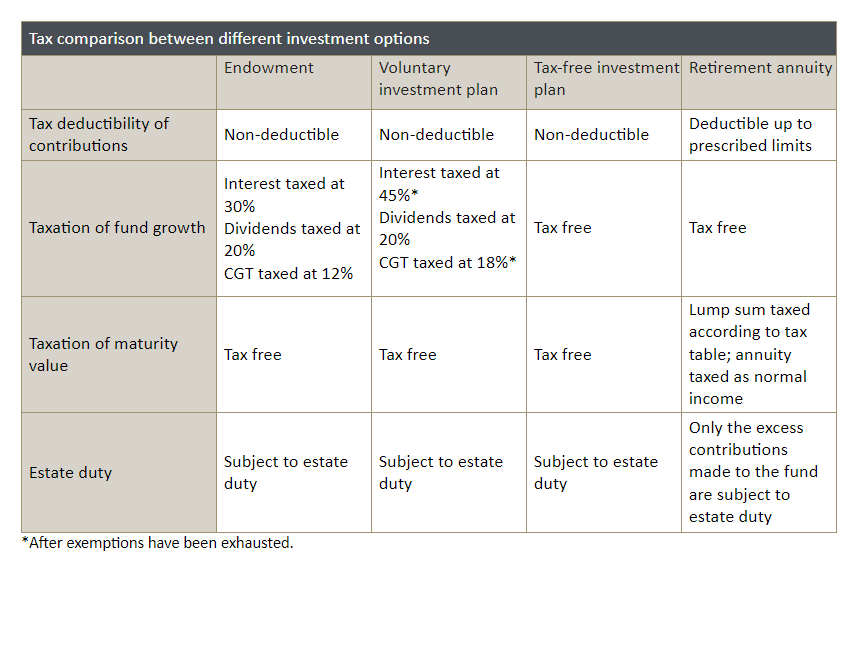

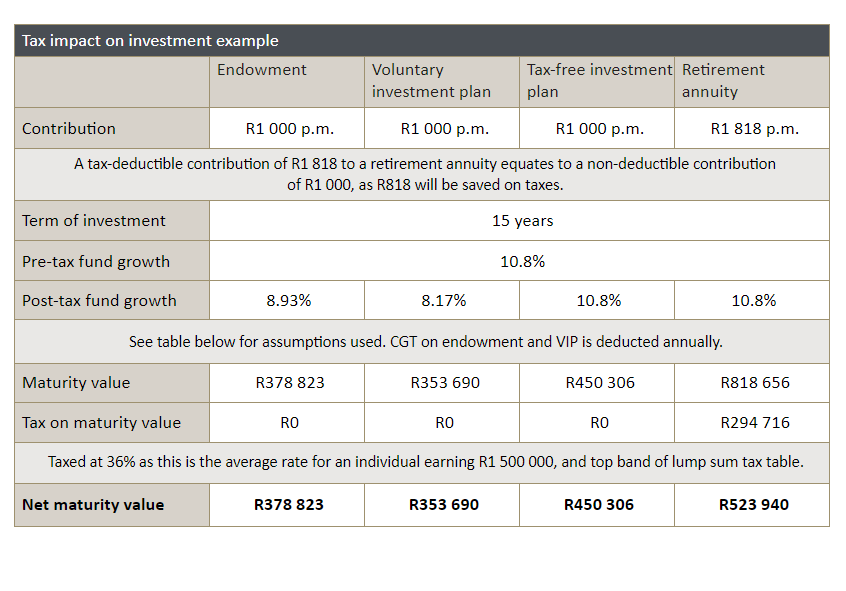

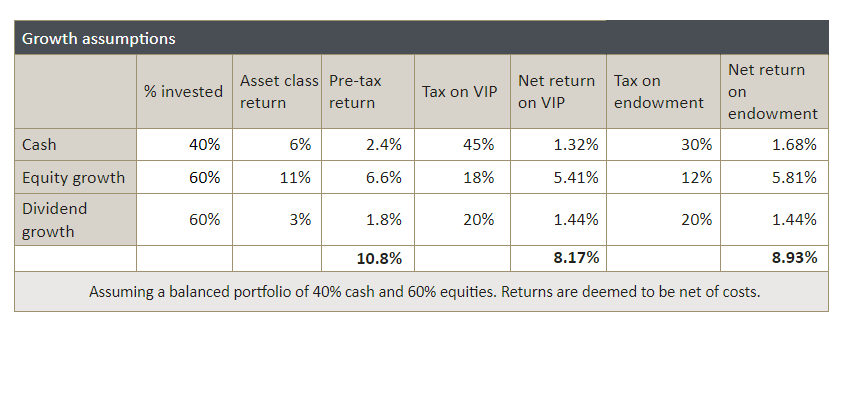

Understanding the tax benefit

However, this argument ignores the fact that the tax rates of retirees are normally significantly lower than prior to retirement when they received the tax benefits from contributions. It also ignores the benefit of tax-free growth within the portfolio as well as benefits in estate duty. The table below compares an endowment, a voluntary investment plan, a tax-free investment plan and a retirement annuity.

Understanding Regulation 28

Regulation 28 is aimed at preventing fund members or trustees from selecting highly concentrated portfolios and running the risk of losing everything. However, the most negative publicity retirement funds receive is probably because of Regulation 28 and the limitations it imposes – such as the 75% limitation on equity and 30% on offshore investments. It is argued that a retirement fund is a long-term investment and there should therefore be no limitation to investing in equities, which have historically provided the highest returns over the long term. The same argument is made about the limitation on offshore assets. Research, however, shows that only a small percentage of investors invest close to the limitations that apply in terms of Regulation 28. In addition, it is possible to build a diversified aggressive portfolio within the confines of Regulation 28. Even where an investor believes a Regulation 28 portfolio is not the optimal choice for them, the potential return foregone by choosing a ‘more conservative’ portfolio is outweighed by the benefit of the tax savings realised (on contributions and returns).

Base decisions on facts, not fears

The issue of retirement funding is one that elicits many emotions from the public, but these are often not founded on facts, but rather on fears. While there are reasons for concern, these are often not as dire or cataclysmic as imagined. Retirement funds offer their investors a multitude of benefits, and these are best considered holistically when making an investment decision. DM/BM