In the case of Covid-19, no country is safe until every country is safe – a fact of our deeply interconnected and interdependent realities, say the writers. (Image: wikimedia / numista.com)

In the case of Covid-19, no country is safe until every country is safe – a fact of our deeply interconnected and interdependent realities, say the writers. (Image: wikimedia / numista.com) To date (26 March 2020), the total number of confirmed infections has reached over 416,686 in 197 countries with 18,589 deaths. In a matter of two months, Covid-19 has reshaped our ideas about being socially connected, economically entangled and existentially unprepared for radical change.

Quarantine and social distancing measures, travel bans and restrictions, closed regional and national borders, and health communications have been ratcheted up globally to reduce the chance of exposure as Covid-19 infections and fatalities continue to rise.

As China has demonstrated, only stringent aversion behaviour is able to control Covid-19’s spread. The World Health Organisation (WHO) has criticised some governments’ slow early response, especially those of advanced economies. They accuse these countries, especially in Europe and North America, of not understanding the science and the pattern of Covid-19, calling their early efforts at managing a public health emergency “too little, too late”(Oqubay, 2020).

Europe has now become the new epicentre of the virus after China’s measures to contain and control its spread show promising signs. Since March 2020, new cases of Covid-19 in China have dwindled to less than 1% (Oqubay, 2020).

Covid-19 in Africa

The WHO says just over 2,455 positive cases of Covid-19 have been recorded in Africa (WHO, 26 March 2020). Twelve countries in Africa are now experiencing local transmission and with vastly different population demographics, the shape and impact of Covid-19 in Africa could look very different from Europe, Asia and North America.

Testing kits and medical supplies have been shipped to several countries on the continent, enabling 45 African nations to now test for the virus, as opposed to just two at the start of the outbreak in January 2020. WHO has also been supporting government health ministries across Africa, training 36 Rapid Response Teams. The training aims to improve their surveillance and contact tracing abilities along with data collection, reporting and diagnosis (Wang, 2020).

Africa’s health vulnerabilities

Covid-19 is said to affect the elderly more, but this is cold comfort for Africa, which is a world region that has the youngest population compared to other world regions. Vulnerability to Covid-19 in Africa is more related to underlying health conditions, of which Africans have a disproportionate share.

The WHO estimates there are 26-million people who are HIV positive in the region, a condition that compromises the body’s immunity. Over 58-million children in Africa are malnourished and suffer from stunting, making it entirely plausible that younger people in Africa could be much more susceptible to Covid-19 than other world regions.

Health systems in Africa are also already stretched in dealing with ongoing disease burdens like malaria and Ebola. Effects of the Ebola outbreak in 2014-16 in West Africa resulted in fewer resources dedicated to endemic conditions as well as fewer people seeking treatment for maternal health, hypertension and diabetes (Wang, 2020). Health authorities fear the same trend with regional Covid-19 outbreaks.

Global economic fallout from Covid-19

Initially, global leaders imagined a sharp, but short hit to the world economy, presuming the Wuhan-originating outbreak would largely be a localised problem for China with some knock-on effects.

Now, towards the end of March 2020, a V-shaped recession in the first half of the year, followed by a recovery in the next half looks unlikely (Elliot, 2020). The Organisation for Economic Cooperation and Development (OECD) has warned that the virus poses the biggest danger to the world economy since the 2008 financial crisis.

Measures to contain the virus, including national lockdowns, social distancing, factory closures and travel restrictions have crippled supply chains, reduced output, hit commodities and sent confidence on a downward spiral. Covid-19 is a health emergency that is fast becoming an economic crisis, with both a supply- and demand-side shock.

