The increase in debut bond sales will help add depth to the debt market, providing more choices for investors while also giving rise to the risk of buying notes of borrowers that lack a track record. For the issuers, debt deals are an opportunity to build cash buffers in a slumping economy. India’s bond sale boom is in line with a jump in debt offering across Asia as policy makers flood markets with cash to fight the coronavirus pandemic.

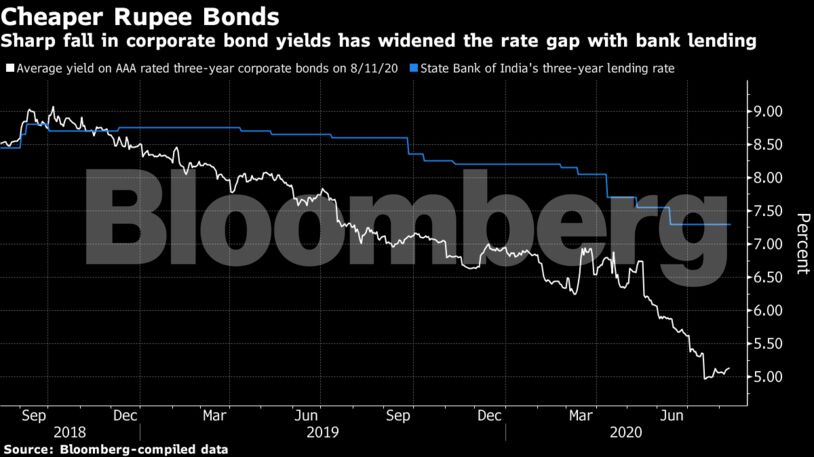

It typically costs less to sell a bond than to get a loan in India, because banks are curbing lending to battle the world’s worst debt ratio. The average yield on top-rated three-year notes at 5.09% is 221 basis points cheaper than loans of similar tenor at the country’s largest lender State Bank of India.

Borrowing costs on bonds have plunged after Indian policy makers unveiled record stimulus to help combat the financial fallout of the pandemic. Steps included slashing interest rates to the lowest level since at least 2000, funding banks’ purchase of 1.13 trillion rupees ($15 billion) of company notes and deferrals on loan repayments for individuals and businesses.

Some investors worry that the Covid-19 relief measures are masking the true picture of businesses’ credit health. But bond yield premiums suggest the market welcomed the moves.

See also: Record Stimulus Slows Credit Downgrades of Indian Companies

The spread between top-rated three-year corporate notes and similar tenor government debt fell to 22.4 basis points last month, the lowest level since October 2005. The gap stood at 23 basis points on Friday.

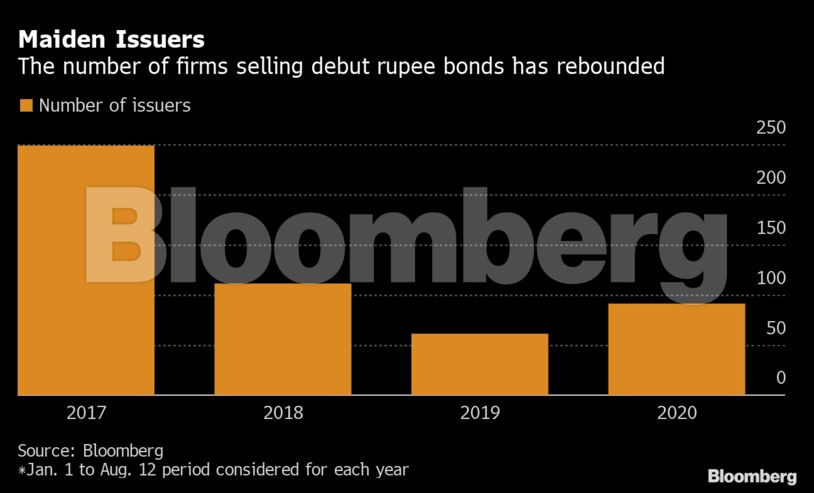

Other notable firms are tapping the debt market for the first time. Godrej Industries Ltd., part of a 123-year-old conglomerate, raised 7.5 billion rupees in July, while Rashtriya Chemicals & Fertilizers Ltd., a state-owned firm, this month raised 5 billion rupees.