Illustrative image | From left: Greg von Holdt and a Coast2Coast colleague. (Photo: Supplied) | Greg von Holdt and PIC dealmaker Lawrence Mulaudzi. (Photo: Supplied) | Coast2Coast crew - Greg von Holdt (left), Crispian Dillon (middle) and Gary Shayne. (Photo: Supplied) | Unsplash | Adobe Stock | UIF logo

Illustrative image | From left: Greg von Holdt and a Coast2Coast colleague. (Photo: Supplied) | Greg von Holdt and PIC dealmaker Lawrence Mulaudzi. (Photo: Supplied) | Coast2Coast crew - Greg von Holdt (left), Crispian Dillon (middle) and Gary Shayne. (Photo: Supplied) | Unsplash | Adobe Stock | UIF logo It took only a week in May 2018 to move hundreds of millions of rands in public monies from South Africa’s Unemployment Insurance Fund (UIF) to an array of offshore entities incorporated in places like Malta and the British Virgin Islands.

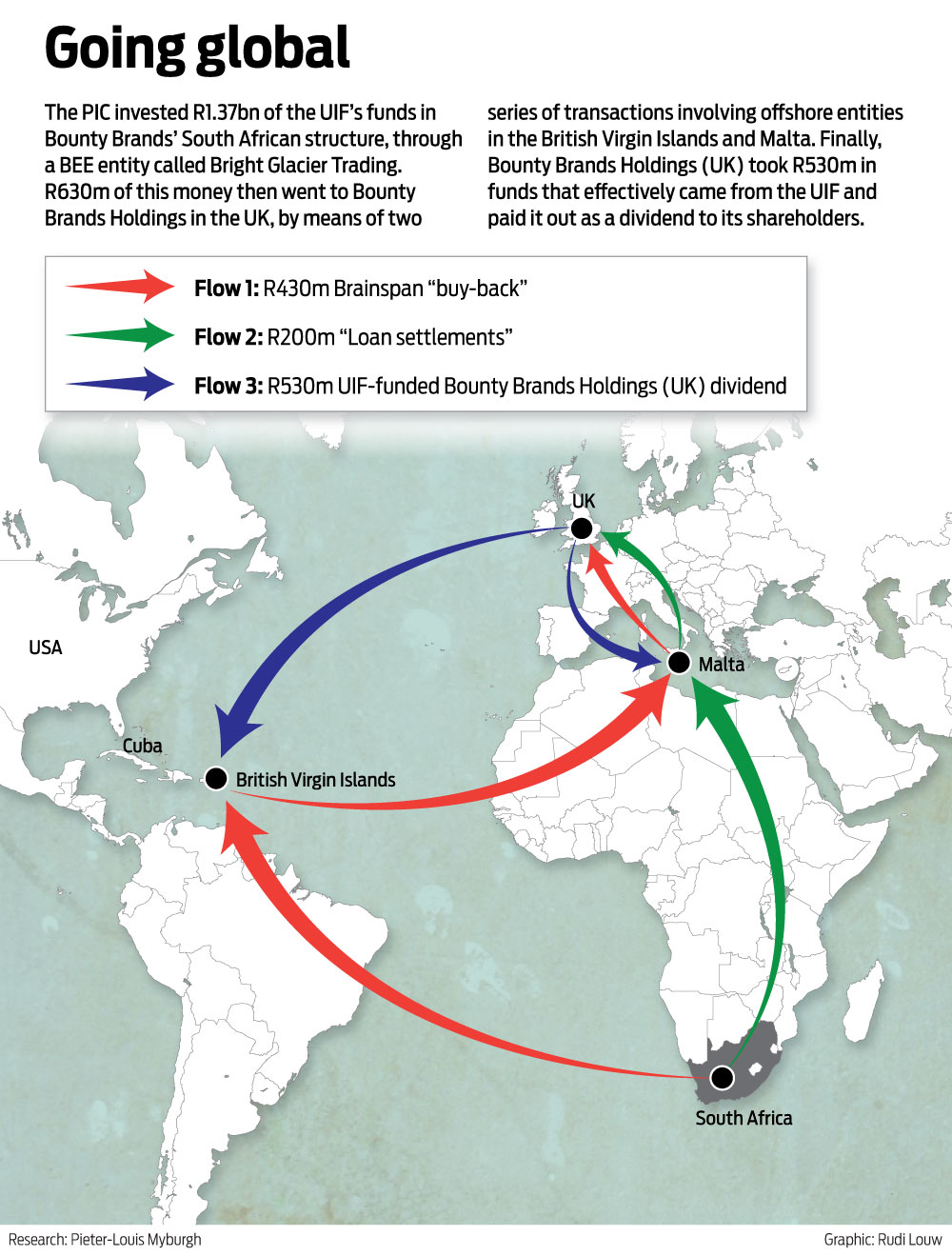

First, through crafty accounting and legal manoeuvring, R630-million of the UIF’s R1.37-billion investment was channelled from South Africa to Bounty Brands’ holding company in the United Kingdom.

Next, the UK holding company paid dividends to its shareholders totalling an eye-watering R530-million.

The dividends were bankrolled with money that effectively stemmed from the UIF’s investment back in South Africa.

Most of this money was paid to entities registered in foreign tax havens.

At least a portion of the dividend was bankrolled through questionable "shareholder loan" payments between various Bounty Brands entities, our months-long investigation has revealed.

Who are Bounty Brands? See all the brands in their stable

By means of these transactions, and using the UIF’s money, the shareholders effectively paid themselves a handsome dividend on the back of unpaid debts owed to some of the consumer goods businesses Bounty Brands had acquired.

What makes this particularly troubling is the fact that Bounty Brands’ founding shareholder — and the largest beneficiary of the dividend — later defaulted on these very debts, triggering a crisis that eventually torpedoed the UIF’s investment.

