/file/dailymaverick/wp-content/uploads/jess-zondo-april1.png)

SYSTEM IN DECLINE

Leaking pipes, filthy rivers and health risks exposed in SA’s latest water report cards

By Tony Carnie

/file/attachments/orphans/drop1adurbanwaterburstimagesupplied_471293.jpg)

Your local

Newspaper

Enter your email below and we'll send you a one-time pin to log in.

PERSONAL FINANCE

SURGING COSTS

BUSINESS MAVERICK

BUSINESS REFLECTION

NEWSFLASH

MAVERICK CITIZEN

PHOTO ESSAY

FOOD BASKET

BHEKISISA

MAVERICK CITIZEN

TOXIC BATTLES

MAVERICK EARTH

SYSTEM IN DECLINE

GAME-CHANGER

NET HARM OP-ED

SCORPIO

VIDEO

SCORPIO

NEWSFLASH

SCORPIO

SOLE MATES

MOVING ART

GUEST ESSAY

REPORTER’S NOTEBOOK

LET ME ENTERTAIN YOU

OOPS, WE MISSED THAT!

ROYAL CONFUSION

OBITUARY

FUMBLING FIELDERS

MUNICIPAL VOTE

CHANGE MAKER

WHAT WE'RE WATCHING

JOBURG WEEKEND

THE CONVERSATION

THE CONVERSATION

CRITICAL CROSSROADS

INTERNATIONAL RELATIONS OP-ED

HIDDEN INFLUENCE

NET HARM OP-ED

OPEN LETTER

FUMBLING FIELDERS

PANEL DELAY

EURO PAIN

SCHOOLBOY RUGBY

MOTORSPORT

WHAT’S COOKING

OP-ED

THE CONVERSATION

THE CONVERSATION

WHAT'S COOKING

OOPS, WE MISSED THAT!

