Time will tell whether the turnaround in sentiment persists alongside the gradual opening of economies during May. However, European stocks tumbled about 3.5% on Monday, and South African counters lost about 2.5%. (Image: Rawpixel)

Time will tell whether the turnaround in sentiment persists alongside the gradual opening of economies during May. However, European stocks tumbled about 3.5% on Monday, and South African counters lost about 2.5%. (Image: Rawpixel) As stock markets rallied sharply during April, they diverged further and further from the economic realities facing countries around the world.

By the end of the month, the optimistic tone of equity investors was in complete contrast with growth and business activity statistics that confirmed even the most pessimistic views of how deep and painful the shutdowns could prove to be.

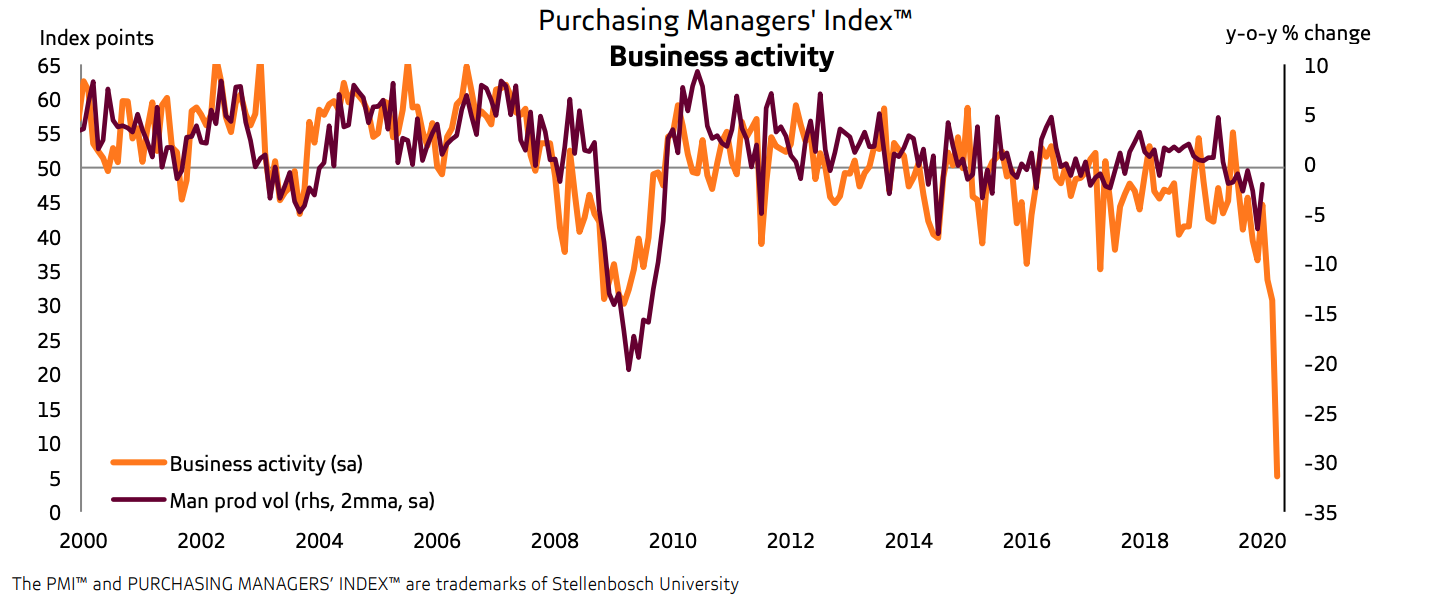

South Africa got its first bitter taste of the economic ramifications of the full lockdown yesterday when the Absa Purchasing Manager’s Index was released yesterday. The Business Activity Index fell a staggering 83.4% month-on-month and more than 30% year-on-year to 5.1 in April, confirming a complete economic meltdown.

Offshore, first-quarter GDP decreases ranged from the US GDP contraction of 4.8%, Europe’s negative 3.8% and Hong Kong’s 8.9% decline. In Europe, European Central Bank President Christine Lagarde went on the record saying that the region could see GDP growth decline by as much as 15% this year.

These are first-quarter figures and thus don’t include the effect of the shutdowns. Goldman Sachs gives some indication of what could be expected in April. Its current activity indicator came in at -4.8% at the end of April versus -2.2% at the end of March. China bounced back from -14% in February at the peak of its shutdown to -1.6% in April.

Investec Wealth and Investments points out that the Goldman Sachs measure for the US is currently tracking at -10.3% (-7.2% in March), while Europe is running at -7.8% (-5.4% in March).