Bounty Brands was founded by Coast2Coast Capital, a private equity firm headed by Cape Town businessman Gary Shayne, perhaps the lead character in the Bounty Brands saga.

Shepstone Capital, an offshore entity controlled by Shayne, received a R375-million slice of the funds that effectively came from the UIF.

Only five months later, Shepstone Capital starting defaulting on debt linked to acquisitions for the Bounty Brands group.

This left several creditors wondering why some of the UIF’s investment hadn’t been used to settle their debts.

Two of Shayne’s colleagues at Coast2Coast, Greg von Holdt and Johan Botha, also bagged a considerable portion of the dividend, according to documents in our possession.

Von Holdt’s and Botha’s offshore entities collectively received about R55-million, the documents reveal.

/file/dailymaverick/wp-content/uploads/2022/07/Gary-Greg-and-Chris-Dillon.jpeg "Coast2Coast crew: Greg von Holdt (left), Crispian Dillon (middle) and Gary Shayne. (Photo: Supplied)")

Shayne strongly denied any wrongdoing.

The UIF investment largely settled debt related to acquisitions for the Bounty Brands group, Shayne stated.

However, he chose not to answer several detailed queries regarding the complex series of transactions that effectively converted a portion of the UIF investment into a dividend for Bounty’s shareholders.

Crucially, Shayne and his colleagues have failed to account for exactly how the R530-million in dividends, effectively sponsored by the UIF, had helped to remedy the debt load that later sank the UIF investment.

“I am concerned that my answers would not be portrayed correctly because you are already making assumptions and accusations in your emails and therefore pre-judging the situation with no evidence that there was foul play,” said Shayne.

Sources familiar with these events questioned the business decisions Shayne and his colleagues made prior to and after the UIF investment, with one individual alleging their dealings were “outright dodgy”.

Von Holdt, Botha and Crispian Dillon, Shayne’s co-founder in Coast2Coast, have all seemingly gone to ground.

Scorpio tried to phone the trio for comment, but they didn’t answer our calls. They also appeared to have read requests for comment sent on WhatsApp, but failed to respond.

As Bounty Brands’ equity partner and majority shareholder, Coast2Coast Capital was responsible for sourcing and managing the loans and investments needed for growing the consumer goods group.

This included the UIF’s considerable investment, which was paid to the group via Bright Glacier Trading, an empowerment consortium that held the UIF’s stake in Bounty Brands.

The final go-ahead to invest the funds, meanwhile, came from the Public Investment Corporation (PIC), which acts as the UIF’s investment manager.

The decision to pay the dividend with monies that stemmed from the UIF’s investment warrants serious scrutiny in light of Bounty Brands’ and Coast2Coast’s huge debt load.

As we’ve previously reported, this debt load sparked a crisis when Coast2Coast Capital and its associated entities defaulted on certain liabilities.

Read in Daily Maverick: Shayne’s World: How R1.8bn in UIF cash vanished in Coast2Coast debt hole

The defaults nearly sank the entire group and required a drastic restructuring that ultimately rendered the UIF’s investment next to worthless.

Scorpio’s latest instalment in this series — the result of months of combing through internal company records and engaging with sources — breaks down Bounty Brands’ usage of the R1.37-billion UIF investment.

We’ll specifically focus on the monies that flowed from the group’s South African coffers to effectively bankroll the huge dividend that ended up in foreign bank accounts.

Some of the documents we’ve obtained suggest that a large portion of the dividend sponsored by the UIF investment may have ended up with an offshore company owned by Shayne’s Lighthouse Trust.

The documents may fuel suspicions that Shayne, or at least his trust, had personally pocketed a portion of the UIF’s cash.

Shayne has strongly denied this.

“To be clear, the funds received from Bounty [after the UIF investment] were used to settle debt in the group, a large part of which was incurred to acquire businesses for Bounty. None of the funds paid by the UIF to Bounty were paid to me or the Lighthouse Trust,” he stated.

However, as this investigation will demonstrate, Shayne’s broad denials fail to address vital aspects concerning Shepstone Capital’s usage of the UIF’s money.

As a means to allay our concerns, we also invited Shayne to throw open his trust’s bank accounts and financial statements, along with those of other key entities identified in this piece.

He did not respond to this request.

/file/dailymaverick/wp-content/uploads/2022/07/UIF-queue-Randburg.jpg "The Department of Labour’s (DoL) offices in Randburg, Johannesburg. Every day thousands of South Africans join queues like these at DoL offices across the country to claim payouts from the Unemployment Insurance Fund (UIF). (Photo: Gallo Images / Fani Mahuntsi)")

The money trail

The UIF’s R1.37-billion investment reached Bounty Brands on 14 May 2018.

More precisely, the money came from Bright Glacier Trading, the empowerment consortium that, on 11 May, had received the UIF’s money.

Bright Glacier Trading paid the R1.37-billion investment to K659, one of the myriad entities in the complex web of local and foreign structures that tied Bounty Brands to its equity partner, Coast2Coast.

K659 was the majority shareholder in Bounty Brands (Pty) Ltd, the holding company for the local consumer goods businesses in the Bounty stable.

Included in this collection of businesses were well-known brands like Tuffy homeware products and popular apparel labels like Vans, Diesel and Hurley.

By the time the UIF made the investment, Shayne’s Coast2Coast Capital had already formulated a clear plan for how they would use the money.

This is evident from a “closing schedule” pertaining to the UIF investment, leaked to Scorpio, along with documents filed in an ongoing court case.

According to the documents, K659 distributed the bulk of the funds as follows:

- R592-million went towards settling debentures, a type of debt instrument through which Bounty Brands had secured funding for buying some of the businesses in its portfolio. It is not clear at this point who exactly these debenture holders were.

- R430-million was used to buy back the shares an entity called Brainspan Ventures had held in K659.

