Discovery CEO Adrian Gore. (Photo: Gallo Images / Freddy Mavunda)

Discovery CEO Adrian Gore. (Photo: Gallo Images / Freddy Mavunda) Of all of the listed companies likely to be impacted by the arrival of NHI, medical scheme administrator Discovery appears to have been hit the hardest.

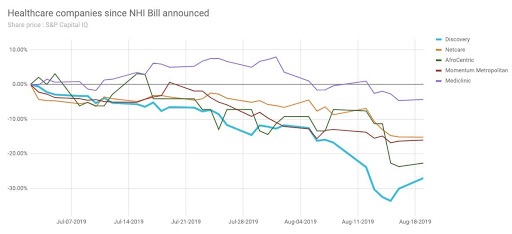

The NHI Bill was tabled in parliament on August 8th and lays the groundwork for the establishment of a central fund that will purchase medical services for all in South Africa. While much about the Bill is not clear, what seems apparent is that the role of medical schemes will be limited to providing cover for benefits not provided by the fund.

In addition, the bill makes no provision for private scheme administrators. Considering that 39% of Discovery’s bottom line profit comes from this activity, the advent of NHI – even if it’s a decade away - might concern some investors.

As a result, the share prices of administrators, as well as the private hospital companies and drug manufacturers, all dipped sharply on the news, which really hit the street on the 9th August, with Discovery losing 15% of its value, AfroCentric 20%, Momentum 3.5%, Netcare 10% and Aspen 21.5%.

Since then most of these companies have seen their share price stabilise – although they have not recovered – with the exception of Discovery, which continued on its downward trajectory before coming back a bit. This makes one wonder if there is more at play?

As it turns out, some investors are concerned about Discovery’s balance sheet, and its accounting practices, which are said to be more ‘aggressive’ than the likes of Sanlam and others in the insurance sector. In this frazzled investment climate, investors are exceedingly cautious and any warning signs are enough to send them skittering out of the share.

In a recent note to clients Terence Craig, chief investment officer at Element Investment Managers, said: “We are concerned that Discovery may become a future ‘Market Darling turned Fallen Angel’ as there appear to be multiple and material warning signs, similar to other companies in our “Angels Eleven” table.”

The warning signs he says include: share prices that reached all-time highs (ATH) in the five years to end 2018; a share price that fell -50% or more from their ATH to end December 2018; investors who are willing to ‘pay-up’ for the value inherent in this market darling and ‘game-changing’ acquisitions, among others.

Source: Element IM second quarter newsletter

In the note, Craig goes on to cite research conducted by Citigroup insurance analyst, Francois du Toit, who is himself an actuary. Du Toit says that Discovery made two noteworthy changes to its assumptions, one in 2013 and the other in 2018.

In the first, Discovery changed its assumption relating to the length and cash flow profile of its in-force SA Life policies. It extended the duration of the contracts from 20 to 40 years and significantly increased the cash flow stream from year 20 onwards. Considering the Life business was only launched in 2001, this was definitely not conservative accounting - particularly as Discovery had seen a number of policies lapse closer to the ten-year mark.

The implication is that this effectively increased Discovery’s SA Life policies profit growth rate by about 5% a year.

In 2018 Discovery changed its method of estimating future inflation, investment returns and risk discount rates. Simply, it increased its inflation assumption and lowered its risk discount rates. That means that the company now assumes future inflation will average 7.48% per year.

“The inflation rate has not been this high in any of the past 120 months,” says Craig. “This is also well above the target of 4% to 6% set by the SA Reserve Bank.”

However, this change added R5-billion to the value of these existing contracts, which means that Discovery shows a higher, growing stream of net cash flows relative to the lower flat stream of net cash flows from SA Life policies it would have shown before the assumption changes.

None of this information is necessarily new, it’s just that investors are looking at it with slightly more jaundiced eyes – as if often the case when a balance sheet becomes a bit debt-heavy, earnings are not quite as sprightly as in the past, and the launch of a much-anticipated project – namely Discovery Bank – is slower than expected.

In the first half of this financial year the company reported earnings that were weaker than expected – normalised headline earnings decreased by 16%. This was driven by a disappointing performance from Discovery’s SA Life Business, as well as ongoing and significant investment in its new and emerging businesses. To be fair the emerging businesses, Discovery Insure, Vitality Group and Ping An Health, grew strongly and offer promising growth in the future.

But the launch of the newest baby, Discovery Bank, has added about R5-billion to the balance sheet, bringing total amortised borrowings up to R14.6-billion.

Citi’s Du Toit estimates that Discovery would need to generate net cash earnings of about R700-million per year to generate excess returns on the R5-billion net invested to date.

“We agree with Citi’s view that it will likely be many years before the bank generates this level of earnings and that there is at least an even chance that Discovery will destroy shareholder value in banking,” says Craig. “Discovery has borrowed heavily and also raised shareholder capital to build the bank. It will need to earn a significant level of net cash profit to repay funding costs and shareholder required returns.”

Discovery is in a closed period and reports its full-year results on September 4th. One hopes the results will allay investor concerns.BM