SPONSORED CONTENT

Are we at the sweet spot for SA fixed income?

Peter Kent, Co-Head of SA & Africa Fixed Income, and Adam Furlan, Portfolio Manager, Ninety One, set out the case for fixed income assets in 2023.

The deceleration of inflation globally, combined with the growth impact of China reopening its economy, finds emerging markets in somewhat of a sweet spot. Data out of the US at the start of the year showed continued gains in the labour market, but there are indications of some wage normalisation through a slowdown in average hourly earnings. With headline consumer price inflation (CPI) slowing, the Fed could slow the pace of its tightening cycle to 0.25% at its February FOMC meeting.

Across the pond, a relatively warm winter in Europe has softened demand for natural gas and continues to temper energy prices. The relatively benign outlook for global energy prices continues to place downward pressure on global CPI, allowing central banks to take their foot off the throttle and slow the pace of monetary policy tightening.

Late in December, China relaxed their Covid controls, which has already improved sentiment about Chinese growth. This move, combined with measures to support the property sector taken in late 2022, will likely bolster commodity prices and further buoy the commodity-exporting emerging markets.

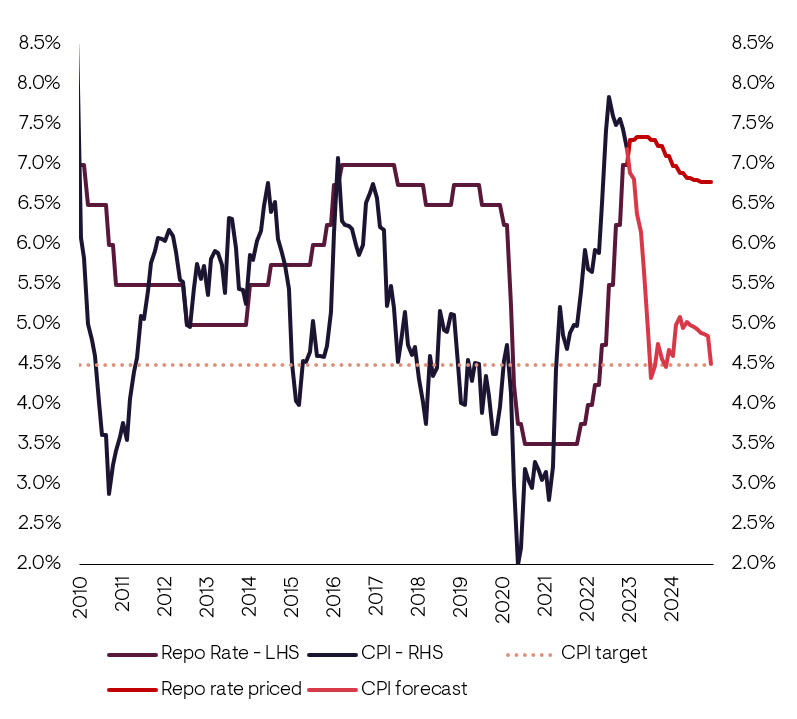

Here at home, headline inflation peaked in July 2022 at 7.8%, falling to 7.2% in December. Looking forward, we see headline inflation averaging 5.4% in 2023, owing largely to declining petrol prices and a deceleration in food inflation. At 7.25% currently, the repo rate reflects a more neutral policy setting (relative to expected inflation). With the inflation picture improving and many of the upside risks abating, we expect that we are close to the end of the SARB’s hiking cycle.

Figure 3: SA Inflation and Repo Rate Outlook

Source: Ninety One, Stats SA and Bloomberg, January 2023.

The growth outlook remains difficult with consumer sentiment souring after a year of rate increases and high inflation. We remain optimistic about private investment in the energy sector on the back of structural reform underpinning our 1% GDP forecast for 2023. As we expect commodity prices to remain elevated, we also see fiscal revenues performing well. This should allow National Treasury to further consolidate the debt burden over the coming year. The economy has shown remarkable resilience to the high levels of power outages in 2022, but load-shedding undoubtably places a cap on sentiment and potential growth.

So how do we construct fixed income portfolios in this environment?

Despite extreme volatility, the Ninety One Diversified Income Fund generated an attractive return over 2022, outperforming bonds and cash while avoiding any negative quarterly returns. We often talk about how the Fund tries to “participate and protect”, and this was very much a year to protect. For most of the last year we thought SA bonds were cheap, but not riskless. So our job was to find a way to own SA bonds, earning the attractive interest on offer, but in a way where we protected the from the many developing risks. With global risks subsiding, local inflation likely to have peaked in the third quarter of 2022 and local political risks abating post the ANC elective conference, we are optimistic on bond market returns.

Hefty income on the table, combined with dynamic portfolio construction, will continue to help protect capital against global monetary policy and growth volatility, and continued load-shedding locally. We remain overweight the 10-15 year sector of the curve relative to longer-dated bonds as valuations look most attractive in this space. These shorter-dated bonds should benefit further from a slowing or pause in the monetary policy cycle over the first half of the year. With yields on credit looking relatively less attractive given where government bond yields are, we remain underweight investment-grade credit. However, we continue to look for yield-enhancing opportunities in high-quality counterparties.

The portfolio’s currency exposure remains underweight, given dollar momentum waning and elevated terms of trade supporting the rand. Yields on offshore credit, however, look attractive. We hold a material exposure to high-quality SA counterparties issuing in dollars, and US investment-grade credit. This portion of the portfolio yields 6.3% in US dollars.

With listed property balance sheets in a healthier position post Covid and the sector paying out dividends again, we have marginally increased our exposure during the fourth quarter of 2022, further reducing our underweight. As we expect a slowdown in economic growth in response to global monetary policy tightening, we remain more constructive on the prospects for SA government bonds relative to listed property.

In summary, with inflation decelerating across the world, monetary policy cycles nearing an end, and China reopening its economy, we are constructive on the outlook for emerging markets. We hold a similar view on monetary policy locally, and combined with continued fiscal consolidation, we expect strong returns from SA fixed income assets in 2023. DM/BM