SPONSORED CONTENT

Avoid getting emotional with your money

There’s a lot to be downbeat about in South Africa – you can take your pick from load-shedding, political uncertainty, poor economic growth and the collapse of many state-owned enterprises – to name a few. While you can’t wish away the steady stream of bad news, what you can do is avoid getting emotional with your investments, says Malcolm Charles, Portfolio Manager at Ninety One.

It’s easy to lose perspective when you are in the middle of a challenging situation over which you don’t have control. Feeling powerless to change adverse external circumstances can drive you to ‘want to do something’. When it comes to your money, panic selling could cost you dearly.

Journeying back in time can be a useful exercise when you’re facing tough times. Most South Africans would agree that 2015-2016 was a dark time for the country. In December 2015, the shock dismissal of then-Finance Minister Nhlanhla Nene sparked a market sell-off. During this tumultuous period, the outlook for South Africa was dismal as political uncertainty and allegations of state capture weighed heavily on the country. Then-President Jacob Zuma was also pushing for a massive Russian nuclear project, which would have been catastrophic for SA if it had gone ahead.

Sentiment was overwhelmingly negative – very similar to now. Inflation and interest rates were on the rise here and globally. The South African Reserve Bank (SARB) hiked its repo rate in January and March of 2016 before pausing. Investors were emotional and panic-stricken. The rand plunged to almost R17 to the US dollar. But a year later, it was back below R13.70. For those who remained invested, government bonds gave a 15.5% return in 2016.

The lesson here is: don’t get emotional with your money. Sure, load-shedding and political mismanagement can leave you feeling emotional, but when it comes to your money keep a cool head. Fortunately, it’s not all bad news, there’s some improving news too.

Progress with rebuilding state institutions

During Ninety One’s interactions with clients around the country this year, a key concern that we kept hearing is that President Cyril Ramaphosa has done nothing since taking the highest office in the country. While the President hasn’t done as much as we’d hoped, the strong turnaround of the South African

Revenue Service (SARS) and progress with rebuilding the prosecuting authorities and the Special Investigating Unit should be recognised as tangible achievements since he took over the reins. Some R12.9 billion has been recovered from plea bargains and other admissions, thanks to the State Capture Commission.

While arrests have taken place, prosecutions have been slow. We need to see meaningful convictions of state capture/corruption to get off the greylist.

Eskom on a much better financial footing

Eskom represents the biggest challenge to post-democratic South Africa. Unfortunately, load-shedding will remain a drag on our economy for at least 24-36 months, and this winter is going to be really tough. Understandably, the problems at Eskom are also a big worry for many of our investors. The good news is that the government has agreed to repay R254 billion of Eskom’s debt, which should provide space for the power utility to focus on operations. National Treasury has also put strict conditions in place to prevent irregular and wasteful expenditure.

The restructuring of Eskom is gathering pace. In time, Eskom’s main asset will be the transmission company, with new energy generation increasingly in private hands. Tax breaks for renewable energy installations will also encourage more businesses to go off the grid or reduce their reliance on Eskom power. Businesses will now be able to deduct 125% of the cost of projects in the first year – which may be a game-changer, as was the case in Vietnam when it adopted similar tax incentives.

Private businesses are planning to add a further 18GW in renewable projects. Transmission capacity may now also be built by these renewable energy companies, creating a pathway to free SA from load-shedding in a few years. Economic growth will be a battle while load-shedding continues to cripple many businesses. Weak or no growth will also have an adverse effect on government finances because of the direct impact on revenue. So, we need to see new Electricity Minister, Kgosientsho Ramokgopa, come with tangible solutions to get us through the next 2-3 years while new generation capacity is being built.

Inflation picture improving

Like many other nations, South Africans have faced the ‘double whammy’ of rising prices and soaring interest rates. Fortunately, this horrible headwind seems to be abating – within the next quarter, we could see the SARB hitting the pause button on rate hikes. Inflation is coming down globally, with data pointing to moderating inflation risks in the US and other parts of the world.

