Increasingly, investors are split between their wish for higher dividends in the short run and the need to assure company stability over the long term. Finding the “best of both worlds” in allocating the rising cash pile is key for the future of the industry, according to Josh Wolfson, an analyst at RBC Capital Markets.

“Miners in general are exposed to significant external factors that are out of their control,” said Simon Jaeger, a portfolio manager at Flossbach von Storch AG, a top-10 investor in both Newmont Corp. and Barrick Gold Corp. “It’s certainly a reason for not paying too much in dividends,” he said. “You want to have the cash buffer on your balance sheet in order to be financially flexible when prices get worse.”

Gold prices are currently at a seven-year high as concerns mount that the coronavirus outbreak in Asia will derail global growth. In a sign that the virus is already starting to dent the world’s largest economy, business activity in the U.S. shrank in February for the first time since 2013. The metal jumped as much as 2% on Friday as the S&P 500 Index was posting its first weekly loss since January.

Gold producers are “gushing cash,” said John Hathaway, senior portfolio manager at Sprott Asset Management, in support of the higher dividends. “They are in a position to raise their dividend,” he said. “And there will be boardroom pressure and shareholder pressure to do that.”

The industry has been blasted in the past for underspending on production, overspending on acquisitions and piling up debt. Now, though, after years of fat-trimming, miners and their investors are well-positioned to gain from the higher prices. That’s allowed companies including Barrick and Newmont to boost free-cash flow and, to varying degrees, reward shareholders.

Earlier this month, though, Mark Bristow, Barrick’s chief executive officer, sent a warning shot across the bow of the industry. Even if all current projects work out, he said, gold supply will still fall 30% by 2029. While sinking supply would be bullish for bullion prices, margins and revenues could be hit if companies are forced to mine lower-grade or hard-to-access deposits.

The divide between whether to push profits or new production has become more focused this year.

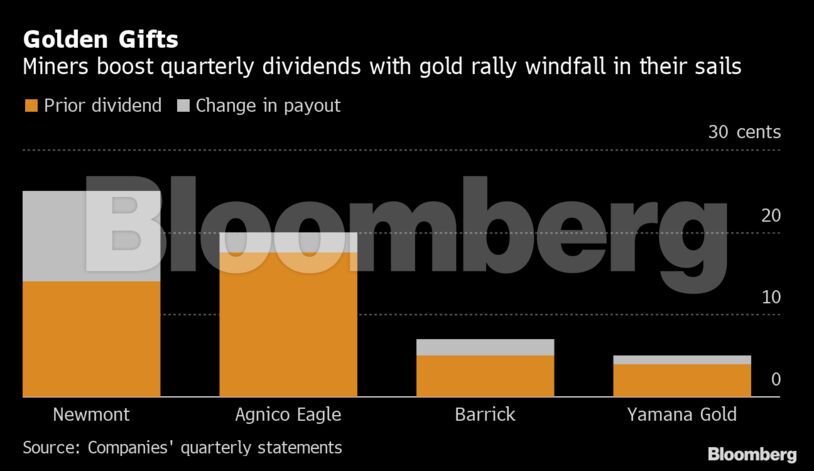

Agnico Eagle Mines Ltd. offers a case in point of how closely investors are watching the issue. Despite boosting its dividend 14% and forecasting rising production through 2022, Agnico’s shares were punished after it cut its 2020 output guidance earlier this month. In an interview after the results, CEO Sean Boyd argued that dividend increases are important not just as a way of sharing the benefits of higher gold prices, but also because it demonstrates a company’s ability to maintain capital discipline.

Success in the changing shareholder landscape is “going to be from the better gold-mining businesses being able to attract new generalist money,” Boyd said by telephone.

‘Endless Pit’

Steve Land, portfolio manager for the Franklin Gold and Precious Metals Fund, believes the next step for miners is to show the sector is “not just this endless pit of having to pour more and more money in all the time.” The trend toward higher dividends is a way of rebuilding trust and confidence, according to Land. These companies can also take the time to assess future projects, he said, but should be “in no rush to push things forward.”

Newmont, meanwhile, seems to be seeking to meet a “best of both worlds” scenario.

In January, Newmont said it planned to hike its dividend by 79% to $1 per share annually, effective in April, while maintaining production for the next five years. On Thursday, Chief Financial Officer Nancy Buese said the U.S.-based miner was considering “other shareholder friendly actions” it might take.

One key consideration “will be to determine our appropriate level of dividend on a go-forward and sustainable basis,” she said.

Also see: Barrick’s dividend boost looks like gold industry harbinger

Barrick, meanwhile, announced a 40% dividend hike to 7 cents a share earlier this month. As it sells assets and tackles its debt, the Canada-based miner is hoping to attract generalist investors to its stock. But it also lowered its five-year production guidance and is reevaluating its portfolio mix.

Generally, it appears the high-dividend strategy is helping lift gold equities. A Bloomberg Intelligence index of senior gold producers lagged the performance of gold futures for most of the past decade. But in the past 12 months, the gold group is killing it, rising 57% compared with 24% for gold.

“If a company has genuine productive opportunities to invest capital in their business at high return, that is always going to be preferable versus paying a dividend,” said RBC’s Wolfson by phone. “But companies which can demonstrate overall discipline by allocating capital effectively -- plus paying out cash flow to shareholders -- I think will ultimately accomplish the best of both worlds.”