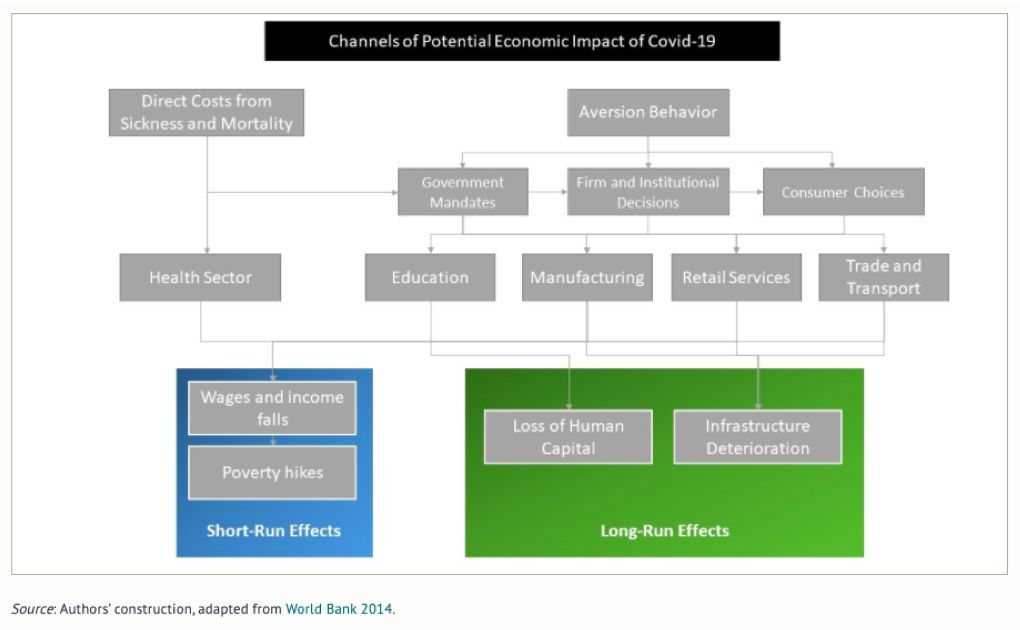

There are both long- and short-term effects on the pandemic as the diagram below shows. “Aversion behaviour” is understood to be all the actions taken to avoid infection, be they on a global, national or personal scale. It is the most likely category of actions that will lead to longer-term economic consequence, stemming from state restrictions on social and business activities, leading to business and school closures, resulting in lost payment for workers, which eventually translates into less spending and social activity (Evans and Over, 2020).

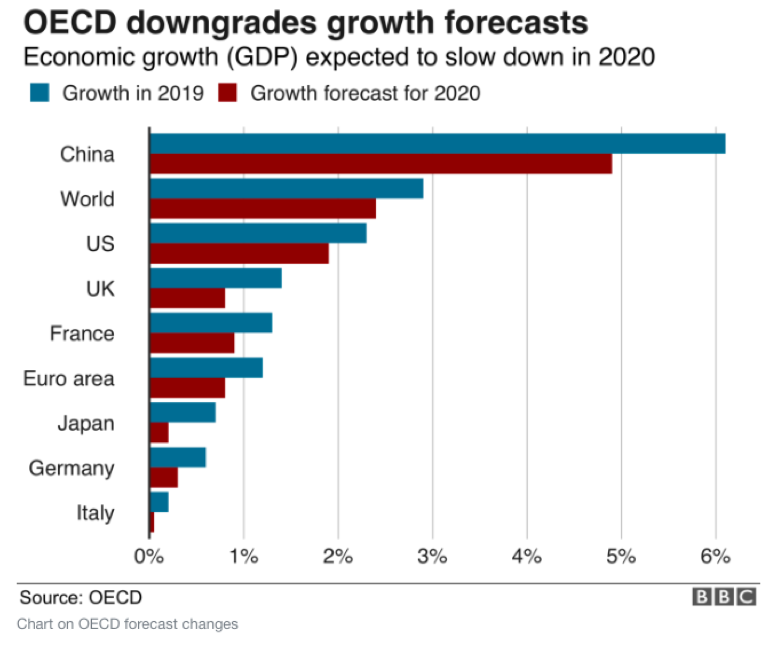

Economists and analysts calculate that the long-run effects will lead to reduced global growth. In the figure below, the Organisation for Economic Cooperation and Development (OECD), has revised down growth forecasts to hover around 2% to 1.5%, which is half the projected rate before the Covid-19 pandemic (OECD, 2020). This low growth would erase $1-trillion off the value of the world economy (Hutt, 2020).