- Roughly R200-million went to Bounty Brands SA, an entity in Malta, by means of a “shareholder loan settlement”.

There were also all manner of other payments, including a sweet little capital raise fee of R16.8-million paid to Shayne’s Coast2Coast Capital in Malta.

As we revealed in a previous report, politically connected businessman Lawrence Mulaudzi’s company, Blackgold Oil and Gas, scored a R50-million fee from the deal, of which nearly R6-million seemingly flowed to ANC heavyweight Zweli Mkhize.

Read in Daily Maverick: Exposed: Zweli Mkhize’s R6m ‘cut’ from PIC’s R1.4bn deal using Unemployment Insurance Fund money

Mulaudzi was the intermediary between Coast2Coast, Bright Glacier Trading and the PIC, the UIF’s investment manager.

/file/dailymaverick/wp-content/uploads/2022/07/Greg-and-Lawrence.jpeg "Greg von Holdt and Lawrence Mulaudzi, the PIC dealmaker who brought the UIF’s R1.37-billion investment to Coast2Coast. (Photo: Supplied)")

The focus of this instalment is the R430-million Brainspan buy-back and the R200-million “shareholder loan settlement” paid to the entity in Malta.

By means of these two transactions, Shayne and his colleagues at Coast2Coast effectively removed R630-million of the UIF’s investment from K659’s South African account.

The monies moved through a pipeline of offshore entities in the Coast2Coast and Bounty Brands group before landing at Bounty Brands Holdings, or BBH (UK), the group’s main holding company in the United Kingdom.

It was from BBH (UK) that the group’s shareholders in May 2018 received dividend payments totalling about R580-million, largely bankrolled with the R530-million that came from the UIF investment.

We’ll detail the two main money flows that effectively allowed a considerable chunk of the UIF’s cash to move from South Africa to the offshore accounts.

Along the way, we’ll raise pertinent questions concerning the business rationale behind the series of transactions.

We’ll also scrutinise Shayne’s claim that most of the UIF’s money had been used to lessen the debt load that later crushed the UIF’s investment.

Flow 1: The R430m share ‘buy-back'

When K659 was founded in 2015, an entity called Brainspan Ventures secured a 15% stake in the company, at a nominal cost of only R2,250.

Brainspan was owned by Dillon, Shayne’s co-founder and partner in Coast2Coast Capital.

Roughly three years later, in anticipation of the UIF’s investment, K659 decided that it would buy back Brainspan’s shares in K659.

The buy-back deal was concluded before K659 received the UIF’s money, so the outstanding monies owed to Brainspan sat in K659’s books as a loan.

In other words, by the the time K659 secured the UIF’s R1.37-billion investment, the company owed a debt to Brainspan, one it would be able to repay using the proceeds from the UIF investment.

One could say the debt had been artificially created by the group’s accountants and lawyers on the eve of the UIF investment, an arrangement that would see a substantial portion of the UIF’s funds being diverted from K659’s account.

To settle the “buy-back loan”, K659 on 14 May 2018 transferred a whopping R430-million to Brainspan, all bankrolled with the UIF’s cash.

The value of Brainspan’s 15% stake in K659 had therefore effectively grown from just R2,250 in 2015 to a staggering R430-million in 2018.

This astronomical rise in value was a result of the aggressive acquisitions strategy the broader Bounty Brands group had been following since the group’s inception.

Between 2015 and 2017, K659’s subsidiary, Bounty Brands (Pty) Ltd, acquired several local consumer goods businesses on behalf of the Bounty group.

With each new business Bounty Brands acquired, K659’s value naturally increased, and so too did the value of Brainspan’s stake in K659.

But there is a key consideration one has to keep in mind regarding the value of Brainspan’s stake and the R430-million in UIF funds K659 forked out to buy back those shares.

Neither Dillon nor Brainspan contributed any significant amounts of their own capital to help fund the acquisitions that drove up K659’s value, at least not as far as we were able to establish.

Instead, third party investors and lenders, lined up by Coast2Coast, funded the acquisitions.

/file/dailymaverick/wp-content/uploads/2022/07/Cris-Dillon.jpg "Fishy deal? Crispian Dillon, who co-founded Coast2Coast Capital with Gary Shayne. (Photo: Supplied)")

That Brainspan was able to sell its shares back to K659 for such a high figure was therefore largely made possible by acquisitions funded with other people’s money.

This debt pile eventually grew to about R3.4-billion and would end up triggering the default crisis we unpacked in our previous report.

Meanwhile, Brainspan Ventures now sat with R430-million because it had effectively cashed in on its shares in K659, a transaction K659 had financed with the UIF investment.

The purpose of this transaction, as explained to us by Bounty Brands’ principals, didn’t involve Dillon running off with the R430-million.

Rather, the intention had been to move Brainspan’s “entry point” in the group from K659 to Coast2Coast.

To put it differently, Dillon’s Brainspan Ventures would cease being a shareholder in K659 and instead become a shareholder in a Coast2Coast entity.

To do this, Brainspan would reinvest the proceeds from the buy-back transaction.

According to the records in our possession, this occurred on 16 May 2018, only two days after Brainspan received the funds from K659.

Using the full R430-million, along with additional funds Brainspan had received from K659 through an unrelated dividend, Brainspan forked out €32-million (roughly R470-million at the time) for a stake in Coast2Coast Communications, an entity incorporated in the British Virgin Islands (BVI).

Whatever the business rationale behind this transaction may have been, it had the following crucial outcome — R430-million that came from South Africa’s UIF was summarily moved to an entity located in a well-known offshore tax haven.

A summary of Coast2Coast Communications’ annual financial statements for 2018 provides further information regarding this development.

According to the document, Brainspan had secured an 11% stake in Coast2Coast Communications in exchange for the €32-million investment.

This would have given Coast2Coast Communications a valuation of roughly €290-million, or nearly R4.3-billion, a massive figure for a rather obscure-looking entity.

