The average fees charged by the average balanced unit trust, with a mixture of local bonds and equities, in SA is almost three times as high as a similar fund would cost in the US. (Photo: Pexels)

The average fees charged by the average balanced unit trust, with a mixture of local bonds and equities, in SA is almost three times as high as a similar fund would cost in the US. (Photo: Pexels) What should you be paying for good investment advice and balanced investment returns?

According to the latest Morningstar Global Investor Experience study (GIE) released in September, local fee structures have improved from “above average” to just “average” compared with the rest of the world.

But it’s a bit more complicated than this because what is included and excluded from fee structures is a bit of a moveable feast.

The biennial report compares unit trust markets across the world, based on the fees investors are paying. This study does not, however, evaluate the potential total cost, including financial advice and brokerage cost, which is not readily available in many jurisdictions, including in South Africa.

Financial advice comes in many different forms, but normally, it’s what you pay your financial adviser. Brokerage cost is the fee you pay to actually buy the shares that form part of unit trusts, for example.

“Advice fees can vary by investor, advisory firm and account type, and fee schedules are not required disclosure in the same way as the various fees associated with a registered fund itself,” Morningstar reports.

“Given the differences in the way fees are calculated, reported, and named across different markets, it can be difficult to ensure like-for-like comparisons,” the organisation says.

The study methodology still tends to penalise costlier fund markets where it’s been common to bundle advice and distribution fees into fund expense ratios.

So average might be less average, or is that more average, than it seems.

Even the “average” description doesn’t quite capture the comparison.

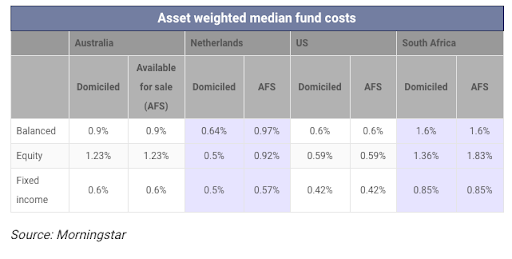

As the chart below shows, the average fees charged by the average balanced unit trust, with a mixture of local bonds and equities, in SA is almost three times as high as a similar fund would cost in the US and the Netherlands. In Australia, it’s about 50% cheaper.

South Africa’s Fees and Expenses grade falls to average in this study, because local unit trusts are relatively expensive, with a median of 1.60%, while the medians for local equity and fixed-income funds are 1.36% and 0.85%, respectively.

But the key takeaway of the study is that there is a clear trend towards lower fund fees globally. Most of the 26 markets studied saw the asset-weighted median expense ratios for locally domiciled and available-for-sale funds fall since the 2017 edition.

The trends that were driving fees lower include regulation such as the the UK Retail Distribution Review, Australian Future of Financial Advice, and the subsequent Banking Royal Commission as well as the Markets in Financial Instruments Directive, which have all hastened the lowering of fees for investors in the UK, Australia, and some European markets, particularly the Netherlands. In 2018, the Indian market regulator the Securities and Exchange Board of India also intervened, reducing the expense ratio cap for funds across Indian categories.

When South Africa’s Retail Distribution Review (RDR) was announced in 2014, much was made of how it would profoundly change the financial services industry. To meet its aims of professionalising financial advice, helping customers make informed decisions and promoting fair competition, it would require some major shifts in how products are accessed and paid for.

Five years later, the implementation of RDR has been slower than might have initially been expected and is yet to come into force.

Where South Africa is in line with many other jurisdictions is that investors, in general, are becoming more aware of what they are paying. This is because of increased scrutiny from the media, regulators and government.

“Investors have realised that minimising costs is very important,” says Michael Kruger, investment analyst at Morningstar Investment Management South Africa.

“They are moving into cheaper products and this has increased the competition between managers. This has forced active managers, in particular, to bring down their fees in order to compete.”

However, this hasn’t been as pronounced as other markets, or investors, would have liked. This is particularly the case with the large local managers who dominate the landscape.

“They have enormous scale benefits, but in many cases aren’t passing these on to their clients,” Kruger adds.

“There is a point where additional assets under management don’t require incremental costs,” Kruger says. “We would expect managers who have significant assets to decrease the fees that they charge and pass this benefit back to investors, but I don’t think that is happening in the South African environment.”

The fact that passive investing has also not yet gained significant traction in South Africa also means these asset managers are not facing the same threat from this as their international counterparts.

“Globally, there has been a big move to passive, particularly in the US, where we have now seen assets under management in passive equity funds overtake those of active,” Kruger explains.

“In the US, firms have moved away from charging performance fees because regulation says you have to use a fulcrum fee – that the manager has to participate in the downside,” Kruger adds.

The Morningstar study finds local performance fees problematic in that they are charged on different structures by different managers, and are generally difficult to understand.

“We sit down and try to work out how each of these fees is calculated, and it’s not easy, so it is very difficult for the person in the street to understand what they are paying,” Kruger notes.

“Disclosure on performance fees is generally not great from managers either. The way they explain how they work doesn’t do enough to explain how they are calculated and charged.”

The added complication is that what the investor is paying can change significantly over time.

“Performance fees can change drastically from year to year,” Kruger points out.

Earlier in 2019 the Association of Savings and Investments (ASISA) issued an update on the Effective Annual Cost (EAC) measure, a standardised disclosure methodology — to replace TER — that can be used by consumers and advisers to compare charges on most retail investment products, and their impact on investment returns, to remedy some of these challenges.

“The EAC is a measure of the charges that an investor will likely incur in purchasing and holding a financial product and does not attempt to measure the features of a financial product,” ASISA states.

Other initiatives to standardise and centralise the unit trust proposition are also on the way.

Cost certainty is best for all investors at the end of the day, concludes Kruger. BM