Volatile world markets have compounded aversion behaviours since the coronavirus outbreak in Wuhan, China in December 2019. It has caused oil and stock prices to tumble with a few historic levels recorded in March 2020.

Oil

China is the world’s biggest oil importer and with much of the country still in lockdown, combined with several other countries just enforcing lockdown and states of emergency to contain Covid-19, the International Energy Agency (IEA) has predicted the first drop in global oil demand in a decade (Hutt, 2020).

The IEA’s monthly report for March 2020 puts the year-on-year slump at 90kb/d. The current price of oil, as of 23 March 2020 at $22.43 a barrel is close to record lows during the Asian Financial crisis in 1998/9 (World Oil, 2020).

Analysts have predicted that the price war between Russia and Saudi Arabia has been catastrophic for OPEC, the world’s most successful cartel. In March 2020, the Saudis abandoned their 2017 output agreement, flooding the market with cheap crude oil. The move was in response to Russia’s refusal to effect deeper production cuts to help prop up prices in the face of declining demand due to Covid-19 (Fortune, 2020).

Oil price volatility has deep impacts for African oil-producing and exporting countries like Libya, Algeria, Nigeria, Angola and Ghana. The oil price drop in 2014 impacted significantly on the continent, which saw a decline in GDP growth for the sub-Saharan region from 5.1% in 2014, to 1.4% in 2016 (Brookings, 2020). Compared to 2014, the oil price fallout during the Covid-19 pandemic has plummeted over a shorter time, declining 54% in just three months.

African oil-producing countries rely heavily on oil earnings to fund national budgets. They have pegged national earnings on a much higher oil price of around $60 per barrel (Bloomberg, 2020).

Ghana’s hopes of earning at least $1.5-billion off new oil discoveries this year have been dashed not to mention Nigeria’s and Angola’s projections, the continent’s first, and second-biggest producers and exporters respectively. China is Angola’s largest oil importer and with demand low, Angola’s economic resilience to weather a global economic recession is poor, this at a time when it is experiencing its fourth year of recession (SET, 2020).

Fragile and volatile markets look to be the order of the day, with key indices decidedly down on 23 March 2020. Uncertainty around when the pandemic disruptions would cease has prompted investors to sell even good stocks with fundamental value (Bloomberg, 2020). The big winners are those who anticipated the crash and bid short.

The Africa/China connection

Since 2009, China overtook the US as Africa’s biggest trading partner. Now, during this time of virus-induced panic, analysts are looking to China first for indicators of knock-on economic impact. China’s cities are still in lockdown, its production sectors have slowed dramatically, travel internally and to the rest of the world has all but ground to a halt, and commodity prices have plunged.

A slowed-down super-power means that low- and middle-income countries dependent on trade and tourism with China will feel the sting of the virus, even if Covid-19 infections in those countries don’t spike on the global graph.

Beijing’s Belt and Road Initiative has funded a range of infrastructure projects across the Eurasian continent and beyond, from roads and railways to power plants. Construction on the 2,000km crude-oil pipeline and the almost-complete Lagos-Ibadan railway has ground to a halt, the Chinese workforce not having been on site since just before the Chinese Lunar New Year in February 2020 (Kitimo, 2020).

Africa/China trade and commodities

Besides oil, Africa’s other commodities are also closely linked to China’s fortunes. Depreciations in industrial commodities are hitting resource-dependent economies hard.

The Congo’s commodity exports amount to 70% of GDP with exports to China accounting for 50% of total GDP (Smith, 2020).

Copper prices are down by 7%, which in turn will lower the value of exports from major suppliers – Zambia, the Republic of Congo and the Democratic Republic of Congo.

Africa’s copperbelt region produces 70% of the world’s cobalt and supplies a large percentage of global demand for lithium and other rare minerals.