Some of our detailed questions that Shayne failed to address included the following:

How was Brainspan’s €32-million investment in the BVI entity justified?

What was the underlying value of Coast2Coast Communications at that point in time, and what assets did it own to support such a valuation?

Meanwhile, once the money reached Coast2Coast Communications, the flow of funds was far from over.

It is important to keep in mind that the €32-million, or roughly R470-million, that Brainspan had invested in Coast2Coast Communications largely consisted of the R430-million in UIF funds that had flowed to Brainspan from K659.

The scheme’s designers next saw to it that the full €32-million moved from Coast2Coast Communications to Shepstone Capital, a Coast2Coast entity incorporated in Malta.

Through Shepstone, Shayne essentially held his majority stake in BBH (UK).

But the money didn’t flow directly to Shepstone.

Instead, the funds moved through no less than three Maltese entities, namely Coast2Coast Capital, Coast2Coast Holdings and Coast2Coast Ventures, before the latter entity transferred the money to Shepstone.

Each payment in this series of transactions was treated as a “shareholder loan”, according to the documents in our possession.

The “loan” payments were all concluded in a single day, namely 16 May 2018.

This string of transactions we’ve detailed up to this point may seem confusing, but the key takeaway is this:

Brainspan on 14 May 2018 received R430-million for selling back its shares in K659, and K659 used the UIF’s money to pay for the shares. From Brainspan, this money then skipped through four Coast2Coast entities in the BVI and Malta, before settling at Shepstone Capital in Malta only two days later.

We had hoped Shayne would address the following questions regarding the mechanics behind this flow of funds:

Were there legitimate loan agreements for each “shareholder loan” that effectively drove the funds through the pipeline of Coast2Coast entities?

If so, could Scorpio have a look at them? And what were the conditions and repayment terms for these loans?

Meanwhile, having received the €32-million on 16 May 2018, Shepstone Capital immediately utilised this entire amount to subscribe for shares in BBH (UK).

When BBH (UK) was founded, Shepstone was its 100% shareholder.

Over the years, though, the size of the stake decreased as other investors put money into the group in exchange for equity.

But Shepstone always remained the majority shareholder, and with the latest share purchase, its stake grew to over 70%.

What this purchase of shares effectively also did was to ensure that BBH (UK) now had the full €32-million, or R470-million, largely consisting of the R430-million that emanated from the UIF’s investment in K659 back home in South Africa.

We’ll return to this UK entity after we’ve unpacked a second flow of funds following the UIF’s investment in K659.

Flow 2: The R200m ‘loan settlement’

With the proceeds from the UIF’s R1.37-billion investment, Bounty Brands and Coast2Coast channeled a further €13.35-million, or roughly R200-million at the time, from K659’s South African account to BBH (UK).

This flow of funds is perhaps the most questionable of the two.

Thanks to wily corporate legalese and yet more deft accounting, Bounty Brands’ shareholders effectively converted a chunk of the group’s debt — monies owed to real, third-party creditors — into a dividend for themselves.

Again, it was the UIF’s money that funded these dealings.

The outstanding debts behind the dividends would later play a significant role in the default crisis that effectively scuppered the UIF’s entire investment.

To fully explain how this happened, we need to jump back to the period between 2015 and 2017, when Bounty Brands acquired several consumer goods businesses, or vendors, in its South African portfolio.

The pile of debt within the broader Bounty Brands and Coast2Coast groups partly stemmed from the manner in which these deals were structured.

Bounty Brands didn’t pay the owners of these businesses the entire purchase price at the point of sale.

Instead, the owners received a “day one” payment, consisting of only a portion of the selling price.

The outstanding amounts needed to be paid on different dates in the future, mostly in late 2018 and throughout 2019.

These unpaid debts, or “deferred vendor liabilities”, were initially held within various entities in Bounty Brands’ South African group structure.

Here’s an example:

In 2016, Bounty Brands bought RJ Genesis, a local manufacturer and distributor of cleaning products.

More specifically, Rieses, a subsidiary of Bounty Brands, bought RJ Genesis.

The selling price was roughly R315-million, but RJ Genesis’ owners only received a “day one” payment of about R30-million.

This left a debt of R285-million that needed to be repaid to RJ Genesis’ owners in 2019.

Rieses, the purchasing entity, initially held this "deferred liability".

In this dispensation, Rieses therefore became a debtor entity — it owed money to the owners of RJ Genesis.

But in 2017, this debt was delegated from Rieses to Shepstone Capital, Shayne’s Maltese entity.

In other words, Shepstone would now have to settle the deferred liability owed to the owners of RJ Genesis, not Rieses.

Exactly the same thing was done with the outstanding debts owed to four other businesses Bounty had acquired.

This included Footwear Trading, the distributor and licensee for apparel labels like Diesel and Levi’s.

Reviva, another Bounty Brands subsidiary, had bought Footwear Trading, just as Bounty Brands subsidiary Rieses had bought RJ Genesis.

After the debt delegation, Shepstone would have to settle the debt owed to Footwear Trading's owners, not Reviva.

The total “deferred liabilities” owed to the owners RJ Genesis, Footwear Trading and the three other businesses amounted to roughly R500-million.

When these debts were delegated to Shepstone in 2017, Shepstone became liable for paying the R500-million to the owners of the businesses.

Rieses, Reviva and the other Bounty Brands debtor entities that bought the consumer goods businesses would no longer have to pay the owners.

But their status as debtor entities remained intact, seeing as they now had to pay Shepstone.

Put differently, Shepstone now had receivables from the Bounty debtor entities. Shepstone, in turn, would eventually have to pay the vendors.

In this way, the R500-million heap of debt was essentially taken out of the Bounty Brands group and placed within Shepstone, a Coast2Coast entity.

