The listing requirements for public companies, arduous as they may be, increase transparency and raise standards of corporate governance in the corporate sector. (Image source: Pixels/Pexels)

The listing requirements for public companies, arduous as they may be, increase transparency and raise standards of corporate governance in the corporate sector. (Image source: Pixels/Pexels) The recent Nasdaq listing of plant-based meat company Beyond Meat shot the lights out, with the share opening at $46, almost double the $25 initial public offering price tag, and closing the day at $65.75. This was easily the most successful initial public offering (IPO) of 2019.

Other high-profile, but less successful listings in 2019, include ride-hailing companies Uber and smaller rival Lyft, as well as office communicators Slack, and Zoom Video Communications, social media firm Pinterest and the iconic Levi Strauss. Airbnb and big data company Palantir are expected to come to the market in 2019 too.

This could be a record-breaking year for listings in general, potentially even surpassing the dot-com boom years.

“We think it is possible that 2019 could prove to be a record year for capital raised in the IPO market, at over $100-billion in issuance, exceeding the amounts raised in 1999 and 2000,” says Kathleen Smith, principal at investment bank Renaissance Capital.

Given this news, it is surprising to learn that the number of publicly listed companies is not rising, but is declining, dramatically so. In the US the number of listed companies halved from 8,000 to 4,000 between 1996 and 2018 with the number of annual listings falling from an average of 300 a year in the 1980-2000 period to 108 a year since. In the UK the number of listings fell from 2,500 to 1,200 and in South Africa, in the same timeframe, it dropped from 600 to 361.

“It is quite striking, even across countries with different levels of economic performance, that the trend is the same,” says Gavin Ralston, head of thought leadership at Schroders. “We are seeing a declining appetite for new listings, and a consistently high number of companies delisting, thanks to mergers and private equity buyouts.”

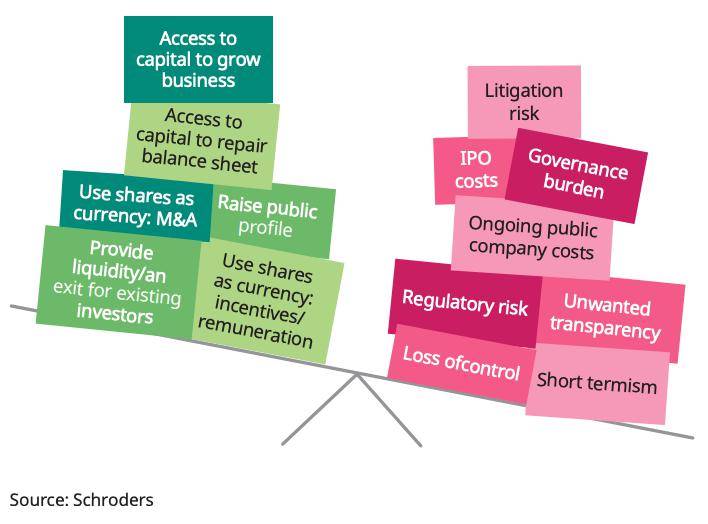

The stock-market cost-benefit analysis

While the past two decades have borne witness to incredible boom and bust cycles, this decline cannot be ascribed to fewer companies being created or more start-ups failing.

“The number of new businesses has risen over the past 20 years,” says Ralston.

Rather, cheap debt and more accessible and robust private equity markets have taken market share.

Not only is the cost of debt cheaper, but companies are able to access quantities of capital that would not have previously been possible outside public markets. Facebook raised $2.4-billion before its $16-billion IPO in 2012, Twitter $800-million before its $1.8-billion IPO in 2013 and Google a scarcely believable $25-million before its $1.9 billion IPO in 2004.

But this has changed — Didi Chuxing, a Chinese transport technology group, raised $17-billion privately. If companies do list, they do so at a later stage of development. Ride-hailing company Uber was 10 years old — mature by tech-company standards — when it made its Wall Street debut.

Like Didi, it had already raised $10.7-billion privately, from the likes of Black Rock, Fidelity Investments and Saudi Arabia’s Public Investment Fund. This proves the point that private capital is available and hungry for investment.

The increasing cost and hassle of maintaining a public listing are also putting companies off. Corporate scandals such as Enron contributed to a rise in regulation, making complying with listing requirements more onerous and expensive. For instance, the average number of words in a US regulatory filing, (the summary of a listed company’s performance which must be submitted annually to the Securities and Exchange Commission), more than doubled from 23,000 in 1996 to nearly 50,000 in 2014.