We expect SA consumer price inflation to begin falling in the second half of the year, reaching 5% in the first quarter of 2024. This forecast already takes into account elevated and sticky food and fuel prices, which we are currently experiencing. We remain of the opinion that we are close to the end of the rate-hiking cycle. Given a more favourable inflation and interest rate outlook, we believe the environment will be supportive for local fixed income assets.

What can we expect from SA income funds?

Emotional investors who are concerned about the country’s challenges may have the perception that SA bonds are best avoided. But when it comes to investments, it’s important to understand what’s in the price. We believe SA government bond yields more than compensate investors for the risk they assume.

Our government bond yields remain attractive versus emerging market bond yields, domestic cash rates and inflation. SA bond investors can earn a yield above 11.5% on 10-year government bonds, which is well above inflation.

Bond investors can also take comfort that government finances remain healthy. SARS has materially improved its revenue collection. Thanks to the commodity windfall, government revenue collections have exceeded budgeted revenue since March 2021. Importantly, the government has not gone on a spending spree but banked some of this money. And the good news for bond investors is that National Treasury has reduced its bond issuance for this fiscal year, which represents a tailwind for the bond market.

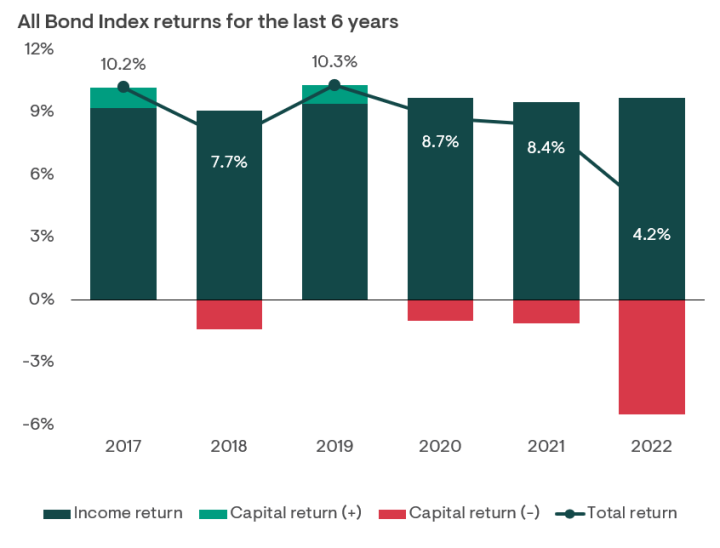

The power of income

Source: Ninety One, Bloomberg, as at 31 December 2022.

The income protection inherent in SA government bonds has helped to shield investors from price weakness. Over the past 6 years, income has been the biggest contribution to SA bond returns, as opposed to capital. Consequently, bonds have been an important source of income for the Ninety One Diversified Income Fund, contributing handsomely to returns.

Positioned to participate and protect

We are happy to own South African government bonds to earn the high yield, given the improved outlook for inflation and interest rates going forward. We do, however, maintain a decent allocation to US dollars to help protect capital against global and local risks. We are marginally overweight government bonds and neutral on local credit. We also have some offshore credit exposure earning an attractive yield of between 6 and 8% in US dollars.

With the US approaching the end of its rate-hiking cycle, we could see the dollar stabilise or even lose a bit of its lustre. The rand will likely hover around R18 to the dollar for the remainder of the year. Unfortunately, South Africa’s energy constraints will continue to limit rand strength. We expect rand weakness to persist relative to other emerging markets (EMs). Our foreign currency position (currently 5%) helps to protect the portfolio from SA risks such as a weak rand.

With inflation decelerating across the world, monetary policy cycles nearing an end, and China reopening its economy, we are constructive on the outlook for EMs and expect attractive returns from SA fixed income assets over the remainder of the year. While uncertainty prevails, we do believe the high yields on SA bonds offer sufficient protection against the risks. DM/BM