/file/dailymaverick/wp-content/uploads/2022/07/Group-structure-image.png "The broader Bounty Brands and Coast2Coast groups, and the debt they raised for acquisitions.")

The reason behind this, we were told, related to the intended dual listing of Bounty Brands on the Johannesburg and London stock exchanges, a development that never came to pass.

In anticipation of the dual listing, Coast2Coast, as Bounty’s main shareholder, wanted to reduce the level of debt in Bounty in order to make the group more attractive to would-be investors.

That is why it had Shepstone take over those deferred liabilities.

The owners of the vendor businesses were happy to go along with this, seeing as they would also benefit from the dual listing.

“Without us moving [the differed liabilities to Shepstone] we were led to believe that the London listing would be impossible,” said one owner of a business Bounty had bought.

As mentioned, this arrangement had the effect of leaving Shepstone with receivables from the Bounty Brands debtor entities, including the likes of Rieses and Reviva, but the arrangement didn’t remain in place for long.

Through yet more accounting wizardry, those receivables were directed away from Shepstone to ensure that they would benefit BBH (UK).

Here’s how that happened:

As we’ve mentioned, Shepstone had originally been the 100% shareholder in BBH (UK).

Because shares or equity in a company aren’t free, Shepstone had to buy this stake.

But, as with most things involving Coast2Coast, this transaction was anything but straightforward.

After Shepstone had bought its stake in BBH (UK), Shepstone took back the money it paid for the shares.

This was treated as a loan from BBH (UK) to Shepstone, explained Peter Spinks, Bounty Brands’ CFO.

“This resulted in Shepstone owning shares in BBH (UK) and owing money to BBH (UK),” said Spinks.

Then, around the time of the planned listings, Shepstone sought to reduce this debt it owed to BBH (UK).

It could do so without having to fork out actual money, if it indeed had any.

What Shepstone did have were those receivables from Rieses, Reviva and the other Bounty debtor entities – receivables that sprang from the deferred liabilities Shepstone had absorbed in 2017.

These were promptly assigned to BBH (UK), which essentially accepted the receivables as payment for the debt Shepstone owed it.

Instead of having to pay Shepstone, Rieses and the other Bounty debtor entities now owed money to BBH (UK).

This is where the UIF’s cash comes into play.

To pay the debts the likes of Rieses and Reviva now owed BBH (UK), the accountants from Coast2Coast and Bounty Brands crafted a plan to use the UIF’s investment for this purpose.

In anticipation of the R1.37-billion investment, the bean counters had effectively cut a pathway that would allow BBH (UK) to receive the funds from the Bounty Brands entities in South Africa.

On the South African side of Bounty’s expansive corporate structure, Rieses, Reviva and the other debtor entities sat beneath K659.

By the time the investment came in, the debtor entities had all assigned their obligations to K659, their ultimate parent company in South Africa.

Crucially, K659 happened to be the recipient of the huge pile of UIF cash.

In other words, Rieses, Reviva and the other debtor entities no longer owed anything to BBH (UK).

Instead, K659 became liable for this debt.

In essence, K659 was purposefully saddled with a large chunk of intra-group debt just before the UIF’s investment poured into the company’s coffers.

But BBH (UK) didn’t directly plug into K659, which could have been problematic in terms of getting the funds to the UK entity.

There are, however, few corporate hindrances that can’t be solved with a company resolution or two – or so it seems.

To get its hands on the money, BBH (UK) “novated” these receivables down the chain of offshore entities that gave it an entry point into K659.

First, the receivables were assigned to BB Enterprises, a direct subsidiary of BBH (UK) incorporated in Malta.

BB Enterprises then delegated the receivables to another Maltese entity, Bounty Brands SA (BBSA), which did actually directly own shares in K659.

These arrangements effectively created a pipeline through which monies could now flow from K659 in South Africa to BBH (UK), via the two Maltese entities.

The transfers were effected as “shareholder loan settlements”.

And so, on 17 May 2018 – three days after K659 had received the UIF’s huge investment – K659 paid a “loan settlement” of €13.35-million, or about R200-million, to BBSA.

On that same day, BBSA paid the money to its controlling entity, BB Enterprises.

Finally, also on 17 May, BB Enterprises transferred a “loan settlement” of €13.35-million to its parent entity, BBH (UK).

Some readers may wonder why the “loan settlement” came to only R200-million, considering that the total deferred liabilities for outstanding vendor payments, the very basis for the “loan settlements”, totalled about R500-million.

The answer lies in a simple subtraction.

BBH (UK), as an indirect shareholder in K659, was also a beneficiary of all the assets owned by K659, which included businesses like RJ Genesis and Footwear Trading.

The R200-million, the net receivables, is the result of subtracting the total value of all those assets from the deferred liabilities.

As far as the above chain of transactions is concerned, there are crucial considerations to keep in mind.

The R200-million in “shareholder loan settlements” that flowed from K659 to BBH (UK) weren’t traditional loan repayments – not by any stretch of the imagination.

K659 had never physically borrowed R200-million from BBSA.

Similarly, BBSA had never borrowed R200-million from BB Enterprises, and BB Enterprises had never borrowed R200-million from BBH (UK).

The “loans” instead all related to RJ Genesis, Footwear Trading and the three other consumer goods businesses Bounty had bought through its subsidiaries.

More importantly, the debts owed to RJ Genesis and the other vendors were still outstanding – they were deferred liabilities that hadn’t been settled yet.

In order to reduce the debt it owed BBH (UK), Shepstone had made BBH (UK) the beneficiary of the monies it would have received on the back of the deferred liabilities.

And while Shepstone could now no longer rely on receiving payments from the Bounty Brands debtor entities, it remained liable for settling the deferred liabilities owed to RJ Genesis and the other vendors.

This means BBH (UK) was now effectively receiving R200-million on the back of debts that Shepstone would have to settle.

What’s more, BBH (UK) could evidently do with this money as it pleased, including paying it out as a dividend to its shareholders.

