Having just completed my 2022/23 income tax return, it became very clear very quickly just how punitive interest income now is from a tax perspective.

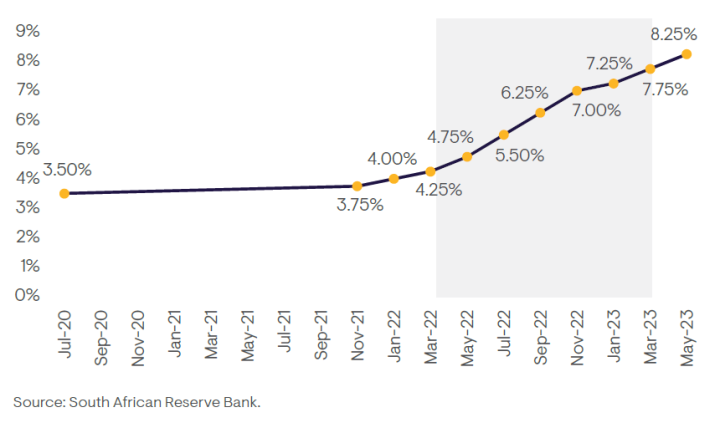

The repo rate has more than doubled, from a low of 3.5% as recently as October 2021 to 8.25%, following the 50 basis-point rate hike in May 2023, as illustrated in the table below. While placing the economy and the consumer under increasing pressure, the higher interest rates on offer have been welcomed by savers and, no doubt, the South African Revenue Service (SARS)!

Graph 1: Recent path of the South African repo rate

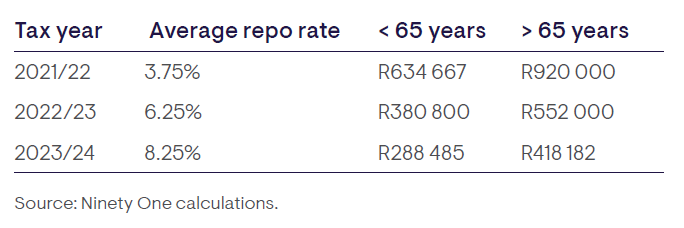

SARS exempts from income tax any interest income earned from a South African source by any individual under 65 years up to R23 800 per annum, and individuals 65 and older, up to R34 500 per annum (there has been no change to these amounts since the 2014 year of assessment). The net effect is that the amount you can hold in an interest-yielding bank or money market account before being subject to income tax at your marginal tax rate has reduced materially. This is illustrated in the following table, where we have used the repo rate as a proxy for the interest earned on a savings account:

Table 1: Estimated savings account thresholds before being subject to income tax

So, the tax-free amount that you could invest in a bank or money market account before incurring income tax fell by approximately 40% from the 2021/22 tax year to the 2022/23 tax year. This comes at a time when retail household bank deposits have reached all-time highs, as South Africans increasingly hide in cash. The South African Reserve Bank’s BA900 economic returns data shows that household bank deposits totaled R1.67 trillion at the end of May 2023. This is significantly higher than the long-term average – and up more than R46 billion over the year to date. At the same time, retail investor assets held in money market unit trust funds amounted to more than R200 billion, as at 30 June 2023. Furthermore, South Africans are holding on to their bank and money market account investments for longer.

Many of us will only fully understand the implications of this in the coming months when we finalise our 2022/23 income tax returns and receive an unpleasant demand from SARS for payment due on interest income earned above the exemption. The following table provides a simple illustration of the effect on someone below 65 years of age, who is subject to a marginal tax rate of 45% for differing amounts invested in a money market account.

Table 2: Illustration of the estimated increased interest income tax paid from 2021/22 to 2022/23

While we cannot do anything now to mitigate this ‘unplanned’ expense for the 2022/23 tax year, we may need to reconsider our financial affairs going into the 2023/24 tax year, especially as you can see from table 1 above that the current amount above which you will be subject to income tax has fallen even further.

What to do, what to do?

We will need to look to alternative, more tax-efficient solutions, as hiding in cash and paying away up to 45% of any excess interest income earned is not the most sensible savings or investment strategy.

Unfortunately, your options are limited. Everyone should be maximising their annual contribution to their tax-free savings account (TFSA), but at an annual limit of only R36 000 this is not going to make a dent. In addition, a TFSA must be viewed as a long-term investment, and therefore the underlying investments should be growth oriented.

Anyone with excess savings and a marginal tax rate of greater than 30% should consider an endowment or sinking fund policy, such as the one available from Ninety One Investment Platform (IP). This is because interest income earned within a sinking fund policy is taxed at 30%, and not your individual marginal tax rate. Ninety One IP also takes care of all tax administration relevant to the investment, including calculating and paying tax on your behalf.

A common concern is that you must remain invested for a minimum period of 5 years. Importantly, however, the Ninety One sinking fund policy does allow one surrender and one interest-free loan within that 5-year period, so you do retain two liquidity options should you require some, or all of your funds. And if you had taken a loan, you have the option to repay it at any time and receive the tax benefits of a matured policy after 5 years, where you can enjoy a regular income stream on which no income tax is payable (only capital gains tax will apply).

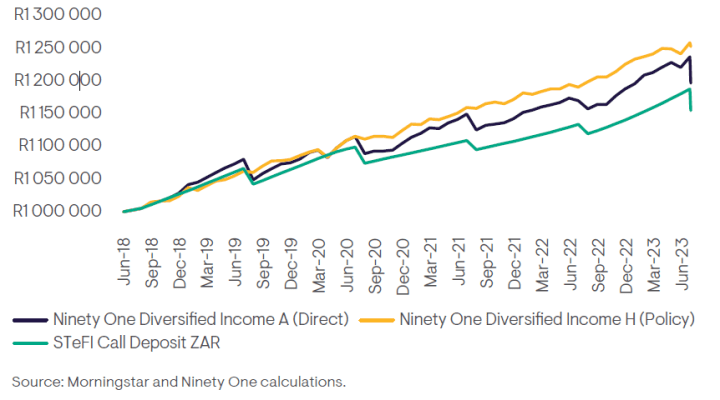

The following graph illustrates the faster-compounding benefits on total investment returns by comparing a R1 million investment held directly in the Ninety One Diversified Income Fund versus firstly, a bank account, and secondly, the same Ninety One Diversified Income Fund investment, but this time held via the Ninety One IP sinking fund policy for the 5 years ended 30 June 2023.

Graph 2: The benefit of a Ninety One IP sinking fund policy

In summary, a direct investment in the Ninety One Diversified Income Fund returned R1.196 million after fees and taxes, R42 000 more than the R1.154 million return of a bank account. However, the real uplift is when investing into the Ninety One Diversified Income Fund via a Ninety One IP sinking fund policy. Here the after- fees-and-taxes return is R1.252 million, R56 000 more than the direct Ninety One Diversified Income Fund investment. This equates to an additional net return of 0.92% per annum.

And finally, earlier this year we announced a 1-year 11% fee reduction for the platform fee class of the Ninety One Diversified Income Fund. We have reduced the H-class annual management fee from 0.45% (ex VAT) to 0.4% (ex VAT), effective from 1 April 2023 to 31 March 2024. This is to further encourage investors sitting in cash to switch to a fund that is well placed to assist them in achieving more meaningful cash-plus returns over time.

The value of independent advice

Given the very real financial and tax planning consequences of this decision, we strongly recommend that investors seek professional financial planning, investment, and tax advice, tailored to their individual circumstances. DM/BM

Comments

Scroll down to load comments...