“In effect, it appears that China is heading back to close to normal, while the US and EU are still finding the bottom of their “U”.

Consensus estimates for developed market growth in 2020 are now at -4%, and downgrades in the consensus estimates of emerging market growth continue, with 1% now expected.

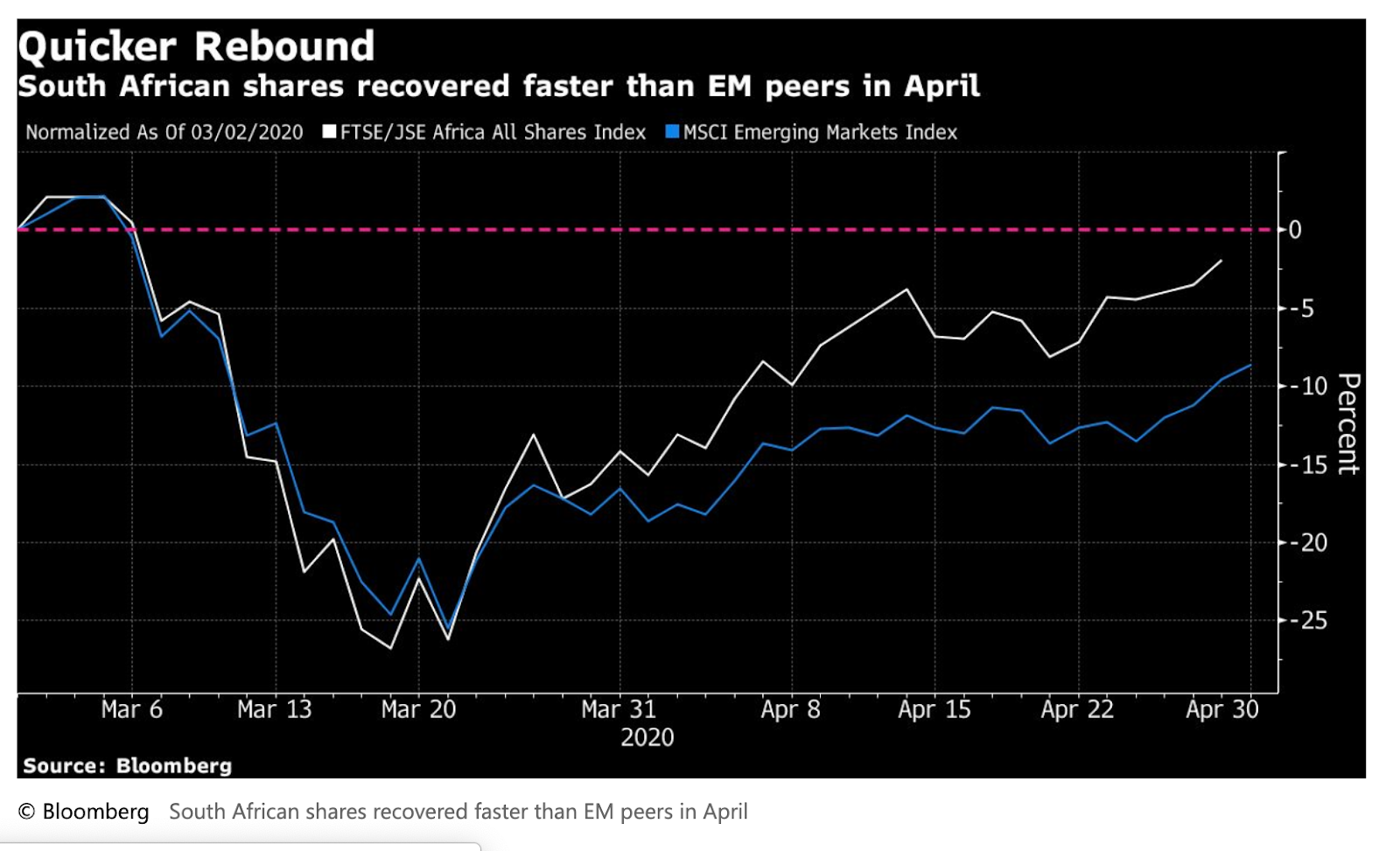

The economic evidence and growing likelihood of a U-shaped recovery at best are in stark contrast to stock market valuations that were pricing in a V-shaped recovery until the end of April. Stock markets had their V-shaped recovery in April, with the S&P 500 and JSE All Share Index regaining most of their lost ground lost during the sharpest and quickest sell-off in history into bear-market territory in late February.