This complex arrangement was, on the face of it, insanely risky.

If Shepstone didn’t settle the deferred liabilities, the entire corporate structure that held Bounty Brands and Coast2Coast together — along with the investments from the likes of the UIF — was at risk of collapsing.

As we’ll come to see, this is pretty much what ended up happening.

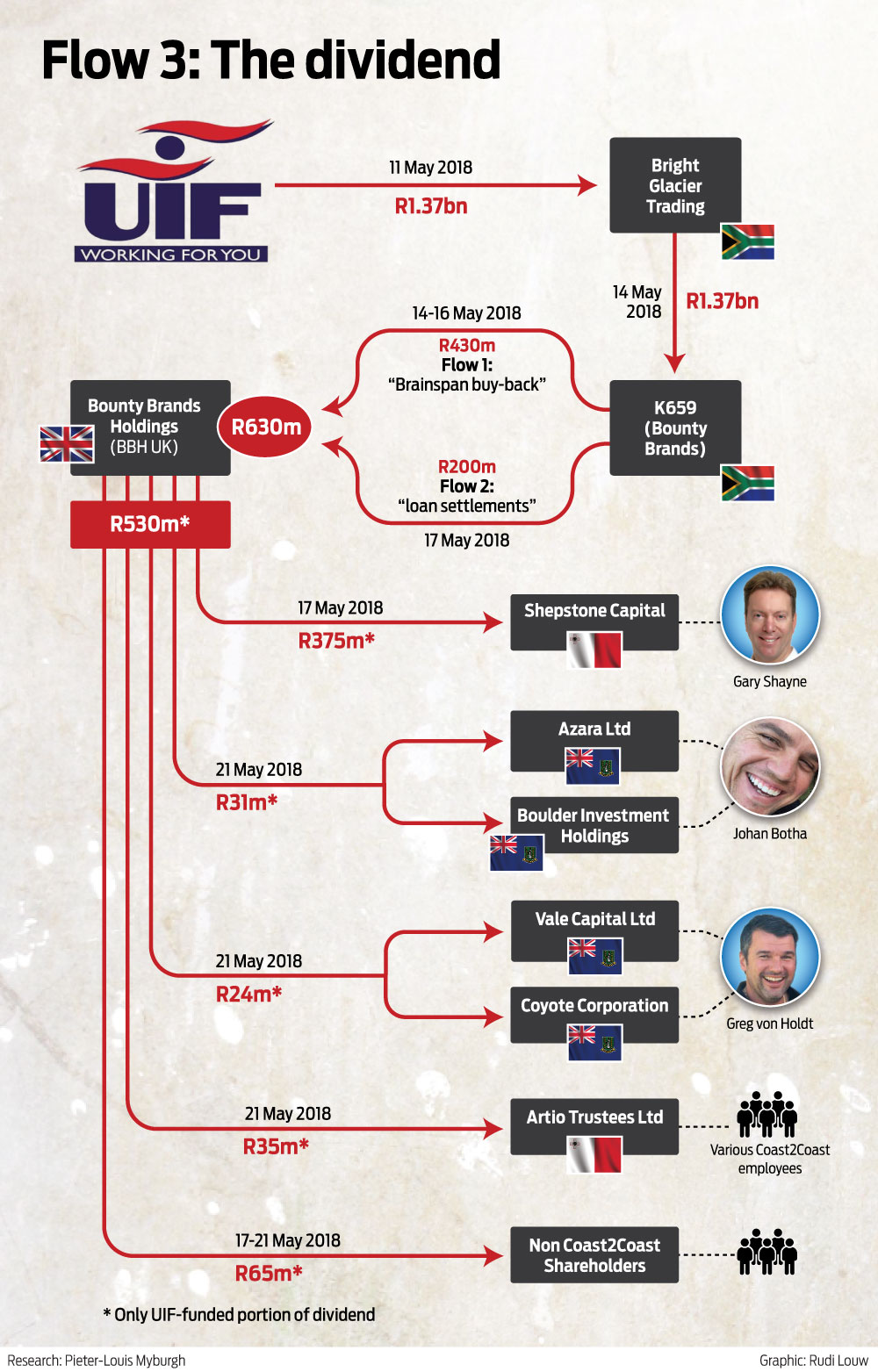

Flow 3: The dividend

Of the R1.37-billion the UIF had invested in Bounty Brands’ K659 entity in South Africa, BBH (UK) now sat with R630-million.

This resulted from the Brainspan share buy-back unpacked in Flow 1, and the “shareholder loan settlement” discussed in Flow 2.

On 17 May 2018, only three days after the UIF’s money had gone into K659, BBH (UK) channeled most of this money to its shareholders in the form of dividends.

As the largest shareholder in BBH (UK), Shayne’s Shepstone Capital would receive most of this money.

BBH (UK)’s May 2018 dividend payments totalled €39-million, or roughly R580-million at the time.

The dividends were paid in euros, but we’ll refer to the rand value for each payment, based on the exchange rate at the time.

BBH (UK) didn’t divvy up the entire R630-million that effectively came its way as a result of the UIF investment, but rather retained nearly R100-million of those funds.

This means roughly R530-million of the R580-million, more than 90% of the dividend, consisted of monies originating from the UIF investment, with the balance funded with the proceeds from an unrelated transaction.

Our focus remains on the R530-million stemming from the UIF investment.

As the largest shareholder in BBH (UK), Shepstone Capital received roughly R375-million of those funds.

Although Shepstone is incorporated in Malta, this money appears to have been paid into the company’s HSBC bank account in the UK, according to a payment schedule.

A further R55-million went to offshore entities whose beneficial owners, according to the payment schedule, were Botha and Von Holdt, Shayne’s colleagues at Coast2Coast Capital.

