The sun sets beyond an offshore oil platform in the Persian Gulf's Salman Oil Field, operated by the National Iranian Offshore Oil Co., near Lavan island, Iran, on Thursday, Jan. 5. 2017. Nov. 5 is the day when sweeping U.S. sanctions on Irans energy and banking sectors go back into effect after Trumps decision in May to walk away from the six-nation deal with Iran that suspended them. Photographer: Ali Mohammadi/Bloomberg

The sun sets beyond an offshore oil platform in the Persian Gulf's Salman Oil Field, operated by the National Iranian Offshore Oil Co., near Lavan island, Iran, on Thursday, Jan. 5. 2017. Nov. 5 is the day when sweeping U.S. sanctions on Irans energy and banking sectors go back into effect after Trumps decision in May to walk away from the six-nation deal with Iran that suspended them. Photographer: Ali Mohammadi/Bloomberg “The growth-into-value rotation may be reinforced after the results of the Georgia Senate election amid the prospect of a higher fiscal stimulus bill and steeper yield curve, which would benefit banks and other non-tech companies,” David Bahnsen, chief investment officer of the Bahnsen Group in Newport Beach, California, wrote in a note to clients.

Congress passed at year’s end a $900 billion spending deal to bolster an economy showing signs of slowing as the raging virus prompts stricter lockdowns across the country. The number of employees at U.S. businesses unexpectedly declined in December for the first time since April, underscoring the ongoing labor-market fallout from the pandemic. The figures preceded the monthly jobs report on Friday, which is projected to show weaker payroll growth.

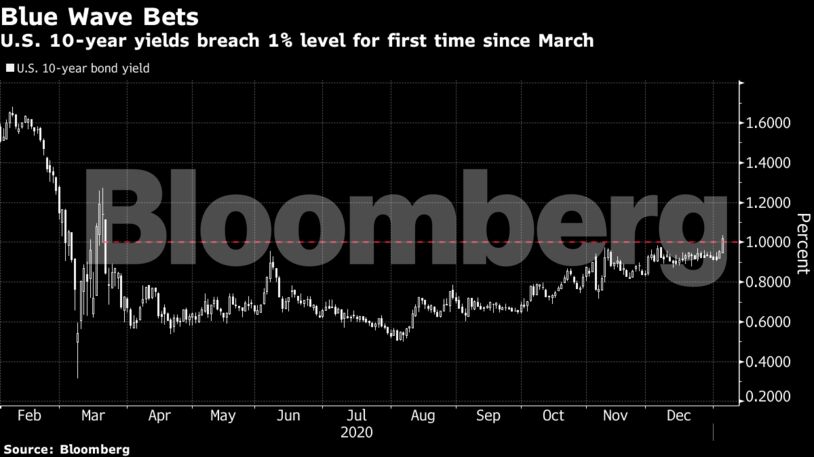

Read: Treasuries Breaching 1% on Democratic Win May Just Be the Start

Federal Reserve officials unanimously backed holding the pace of bond buying steady when they met last month. “All participants judged that it would be appropriate to continue those purchases at least at the current pace, and nearly all favored maintaining the current composition of purchases,” according to minutes of their Dec. 15-16 meeting published Wednesday.

U.S. 10-year breakevens -- a market gauge of inflation expectations over the next decade -- topped 2% this week for the first time since 2018, having gained in each of the last three months. While the pandemic is still raging with the rollout of vaccines in the early stages, the risk is that further signs of inflationary pressure could start prompting bets on Fed rate hikes.

For Matt Miskin, co-chief investment strategist at John Hancock Investment Management, the ball will be in the Fed’s court next and how policy makers will react to this evolving political backdrop.

“They have been wanting more fiscal support, well now they have it, and it is coming with a cost -- higher interest rates based on Treasury yields rising,” Miskin noted. “We will see what the Fed’s pain threshold is for higher Treasury yields in the first half of 2021. The tug-of-war between monetary and fiscal policy will be key to markets. While the fiscal side is looking more promising based on the results today, monetary policy may take a step back.”

Elsewhere, Bitcoin jumped to another all-time high as extreme swings continued to buffet the world’s largest cryptocurrency. And the New York Stock Exchange is proceeding with a plan to delist three major Chinese telecommunications firms, its second about-face this week, after U.S. Treasury Secretary Steven Mnuchin criticized its shock decision to give the companies a reprieve.

These are some of the main moves in markets:

Stocks

- The S&P 500 gained 0.7% as of 3:11 p.m. New York time.

- The Stoxx Europe 600 Index climbed 1.4%.

- The MSCI Asia Pacific Index fell 0.2%.

Currencies

- The Bloomberg Dollar Spot Index fell 0.1%.

- The euro was little changed at $1.2304.

- The Japanese yen weakened 0.4% to 103.17 per dollar.

Bonds

- The yield on 10-year Treasuries jumped nine basis points to 1.04%.

- Germany’s 10-year yield climbed six basis points to -0.52%.

- Britain’s 10-year yield rose three basis points to 0.243%.

Commodities

- West Texas Intermediate crude advanced 1.8% to $50.81 a barrel.

- Gold lost 2.2% to $1,906.91 an ounce.