MUNICIPAL VOTE

NELSON MANDELA BAY

COUNCILLORS MOVE TO OUST MAYOR

LANGUAGE EQUALITY

MAKING A SPLASH

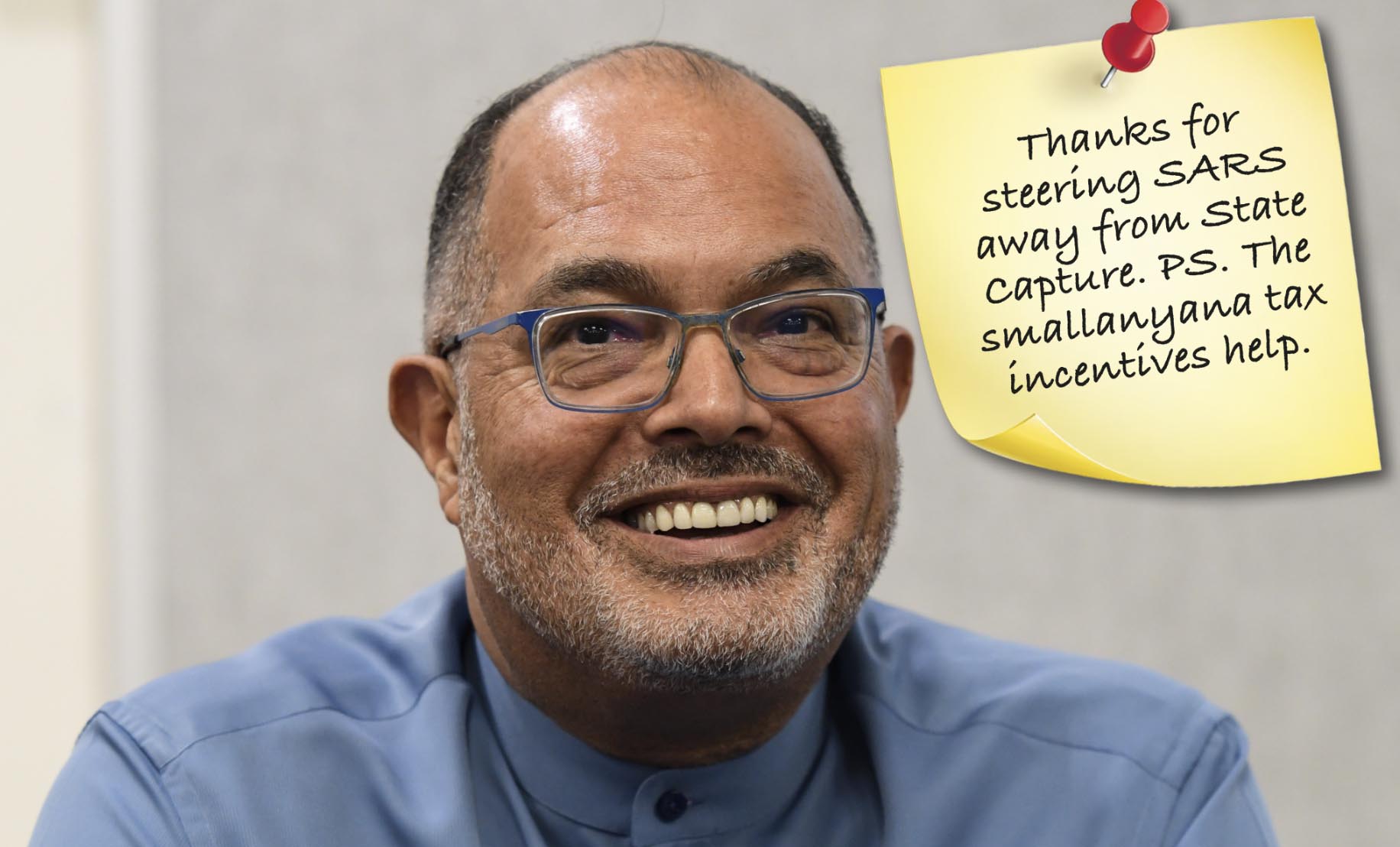

SARS HELM

AGE OF ACCOUNTABLITY

MATTER OF TRUST

OPINIONISTAS

OPINIONISTAS

OPINIONISTAS

OPINIONISTAS

MAVERICK EARTH

SPONSORED CONTENT

SPONSORED CONTENT

SPONSORED CONTENT

SPONSORED CONTENT

SPONSORED CONTENT

DAILY MAVERICK WEBINAR

DAILY MAVERICK WEBINAR

DAILY MAVERICK WEBINAR

SPONSORED CONTENT

BRAZEN INSIGHT

VIDEO

VIDEO

VIDEO

VIDEO

VIDEO

/file/attachments/orphans/WhatsAppImage2026-03-24at115511_881588.jpeg)

/file/attachments/orphans/GettyImages-2264385014_455240.jpg)

/file/attachments/orphans/72489587_631756.jpg)

/file/attachments/orphans/2267774324_155239.jpg)

/file/attachments/orphans/ED_602496_350753.jpg)

/file/attachments/2990/equalstock-h-5uK6ylGbQ-unsplash_591348.jpg)

/file/dailymaverick/wp-content/uploads/2024/06/MC-FoodBasket-Jan26.webp)

/file/attachments/2990/260331dm_835160.jpg)

/file/dailymaverick/wp-content/uploads/2022/07/MC-Tues-5July_1.jpg)

/file/attachments/2990/Image111_546975.jpg)

/file/attachments/orphans/MichellePfeifferasStacyClyburnandBeauGarettasAbigailReeseinTheMadisonEmersonMiller_Paramount_715271.jpg)

/file/attachments/orphans/Craig-Grays-Hospital_158844.jpg)

/file/dailymaverick/wp-content/uploads/2022/08/VC.jpg)

/file/attachments/orphans/BM-Ed-IranwarIMFcopy_826112.jpg)

/file/dailymaverick/wp-content/uploads/2025/08/TL_2348892.jpg)

/file/attachments/2990/CROSSWORD-Wide3_303717_438092_545791_735455_576816_397448_192563_516024_742016_476552_574433_607475_205455_112344_110825_859417_836515_732848_643584_919950_322278.jpeg)

/file/attachments/orphans/WhatsAppImage2026-03-30at190703_234685.jpeg)

/file/dailymaverick/wp-content/uploads/2025/06/2209900329.jpg)