive about the extent of the gas-burning technology that will be used to generate this new energy, given its associated high level of CO2 emissions, which may detract from South Africa’s clean energy goals.

Two thirds of the energy procured will be from offshore “Powerships” which may not support the gross fixed-capital formation that our country desperately needs. The Powerships have also been granted exemptions from local content provisions during their project development phase, a key metric that bidders were required to comply with under the RMIPPP.

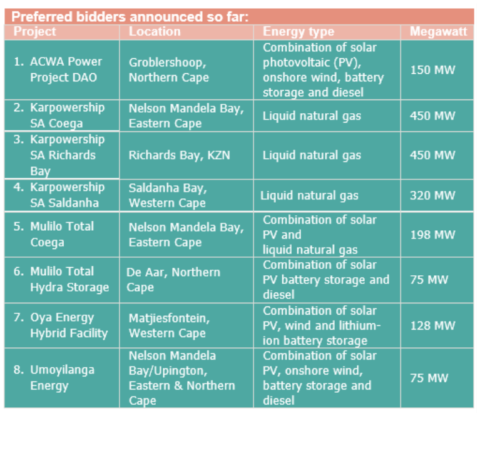

Eight projects with a combined generating capacity of 1 845 MW were selected out of twenty-eight bids totaling a potential contracted capacity of 5 117 MW. Three more projects with a combined capacity of 150 MW are being re-evaluated and could possibly be added to the list of preferred bidders in due course.

The projects under the RMIPPP are required to meet the following criteria:

- They must reach financial close by the end July 2021;

- Construction is to be completed within 12 to 18 months;

- Base load energy must be dispatched to the grid between the hours of 5am and 9.30pm; and

- At least 51% of the shareholding must be local and at least 41% held by Black South Africans.

Electricity generated by these projects will earn tariffs ranging from R1 468/MWh to R1 885/MWh (adjusted for inflation, fuel and the ZAR price of imported gas and diesel over the next twenty years) subject to the projected fuel price assumptions bid by the projects. This is more than double the preferred bid tariffs of approximately R700/MWh under the latest Round 4 of the Renewable Energy IPP Procurement Programme (REIPPPP) and is due to the higher cost of the dispatchable energy required by the RMIPPP, which will rely on technology utilising gas, battery storage and/or diesel in the projects. The preferred bids will benefit from the same government guarantee support regime as bid windows 1 to 4 of the REIPPPP, which has written concurrence by National Treasury.

The eight projects are forecast to create 3 829 job years for local citizens during construction and 13 549 job years for local citizens during the 20 years of their operations. Furthermore, the government envisages that there may be opportunity to capitalise on the new skills and supply lines to be established by the gas technology in the projects and used to develop the potential growth of the gas industry in South Africa. This could involve the repurposing of old Eskom coal-fired power stations to operate on gas, in the areas where there are plans to decommission these plants.

Aspects of the announcement are concerning

Despite the delay in implementing the RMIPPP (since the updated IRP 2019 was released almost eighteen months ago) it is a necessary and important step in the procurement of new energy, particularly to help alleviate the current supply shortfall. However, the dominance of gas in the technology mix of the preferred bidders has raised concerns, given the negative impact of burning gas on the environment and in light of the cheaper and cleaner renewable energy alternatives.

Given the size of the Powership projects, which each have individual generating capacity between two and six times bigger than the other preferred bids, many of the smaller projects were crowded out of the selection process. The market was generally expecting a larger number of preferred bids, comprising smaller capacity projects and a larger contribution of renewables to the mix of technologies.

There is some consternation about the cost of buying electricity from the Powerships for the next twenty years, when this technology is typically used by countries as a stop-gap short-term measure, and not as a long-term source of supply. Although the average bid tariff of R1 550/MWh for each of the Powerships is at the lower end of the price range for the RMIPPP preferred bids, it is not clear to us how the environmental costs of burning gas have been incorporated into the overall cost.

We understand that environmental approvals for the Powerships remain outstanding. In addition, it has been reported by Transnet that they have not received an application for their formal consent (which is required in terms of the National Ports Act) to park the Powerships in the harbour for a 20-year period. Given the very tight timelines to financial close, we are uncertain that the appropriate signoffs will be met by the stipulated financial close deadline of 31 July 2021.

We are also concerned about the risk of the preferred bidders of the onshore projects not meeting the financial close deadline, given the challenge of concluding multiple Engineering, Procurement and Construction (EPC) contracts covering the different technologies that will operate interactively. Historically, projects that utilise a single technology, such as the preferred bidders under the REIPPPP, would strain to achieve financial close within three or four months, and with far simpler contractual requirements and far less technological complexity.

Our key considerations and next steps

Futuregrowth is in the process of formulating its investment view on the projects that have won preferred bids. Specific areas of consideration include:

- The extent of carbon emissions that will arise from burning gas: The relative environmental impact profiles of the projects and their independent environmental assessment reports (including the impact of the Powerships on the surrounding marine life) will be carefully reviewed and we will need to be sure that the environmental costs have been appropriately included.

- Sole reliance on LNG by the Powerships: Energy generated by the Powerships will be totally dependent on imported gas and subject to the vagaries of international commodity prices and exchange rates. Most of the other preferred bidders are anticipated to utilise gas and/or diesel only to generate a variable degree of “top-up” to baseload power generation when necessary to address the intermittency and seasonal weather patterns of renewables.

- Job creation for South Africans: The Powerships will create a significantly lower number of jobs on average during construction (around 150 job years per project) compared to the average of each of the other preferred bidders (around 675 job years per project); however, will create a significantly higher number during the 20 years of operations (around 2 287 job years per Powership vs around 1 341 on average by each of the other projects).

- Ability to deliver the projects under a very demanding time frame: Most of the preferred bidders of the onshore projects will contract to build energy plants using hybrid forms of technology which require significant integration and operational co-ordination. Given the stringent deadlines for financial close and switching on their power to the grid, the construction risk must be mitigated by indisputable track records by the project parties and robust security enhancements for investors.

The Futuregrowth investment team is engaging its deal origination network on a number of RMIPPP debt syndication opportunities, with a view to concluding due diligence and reaching final investment decisions and implementation by the targeted end-July 2021 deadline for financial close of the projects.

On the face of it, and based on the information available, we believe the Powerships raise some critical questions which will require substantial explanations. Unless these concerns are addressed to our entire satisfaction, it will be very difficult to support investment in the Powership projects.

REIPPP Bid Window 5 – More renewables on the horizon

On 18 March 2021, Minister Gwede Mantashe also announced the next round of REIPPP (Bid Window 5) with the closing date for bid submissions on 4 August 2021. The market expects the preferred bidders for Bid Window 5 of the REIPPPP to be made known by the fourth quarter of 2021, and financial close by mid-2022. Futuregrowth will also consider investment in these projects.

Together with the onshore projects with a dominant renewable energy contribution that were awarded preferred bids under the RMIPPP, this introduces an exciting phase in the growth of South Africa’s energy sector and new investment opportunities for our clients. BM/DM

This article was written by Paul Semple, Portfolio Manager at Futuregrowth

Futuregrowth Asset Management (Pty) Ltd is a licensed Financial Services Provider.