(Photo: Adobe stock)

(Photo: Adobe stock) This is the second draft following on the first draft last year by FSCA on the Standard on Investment Linked Living Annuities (living annuities). The new Standard sets out FSCA responses in response to queries by interested parties. The latest set must be responded to by interested parties by July 31 2020.

In my view, the FSCA draft Standard on Living Annuities should be used by retirement funds as a default, and as a guide by anyone using a living annuity bought directly from a linked-investment service provider or life assurance company.

One most important change you should adhere to is on the drawdown rate of income from a living annuity. Stick to this and you will have a much better chance of financial survival. Research by the country’s biggest retirement fund administrator, Alexander Forbes, has shown that by using higher drawdown rates than those suggested by FSCA, you will reach a “point of ruin” when your income declines in both nominal and after-inflation returns.

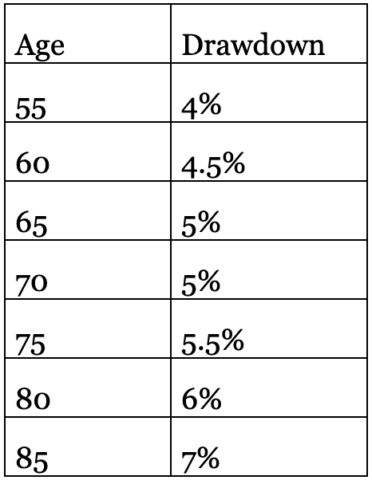

FSCA has now set down two drawdown rates. The first is the maximum drawdown rate at which retirement funds should aspire to when setting the rates. By using this drawdown rate scale, FSCA says retirees should be able to achieve a 90% probability of financial survival. This is based on average life expectancy and a balanced investment portfolio.

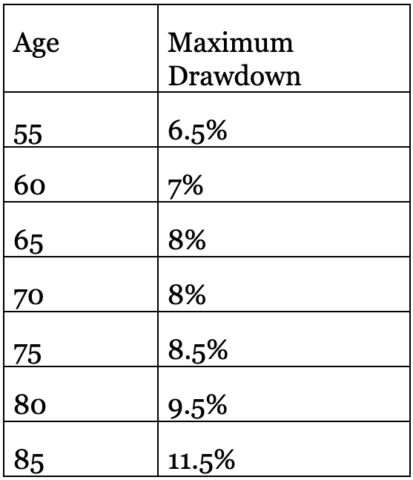

The new FSCA draft table also sets down a maximum allowable drawdown rate.

FSCA says retirement funds must encourage members who choose the default annuity to:

- Use the lower drawdown rate;

- Choose an underlying portfolio that is conservative; and annuity rates should be based on a couple, rather than an individual.

FSCA says that where a pensioner elects a living annuity on retirement, there is a risk that this could result in poor retirement outcomes for the pensioner, such as unsustainable income streams with a reduction in affordable annuity payments over time. The poor outcome could be caused by one or more of the following:

- The living annuity retirement savings being depleted too soon if the draw-down rate elected is too high. You meet an early “point of ruin”;

- Poor investment returns on capital;

- The pensioner living longer than expected, exceeding the average age of death. So, this means you could well have a 50% chance of living longer. You should always get a quote on the average rate of death at your retirement date and for your gender; and

- Excessive fees or charges.

A retirement fund may only include a living annuity as a default option in its annuity strategy if:

- More protection is provided to members choosing a living annuity, compared to the cases where a member makes a specific choice to buy a living annuity from a linked-investment service provider (lisp) or life assurer based on their own circumstances and research.

- It measures the outcomes of the living annuity, which must be monitored and clearly communicated to pensioners at the inception, and, then on a regular basis.

- The information, in terms of the draft Standards, should be at least once a year and should include information on its sustainability, including warnings where a pensioner is unlikely to achieve increased income targets, or income in the long term. The pensioner must be encouraged to take alternative actions.

- The pensioners must be informed when their living annuity is no longer sustainable, even if all the recommendations made in the draft Standard are met.

There is however one big and significant step that living annuity pensioners can take. That is to take out what is called a hybrid annuity, which allows one of the underlying investments to be in a traditional guaranteed annuity.

This is not required by the draft Standards, but in terms of the Standards, you can buy a hybrid annuity.

This is something that retirement funds, which offer default annuities, should offer to their retirees. It makes a lot of sense.

In terms of FSCA draft Standard on Communication of Benefit Projections, your retirement fund must keep records on all its communications with you on any default annuity, living or guaranteed annuity.

This particularly with regard to required retirement benefit counselling. The counselling includes:

- The choices of annuities (pensions) must be explained to you before retirement and must be done whether the fund offers you a default annuity or not. For example, Provident Funds are exempted from providing a default annuity. Remember, to take out a default annuity you must request it – it is what is called a soft default option.

- The language used to provide you with information must be clear and easy to understand, avoids uncertainty or confusion and is adequate and appropriate in all circumstances.

- In terms of existing regulations you must receive retirement benefit counselling from your fund: from before you retire about the fund’s investments; the default annuity; and what happens if you exit from a fund before retirement (this assists you to preserve, or transfer your savings to a new fund and your choices at retirement).

The retirement benefit counselling should take place:

- No more than three months before retirement;

- The FSCA recommends, but does not stipulate, that counselling also take place at five years, one year and three months before retirement.

Retirement benefit counsellors cannot offer financial advice. They will provide you with general guidelines. Retirement benefit counselling is free.

In terms of the draft Standard on Communication, you will also be given a much better understanding of your prospects for retirement before you retire. This will include:

- How your contribution, after the deduction of the costs and insurance benefits and investment returns, will contribute to your pensionable income at retirement.

- Whether, when you are still saving, the projected amount would fund sufficient income in retirement, based on your income at retirement and on certain assumptions that must be detailed by your fund. There are limitations on the assumptions, for example, returns must not be projected at more than inflation plus 4%.

- In the assumptions, the fund must indicate to you the replacement ratio you can expect at retirement. A replacement ratio is the percentage of your final total salary you will receive from your pension. Prior to the publication of this draft Standard, most replacement ratios were only given against basic salary, excluding allowances, bonuses and commissions – not total salary. BM/DM

This is the final in a series of reports written by Bruce Cameron, the semi-retired founding editor of Personal Finance of Independent Newspapers, that cover the effects of Covid-19 on pensioners, including research undertaken by Alexander Forbes on retirement income in South Africa. Bruce Cameron is co-author of the best-selling book, The Ultimate Guide to Retirement in South Africa.

Comments

Scroll down to load comments...