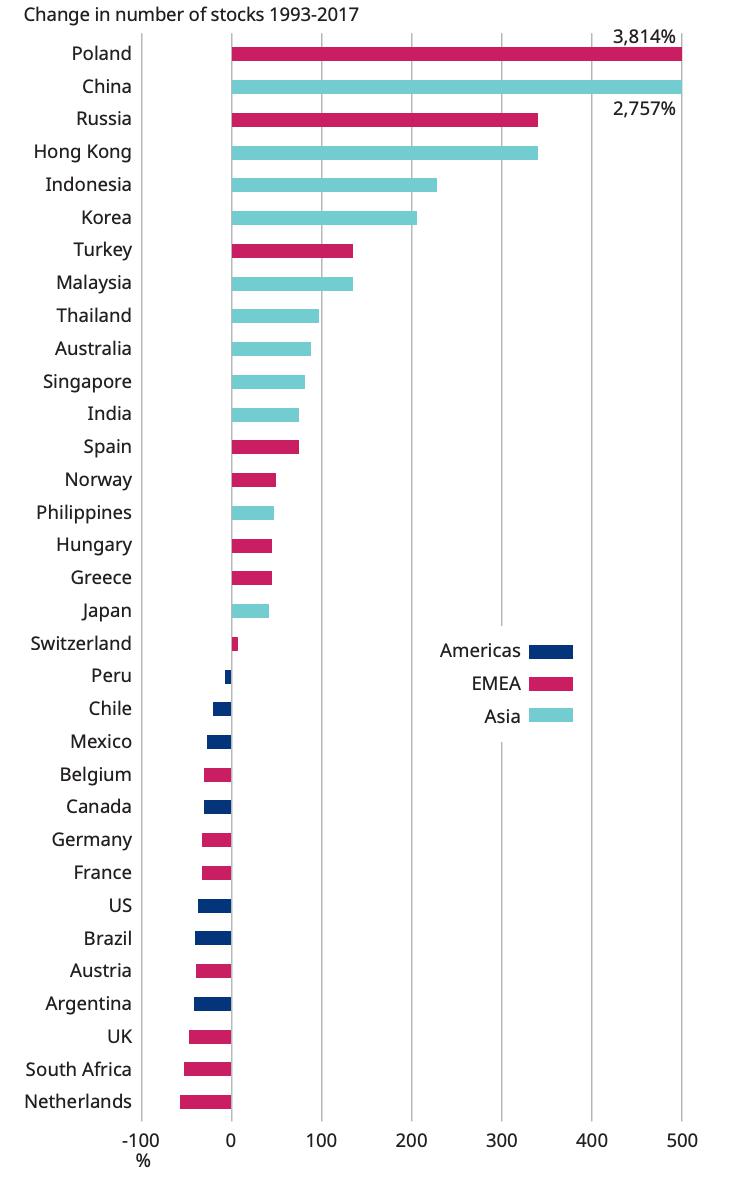

However, according to Schroders, not all public markets have struggled to attract companies. Some have thrived. Emerging markets have fared far better than developed, driven by buoyant growth in Asia and parts of Europe.

“If a country has relatively immature capital markets, as is more common in emerging markets, the rate of new listings seems to be higher,” says Ralston. Former communist countries did not have any capital markets in 1990, so have been starting from a very low base.

The Polish stock market is a good example of this. It had only 22 stocks in 1993 and now has more than 800. Similarly, China’s capital markets have rapidly expanded from just above 100 companies in 1993 to more than 3,000 now, and are continuing to grow at a rate of several hundred a year.

Source: Schroders

Does this matter, one wonders? Ralston believes that it does. A thriving public equity market is the easiest and cheapest way for ordinary savers to participate in the growth of the corporate sector. Because Regulation 28 of the Pension Funds Act has negligible allocations to private equity and other illiquid “alternative” assets, ordinary savers are at a disadvantage to institutional investors who can and do hold more.

Also, public market investors are now accessing companies at a much later stage of their development than in the past, if at all. Given that growth is generally most rapid in those earlier years, it is possible that public market investors are missing out on returns as a result.

It seems ironic that listings are declining as shareholders are finding that they have a voice on issues like remuneration, corporate governance and environmental risks. The listing requirements for public companies, arduous as they may be, increase transparency and raise standards of corporate governance in the corporate sector. BM