China is the biggest importer of cobalt and rare minerals, being the world leader in the production of mobile phones, electric car batteries and hi-tech components (Smith, 2019). China also has significant investments in mines in the copperbelt region, exercising their control over value chains in the mining sector. With the overall China downturn, investments in these ventures have also slowed.

Chrome, manganese and iron ore make up two-thirds of South Africa’s total exports to China. Less demand for these metals has caused listed shares of these mining companies to tumble (Times Live, 2020).

Soft commodities like coffee, tea, rose flowers and cocoa are also suffering due to subdued Chinese demand. The slowdown affects Rwanda, Ghana, Ethiopia, Kenya and the Ivory Coast (Okoth, 2020). South Africa’s fisheries industry took a knock after China stopped all animal imports in January 2020. 95% of the country’s rock lobster harvest is usually sold on to China.

According to researchers at SET, the estimated lost revenue of sub-Saharan exports to China could reach around $420-million. Angola, Congo, Sierra Leone, Lesotho and Zambia have been named as the most economically exposed through exports and tourism (SET, 2020).

Supply chains

China’s record of favourable pricing and efficient logistics has made it a critical player in global demand and supply chains. Many African states have become dependent on Chinese imports like textiles, electronics and household goods.

Kenya’s port of Mombasa has become a regional transport and supply chain hub, receiving goods bound for Uganda, Rwanda, Burundi, Democratic Republic of Congo and South Sudan (Okoth, 2020). Since February 2020, Mombasa has recorded its lowest arrivals of cargo ships to date, with 37 cancellations and a further 104 scheduled dockings still uncertain – most of them from China. This has sent ripple effects across borders and down the supply chain, impacting the rail freight service that operates from the port (Kitimo, 2020).

Thousands of small- to medium-sized enterprises on the continent have been forced to shut down after disruptions to supply chains and an inability to store large stocks. China is Kenya’s biggest source market, accounting for up to 40% of all imports. Kenya Importers and Small Traders’ Association say they’ve lost $300-million since the Covid-19 outbreak (Kitimo, 2020). A fourth of all Ugandan imports come from China as well as 60% of all South Africa’s clothing and textiles (Evans and Over, 2020).

Several state-owned Chinese industries are returning to work after Covid-19 cases drastically reduced, but it is privately-owned industries and smaller companies that are really China’s economic engine. They produce toys, textiles and consumer goods and have not regained momentum with workers still idle due to lack of materials and enduring quarantine measures. (Evans and Over, 2020).

Travel

The airline industry has been a major Covid-19 casualty, decimating business across the globe due to containment measures. At the start of the outbreak, much of the loss was attributed to the diminished Chinese tourist market, but the global spread of the virus with Europe now the epicentre, has collapsed all demand in the sector.

Covid-19 has erased up to 15% of global airline capacity, prompting all carriers to take drastic measures just to stay afloat. (Bloomberg, 2020). The graph below indicates airline capacity, illustrating just how much travel has been curtailed in certain regions, mirroring the aversion regulations countries have put in place to stop Covid-19 infection rates.

The following is a list of the draconian measures global airlines are taking:

- Deutsche Lufthansa AG, Europe’s biggest carrier, will ground 700 planes and cancel 95% of seats

- State-owned Dubai airline, Emirates, will ground most of its passenger fleet, reducing destinations from 145 to 13 and cut wages to half

- British Airways is set to cut back 75% of operations over the next two months

- Australia’s carrier, Qantas Airways, will stop all international operations in March 2020, slash domestic operations by 60% and temporarily lay off up to 30,000 staff

- Delta Airlines in the US is reducing its operations by 70%

- Abu Dhabi-based Etihad is grounding its Airbus A380 fleet along with an entire premier class of service called “The Residence”

- Virgin Atlantic is to reduce 80% of its flights and staff requested to take eight weeks of unpaid leave

- Irish carrier Ryanair has cut capacity by 80% and is considering grounding its entire fleet

On the African continent, airlines have taken similar measures to avoid bankruptcy. The sector has already lost $4.4-billion in revenue since the start of the pandemic. According to data from the International Air Transport Association (IATA), there has been a 20% decline in international bookings and a 15% drop in domestic travel in Africa for March and April 2020.