/file/dailymaverick/wp-content/uploads/2022/07/Johan-Botha-1.jpg "Coast2Coast staffer Johan Botha, one of the beneficiaries of the dividend Bounty Brands Holdings (UK) paid to its shareholders after the UIF’s investment. (Photo: Supplied)")

These entities — Coyote Corporation, Vale Capital Limited, Azara Limited and Boulder Investment Holdings — were all incorporated in the BVI.

However, the funds were seemingly transferred to the entities’ respective bank accounts in Switzerland and the Isle of Man.

Finally, a Maltese entity called Artio Trustees Limited received about R35-million.

According to a legal document, this entity was a nominee company that held a small stake in BBH (UK) on behalf of other Coast2Coast employees.

Of the R530-million in UIF monies that BBH (UK) had paid out as a dividend, roughly R465-million had therefore gone to Shayne’s Shepstone Capital and to his colleagues at Coast2Coast.

The remaining dividend payments emanating from the UIF investment totalled about R65-million and appear to have largely gone to non-Coast2Coast shareholders in BBH (UK).

The final dividend payment was concluded on 21 May 2018, according to the payment schedule.

It had therefore taken only a week to steer hundreds of millions of rands in funds originating from the UIF investment through the pipeline of Coast2Coast and Bounty Brands entities, before the monies ended up as dividends in the foreign bank accounts of Bounty’s shareholders.

Servicing debt

The massive dividend, effectively sponsored with UIF cash, warrants serious scrutiny.

So too does Shayne’s claim that most of the UIF’s investment went towards settling the Bounty group’s debts.

There may very well have been substantial payments to third party debenture holders, but the R630-million that flowed to BBH (UK) — nearly half of the UIF investment — was paid on the back of debts that were, in essence, artificially created through crafty accounting.

K659 wouldn’t have owed R430-million to Brainspan if the buy-back deal hadn’t been concluded before the UIF investment.

Similarly, K659 wouldn’t have owed R200-million to Bounty Brands SA in Malta if the debts owed by the likes of Rieses and Reviva hadn’t been assigned to K659.

Another key driver of the R200-million transfer was the bit of accounting magic through which Shepstone became indebted to BBH (UK) after Shepstone bought shares in BBH (UK), only to borrow back the monies it paid for the shares.

This allowed Shepstone to assign its receivables from the Bounty Brands debtor entities to BBH (UK), opening a channel for a substantial portion of the UIF’s funds to flow to the UK entity, some of which then flowed back to Shepstone and other BBH (UK) shareholders as dividends.

Crucially, it was mostly Shayne’s Shepstone Capital, along with Shayne’s Coast2Coast colleagues, who benefitted from the decision to use UIF money to settle these intra-group debts.

It is difficult to imagine how the monies paid to the offshore entities controlled by Botha and Von Holdt would have contributed towards servicing debts owed to third party lenders.

/file/dailymaverick/wp-content/uploads/2022/07/Greg-and-PA.jpeg "Greg von Holdt and a Coast2Coast colleague during a trip abroad. (Photo: Supplied)")

Instead, these payments may very well have been for the personal benefit of these two Coast2Coast executives.

But the dividend paid to Shayne’s Shepstone Capital evokes even more pressing concerns.

Not only did Shepstone get the lion’s share of what had essentially been UIF funds, but a good portion of the dividend was funded with UIF monies that went to BBH (UK) by means of the “shareholder loan settlements”.

Those payments were a direct result of the deferred liabilities owed to the businesses Bounty Brands had acquired.

In light of this, one would think Shepstone would have used at least a portion of its R375-million UIF-linked dividend for the deferred vendor liabilities.

At the very least, it could have saved some of that money for when those debts became due for repayment.

But it didn’t — at least not to any degree substantial enough to stave off the financial disaster that hit the group later in 2018.

We know this thanks to a confidential stakeholder document prepared by Houlihan Lokey, an American financial advisory firm Bounty Brands later appointed to salvage its dire finances.

The crisis began to unfold in October 2018, only five months after the UIF investment.

This is when Shepstone Capital defaulted on a number of its “financing arrangements”, according to the document. This included some of its vendor obligations — those deferred liabilities owed to the likes of RJ Genesis and Footwear Trading.

In other words, Shepstone had failed to repay its vendor debts, despite the fact that only five months earlier it had received more than R375-million in monies that effectively came from the UIF.

Because of cross-default provisions, Shepstone’s failure to pay these debts left it and other entities in the wider Coast2Coast and Bounty Brands realm in default under other debt facilities.

From that point on, things pretty much went from bad to worse.

/file/dailymaverick/wp-content/uploads/2022/07/Greg-and-Gary.jpeg "Greg von Holdt and Gary Shayne at a gathering before Bounty Brands’ debt crisis. (Photo: Supplied)")

Bounty Brands came within an inch of being liquidated, but a drastic restructuring stopped that from happening.

Unfortunately, this restructuring severely diluted the value of the stakes held by the group’s existing shareholders, so the UIF’s R1.37-billion effectively evaporated.

The key question, then, is what happened to the R375-million in UIF monies in the period between May 2018, when Shepstone received the dividend, and October 2018, when it started defaulting on its obligations?

Why wasn’t some of this money used or saved for the differed vendor liabilities?

Apart from those obligations, Shepstone also sat with a tonne of other debt linked to Bounty Brands’ expansion drive.

It had about R1-billion in deferred vendor payments owing to three Polish businesses in the Bounty Brands portfolio. There were also loans from private investment firms.

On top of this, Shepstone had pledged its own shares in BBH (UK) as security for loans from large institutional lenders like Nedbank and Sanlam, loans that had been taken out by other entities in the interlinked Bounty and Coast2Coast groups.

By all appearances, Shepstone or its related Coast2Coast entities didn’t utilise the UIF funds to service these debts either.

This much seems evident from the Houlihan Lokey document, which includes a detailed presentation of the group’s debt dispensation.