A month later, the US Federal Reserve’s announcement that it would make unlimited purchases of financial assets prompted the sharp turnaround and subsequent steep rally. The S&P 500 gained more than 30%, leaving it just 15% off the all-time February high before the extent of the coronavirus pandemic became clear.

The JSE All Share Index experienced a similarly V-shaped ride, declining 35% before rallying more than 30%. The Index ended the month about 12% lower than it started the year. Most surprising is that despite all the bad news that has rocked South Africa this year, including three rating downgrades and a worrying fiscal outlook, the local stock market outperformed its emerging market counterparts by more than 5% in April, gaining 13% for the month.

The bond market has also held up surprisingly well in the wake of the sovereign downgrades. Investors were waiting to see the full impact of the country’s across-the-board junk status last week when South Africa was due to be removed from the FTSE World Government Bond Index (WGBI) at the end of April. However, so far it seems to have been a non-event, with the bond market beginning this week on a positive note, with foreign flows seemingly unaffected.

May hasn’t started on the same positive note for global stock markets. Equity market investor sentiment took a turn for the worse, prompting investors to take risk off the table as they recalibrated their views to factor in the likelihood of disappointing earnings growth this year and the possibility of a U- rather than V-shaped recovery at best.

This brought up the old financial market adage: sell in May and go away. Time will tell whether this turnaround in sentiment persists alongside the gradual opening of economies during May. However, European stocks tumbled about 3.5% on Monday, and South African counters lost about 2.5%.

A key concern is whether the global economy will return to its pre-crisis level within a two-year time horizon. Although it feels like a world away, it’s worth remembering just how reliant the US had become on the consumer to hold up its growth rate before the coronavirus hit and how important a role the consumer will still have to play in the economic recovery.

Another critical determinant of whether the economy will achieve its former level of economic activity is whether the trade agreement between the US and China holds firm and trade relations do not deteriorate. China’s ability to buy $200bn worth of US goods will be a considerable stretch. But even more worrying is the tough stance US President Donald Trump is taking as he ramps up his efforts to prove that China withheld information about the extent of the danger posed by the coronavirus. This week Trump said he would consider using trade tariffs as the ultimate punishment.

The prospect of the economic shock becoming as deep as the Great Depression has been an ongoing point of debate and, if the world goes down this path, aligns with a worst-case scenario of an L-shaped recovery.

Investec UK Equity spokesperson Roger Lee contemplated this in his analysis on the differences between the Great Depression and the economic shock caused by Covid-19. He says a significant rebound is likely during the second half of 2020, but that it may not be sufficient to overturn the decline inflicted by the virus.

The crucial difference between the Great Depression and now, however, is the current downturn will be temporary rather than as prolonged as the Great Depression.

“At worst it will be months, but hopefully, it’ll be weeks before the lockdown ends and economies can re-start. Even if it takes longer to overturn all the declines from the Covid-19 crisis, it is hard to imagine anything like the years of grinding economic decline and resultant personal destitution of The Great Depression.”

To get a sense of the implications of the different recovery paths on the stock markets, Fidelity’s director of global macro in its global asset allocation division, Jurrien Timmer, has spelt out different recovery scenarios and their possible impact on the S&P500’s valuations this year.

He sees the elevated levels of the stock market at the end of April as “nothing more than a QE-induced bear market rally”. Timmer points out that after discounting a depression-scenario a month ago, the stock market had begun to discount a severe but short-lived recession followed by a recovery.

Timmer compared different recession and recovery scenarios based on a discounted cash flow model. The best-case scenario is the V-shaped recovery that would justify the current stock market valuations, while the worst case is the L-shaped recovery. Another is a swoosh recovery, which he considers most plausible.

He argues that the V-shaped recovery seems too optimistic given the likelihood that the economy will reopen only gradually and with bumps along the way. However, if it does, he notes that this scenario implies that the US stock market will return to its February highs “in relatively short order”.

As for the L-shaped recovery, he says this assumes some impairment to the corporate sector and implies a further 37% decline in the S&P 500 from current levels. But this alternative is unlikely, given the robust and timely policy response by the government and the central bank, Timmer says.

A swoosh outcome, which would play out as a sharp fall in the economy followed by a gradual recovery, would imply minimal upside for the S&P 500 from here, he says, “but also not a ton of downside.”

While the extent of the declines in the JSE All Share Index may differ, his scenarios do give an indication of what we could expect from the local stock market in the event of any of these scenarios playing out – and the potentially wide range of outcomes that lie ahead. BM