South African Airways (SAA) has cancelled all international flights until the end of May 2020 in response to the government declaring a State of National Disaster in South Africa as Covid-19 cases surpassed 400. A further 124 regional flights were also grounded (Omarjee, 2020).

The beleaguered South African state-owned airline was placed under business rescue in December 2019 to avoid bankruptcy after years of mismanagement and corruption that accumulated a $1.6-billion loss.

Kenya Airways was also facing a battle for survival before the Covid-19 impact, after years of increasing debt and allegations of state corruption (Kuo, 2020).

Royal Air Maroc, Air Tanzania, Air Mauritius, EgyptAir, RwandAir, SAA and Kenya Airways have all suspended flights to and from China. On the other hand, for Africa’s most profitable carrier, Ethiopian Airlines, it is business as usual for its China routes. The airline countered calls to suspend its 35 weekly flights to China, arguing that the measure would not slow the spread of Covid-19 (Logupdate Africa, 2020).

Hand-in-hand with a collapse of travel goes tourism, hospitality and entertainment. Cancelled national celebrations, sporting events, cultural and religious practices, art, music and literary festivals and conferencing are decimating these industries which face large-scale job losses.

Economic vulnerability indicators

It is clear that curtailed investment, trade and freedom of movement will result in a global slowdown and they will render economies vulnerable. But vulnerabilities are also dictated by other internal or national factors. Should the pandemic reach high infection rates in African countries and should there be a high degree of community transmission (viral infections from and between local persons), local productivity and local value chains across sectors will be further impacted. The health of national coffers, the level of debt and the state of currency reserves are all internal factors that add to this economic vulnerability.

From this understanding, SET (2020) has compiled an index with several measurable indicators that helps to evaluate a country’s status. Among the 10 most significant indicators are:

- Confirmed Covid-19 cases

- Reduction and cancellation of key airlines

- Travel restrictions

- Total trade with China as percentage of GDP (both exports to and imports from China)

- Inbound Chinese tourism

- Foreign direct investment (as net inflows in % of GDP, as well as China’s outward FDI)

- External debt in % of GDP

- Current health expenditure as % of GDP

- Healthcare access and quality

- Migrants as % of population

Many of these indicators are drawn from slow-changing variables and can be fairly reliable over the course of time. Confirmed infection rates and changes in travel restrictions are perhaps two of the more volatile and subject to more drastic changes. These could significantly affect the weighting of indicators and the placement of countries on the graph.

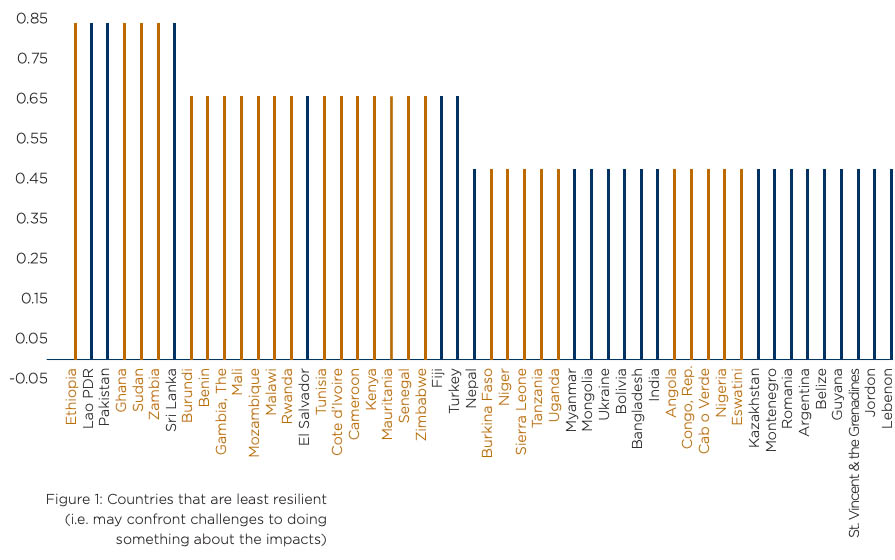

Drawing from the SET methodology, Ethiopia, Ghana, Sudan, Zambia and Burundi are the five African countries least resilient to the economic impacts of Covid-19. These countries top the list because they have less fiscal capacity to buffer the impacts along with poor quality health systems and poor access to them (SET, 2020). Out of the 50 least resilient countries listed on the graph, half are in Africa.