None of the UIF money had seemingly gone towards making dents in any of the debts that remained within the group after the default crisis, the document suggests.

By the end of March 2019, when the Houlihan Lokey document was submitted, Shepstone’s deferred liabilities to the vendors — along with its other debts — had in fact grown because of interest.

The same was true for other debts held in different entities within the wider group structure.

This is why we need to be so circumspect about Shayne’s claim that the UIF monies went towards settling debt within the Bounty group.

Flow 4: Destination Lighthouse Trust?

Remember those intra-group payments from Flow 1?

We detailed how R430-million in UIF monies stemming from the Brainspan buy-back was moved from Coast2Coast Communications in the BVI to Shepstone Capital in Malta.

These payments were effected as “shareholder loans” between the various Coast2Coast entities involved in this chain of transactions.

We also showed how Shepstone then used this money to buy shares in BBH (UK), before a large chunk of this money effectively bounced back from BBH (UK) to Shepstone in the form of the dividends paid out on 17 May 2018.

After its huge dividend payday, Shepstone had a fair sum of money at its disposal.

It could have kept some of this money for the deferred vendor liabilities or other debts owed to third party creditors, but it evidently ranked the “shareholder loans” from its sister entities in the Coast2Coast group as a higher priority.

According to the payment schedule that had been leaked to Scorpio, the following payments were due to be effected after the dividend from BBH (UK).

First, Shepstone would transfer €27.4-million (roughly R406-million) to Coast2Coast Ventures in Malta. This largely consisted of the R375-million that had come into Shepstone’s possession as a direct result of the UIF investment.

The transaction was labelled as a “payment of shareholder loan”, according to the document.

In other words, Shepstone would be repaying the loan from its sister company, the one that had been advanced by Coast2Coast Ventures following the latter’s loan from Coast2Coast Holdings.

As we’ve detailed, these loans were all funded with the UIF monies that went to Brainspan thanks to the buy-back deal, which funds Brainspan subsequently reinvested in Coast2Coast Communications.

From Coast2Coast Ventures, the R406-million was supposed to pass through all those Coast2Coast entities detailed in Flow 1, but in reverse order — at least according to the payment schedule.

The document suggests Shepstone’s dividend, largely bankrolled with the UIF’s money, was used to settle the chain of debts that had been created between the various Coast2Coast entities.

The R406-million would finally end up with Coast2Coast Communications, the entity that had received the buy-back proceeds from Brainspan.

Coast2Coast Communications was also the entity that kicked off the series of loans between the various Coast2Coast companies detailed in Flow 1.

The payment schedule doesn’t tell us what Coast2Coast Communications might have done with the money. Thanks to other documents we’ve obtained, however, we can venture a few guesses.

According to our records, Coast2Coast Communications was owned by Cambridge Capital in the Isle of Man, another Gary Shayne entity.

Cambridge Capital, in turn, was owned by Shayne’s Lighthouse Trust, which was incorporated in Jersey island, a well-known tax haven in the English Channel.

As the ultimate shareholder in Coast2Coast Communications, the Lighthouse Trust was therefore perfectly positioned to receive funds from Coast2Coast Communications.

The Lighthouse Trust, in turn, could then move funds to Shayne’s own pockets.

In fact, we have emails showing how, only a year before the UIF investment, Shayne had used the Lighthouse Trust for this very purpose.

In June 2017, Coast2Coast’s tax advisers were fielding queries from Shayne’s colleagues regarding the Lighthouse Trust.

The Coast2Coast staffers were seeking guidance on how to shield funds from the taxman, monies that Shayne was due to receive from one of his Coast2Coast entities.

“To clarify, if C2C Comms declares a dividend to Cambridge Capital and Cambridge Capital declares a dividend to the Lighthouse Trust and then Lighthouse makes a distribution to Gary [Shayne] all in the same tax year… the distribution would NOT be taxable in Gary’s hands?” reads one of the mails.

In other words, the corporate architecture that would allow funds to flow from Coast2Coast Communications to Shayne via Cambridge Capital and the Lighthouse Trust seemed to have been well established.

Shayne expressly denied that any of the UIF funds had flowed to him via the Lighthouse Trust in the manner discussed in the email.

“The email you have shown above occurred almost a year before the UIF invested into Bounty and has nothing to do with money invested by the UIF,” said Shayne.

One thing that did occur after the UIF investment, however, was the conclusion of the 2018 annual financial statements for all those Coast2Coast entities mentioned in this piece.

Summary notes for Coast2Coast Communications’ financial statements include some interesting remarks.

According to the document, the company declared an $18.52-million dividend (about R245-million at that time) to its ultimate shareholder, the Lighthouse Trust.

The dividend had been declared before Brainspan “reinvested” its R430-million from the UIF-sponsored buy-back deal in Coast2Coast Communications, according to the document.

“The dividend will be paid as and when capital is available in the group,” stated the notes, which were seemingly published in November 2018.

In other words, Coast2Coast Communications was poised to channel R245-million to Shayne’s Lighthouse Trust after the UIF deal.

We don't know if this happened, or whether any of the UIF's money bankrolled such a dividend.

What is certain, though, is that R630-million of the UIF’s R1.37-billion investment flowed to BBH (UK) by means of the dizzying string of transactions described in this piece.

We also know that BBH (UK) then used about R530-million of those funds to pay dividends, mostly to Shayne’s Shepstone Capital and to entities controlled by his colleagues at Coast2Coast.

From Shepstone, a chunk of what had essentially been the UIF’s money appeared to have gone to one of Coast2Coast’s entities in the BVI.

Considering the UIF’s huge loss following these dealings, it is only reasonable to demand from Shayne and his Coast2Coast colleagues an exhaustively detailed account of what exactly became of the R630-million that exited South Africa in May 2018. DM

![]()

Comments

Scroll down to load comments...