The International Monetary Fund headquarters in Washington DC. (Photo: Andrew Harrer / Bloomberg via Getty Images)

The International Monetary Fund headquarters in Washington DC. (Photo: Andrew Harrer / Bloomberg via Getty Images) The weight of economic opinion has swung towards a K-shaped economic recovery that is characterised by increasing divergence between the performance of different countries and industries.

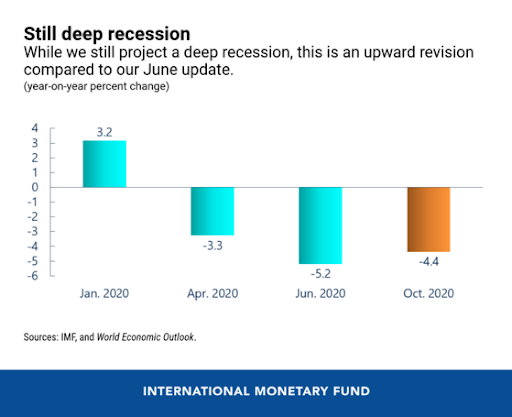

In its October World Economic Outlook, the International Monetary Fund (IMF) describes the global recovery as a long, uneven and uncertain ascent, predicting a -4.4% growth rate this year – a slight improvement on June’s forecast – and a 5.2% rebound next year.

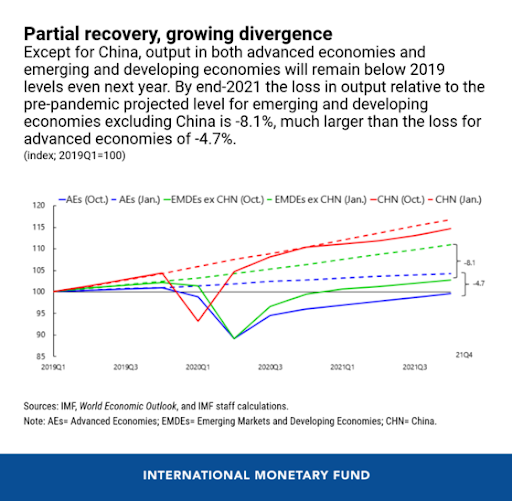

But that overall figure disguises the vast difference between different country growth rates, with Spain expected to deliver the worst economic performance this year, with negative growth of 10.8% and China the only country to deliver positive growth, of 1.9%. Gita Gopinath, IMF chief economist and director of the research department, says: “The divergence in income prospects between advanced economies and emerging and developing economies (excluding China) triggered by this pandemic is projected to worsen.”

At another virtual conference held this week, by the Institute of International Finance, economists were largely of the same opinion: that the recovery will be uneven and the gap between countries and industries will widen.

On a panel titled “Can we recover from Covid?”, Alexandra Dimitrijevic, MD and global head of research at S&P Global Ratings, agreed that the recovery is uneven and that the gap is widening at both a country and industry level.

“The early exiters who have managed to contain the first wave are well advanced in their recovery, with China the only country likely to end the year in positive territory.” In contrast, she expects a number of emerging economies, sadly, including South Africa, as well as India and Mexico, to incur “significant permanent losses” as a result of the crisis. The IMF expects South Africa to experience an 8% decline in GDP this year followed by 3% growth next year.

Dimitrijevic believes the world is going to experience a K-shaped recovery as a result of the divergence in performance underway. “After the sharp mechanical rebound the next leg of the recovery is going to be long and difficult,” she adds. She notes that the US has recovered half of the jobs it lost as a result of the pandemic but that it is likely to take at least until 2023 to recover the other half.

OCBC Bank chief economist Selena Ling also expects a K-shaped recovery, with manufacturers, pharmaceutical and financial companies doing well, and the aviation, hospitality and entertainment industries struggling to recover.

Amundi’s deputy chief investment officer, Vincent Mortier, had a different view, expecting a W-shaped recovery, with economic activity coming back and then retreating before recovering again. He says some sectors are experiencing L-shaped recoveries, while others have U-shaped rebounds. He says China is back on track to achieve pre-Covid levels of economic growth in 2021, but that other countries will take longer and are only likely to get there in 2022. Dimitrijevic believes it may take longer, while the IMF agrees China will recoup its lost ground by 2021. On the other countries, Gopinath says: “Output in both advanced economies and emerging market and developing economies is projected to remain below 2019 levels even next year.”

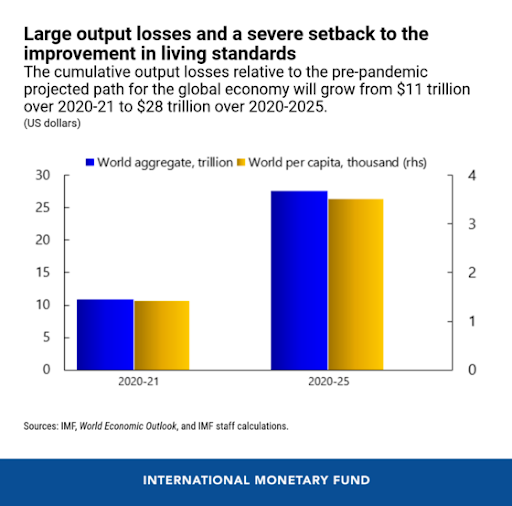

Gopinath says the crisis is likely to leave scars well into the medium term, “as labour markets take time to heal, investment is held back by uncertainty and balance sheet problems, and lost schooling impairs human capital”. Financially, the IMF estimates this could amount to a cumulative loss in output of $28-trillion between 2020 and 2025, (see graph below), which, she says, will have a severe impact on average living standards globally.

Mortier has various concerns about the road ahead. These include unemployment exacerbating inequalities, zombie companies undermining the health of the corporate sector and the sustainability of debt incurred during this crisis. He says: “Jobs won’t come back in the same shape or form as before Covid.”

Mortier notes that a crisis usually stems from debt and adds that he is doubtful about the sustainability of current debt levels and governments’ ability to absorb the massive levels of debt racked up during the pandemic.

Dimitrijevic estimates that global debt to GDP will increase by 60 percentage points in 2020 and level off thereafter. Any improvement in the ratio will be as a result of GDP coming back rather than debt declining, she adds.

Mortier also says markets have become totally addicted to monetary policy and fiscal policy, to the point where, he says, “it is not very healthy and has led to inflation of asset prices for sure”. He adds that the outcome of the stimulus programmes and central bank interventions in the financial markets is that we don’t have a free market any more because it is “totally under control”. He warns that this could lead to complacency.

All economists concurred that it would be ill-advised to withdraw stimulus support prematurely – a view shared by the IMF. Dimitrijevic says it is critical that we avoid the risk of premature austerity, saying that stimulus programmes have been necessary to avoid more substantial economic costs and that these will be sustainable as long as the baseline is a shock that is deep, but temporary.

The IMF stresses that more action is needed. Dimitrijevic says: “Policies must aggressively focus on limiting persistent economic damage from this crisis.” These should include income support through well-targeted cash transfers, wage subsidies, unemployment insurance tax deferrals, moratoria on debt services and equity-like injections into viable firms.

As the recovery strengthens, says Gopinath, policies should shift to supporting sustainable reallocation of works to growing sectors and public green infrastructure investments.

There is no doubt that there is a long road ahead, littered with uncertainty, because these predictions come with significant health warnings about the many downside risks that could materially change the global growth picture of the coming years. DM/BM