Remedies

Creative combinations of monetary and fiscal policy measures will need to make up a multi-faceted response to the economic impacts of Covid-19.

Central banks across the world and in Africa have taken unprecedented measures to reduce interest rates in a bid to arrest a downward economic spiral. But many analysts agree that rate cuts are just a plaster on a gaping wound.

Several sub-Saharan African states are in a technical recession, three of the region’s bigger economies, Angola, South Africa and Nigeria are particularly vulnerable. Combined with Covid-19 impacts, slumping markets and rising unemployment, rate cuts are considered merely reassuring measures that could cushion the blow.

What has been called for are targeted measures to help businesses deal with the short-term crisis and cash flow. Targeted relief is being extended in hard-hit countries like Italy, Denmark, China and the US.

Several African countries have also extended economic support packages, especially for small and medium enterprises that are being throttled. South Africa has announced that a Temporary Employment Relief Scheme will be made available for companies in Covid-19 distress. This scheme is meant to pay salaries directly to employees to avoid retrenchments while reserves in the Unemployment Insurance Fund are also on standby to supplement loss of income for companies unable to foot their wage bill (Chothia, 2020).

Several tax regulations have also been relaxed for compliant SMMEs across several African countries. Mauritius, Kenya and South Africa will expedite value-added tax refunds in the next few months as well as delay categories of tax payments to their respective revenue services without penalties. Banks across these countries have been instructed to suspend and extend loan repayments for affected businesses with existing facilities as well as allow for higher borrowing limits (Chothia, 2020, Reuters, 2020, Central Banking, 2020).

Stimulus packages are able to boost the economy and provide funding to cover the rising costs of the pandemic which include boosting health expenditure. For many African countries, stimulus packages are not affordable, but that doesn’t mean fiscal responses are entirely off the cards. Economists suggest redirecting funding from existing budget line items rather than increased borrowing (Krugel and Viljoen, 2020).

This measure would support additional health resources and other containment measures. This is one of the routes several African nations are taking, but the more economically vulnerable countries like Kenya predict they won’t be able to cope. Kenya is now seeking emergency assistance of $350-million from the International Monetary Fund, much of it to be directed towards the national budget. Kenya has already approached the World Bank for $60-million to support its health sector to better respond to Covid-19 (Reuters, 2020).

Deep cooperation between global leaders and with the financial industry is a prerequisite to stem the human and economic cost of Covid-19. What is significant is the sense of agency that governments and powerful global institutions have been forced to exercise. Relaxing regulations and punitive conditions around tax, banking and debt has allowed governments greater freedom in making economic decisions in the interest of their citizens. Neo-liberal orthodoxies have traditionally limited government interventions and prioritised market interests. Covid-19 has catalysed a crisis that is reshaping this condition to more fully embrace labour, competition regulations and the price of essential goods and services.

United Nations chief, Antonio Guterres has warned that a global recession is likely. “This is a moment that demands coordinated, decisive and innovative policy action from the world’s leading economies. We are in an unprecedented situation and the normal rules no longer apply.”

In the case of Covid-19, no country is safe until every country is safe – a fact of our deeply interconnected and interdependent realities. This pandemic is going to require the reset of rules thought previously immutable, especially economic ones that have over a long period sustained or maintained deep structural inequality. DM

Nina Callaghan & Mark Swilling, Africa Focus Project, Centre for Complex Systems in Transition, Stellenbosch University. Funding support by Bowmans Law Firm.