Key takeaways:

- Despite Covid-19, a significant divide remains between digital leaders and laggards in the corporate world.

- Our analysis shows that digital leaders are growing at almost five times the rate of the digital laggards.

- Comparing Nike and Asics shows that Nike’s foresight in investing in digitalisation has delivered better revenue and profitability metrics.

- Given our focus on growth and quality, we consider some of the best investment opportunities today lie in investing in both traditional and new businesses that embrace digitalisation.

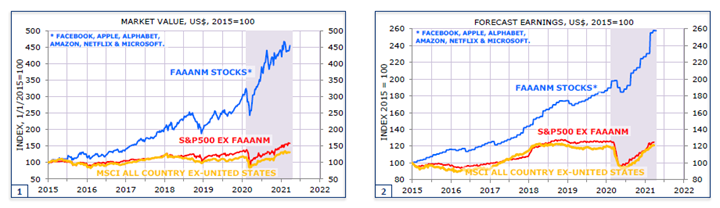

Firstly, taking a step back, the charts below also show the dominance of a handful of companies on the S&P and MSCI ACWI ex US market value and forecast earnings. What all of these companies (Facebook, Apple, Alphabet, Amazon, Netflix & Microsoft) have in common is their digital prowess. Is this the reason for their success?

We asked our research analysts to identify the digital leaders and laggards within their sector(s) and identified 114 companies across seven sectors which formed the basis of our analysis. We used internal forecasts which allowed us to access more relevant annual earnings per share (EPS) growth on a five-year basis.

Perhaps unsurprisingly, our analysis shows that digital leaders are growing at almost five times the rate of digital laggards.

/file/dailymaverick/wp-content/uploads/2022/04/Graph2-Stanlib.png "Source: J.P. Morgan Asset Management, December 2021. Please note, opinions, estimates, forecasts, projections and statements of financial market trends are based on market conditions at the date of the publication, constitute our judgement and are subject to change without notice. There can be no guarantee they will be met.")

Why is this the case? We have taken a closer look at a leader and a laggard in the same industry, Nike and Asics. Both companies have a very long history but Nike has grown into a far larger company.

Looking at more recent history, we can see the two companies really started to diverge in their sales growth, income growth and profitability in the last few years.

/file/dailymaverick/wp-content/uploads/2022/04/Graph-3-Stanlib-1.png "Source: J.P. Morgan Asset Management, Nike Annual Reports, Asics Annual Reports. December 2021. EBIT is earnings-before-interest-and-taxes")

Even more interesting is that, while the gross profit margin of the two businesses has been remarkably similar, the profit at operating level has diverged meaningfully.

/file/dailymaverick/wp-content/uploads/2022/04/Graph4-Stanlib.png "Source: J.P. Morgan Asset Management, Nike Annual Reports, Asics Annual Reports. December 2021")

We suggest one key reason for Nike’s success is its foresight in investing in digitalisation – and far earlier than its peers.

Nike has a huge scale advantage over competitors in employing its digital capabilities, making it viable to invest in initiatives such as the Nike training apps and the Nike run club, purely for better direct consumer engagement. This highly engaged traffic drives higher visitations to Nike’s commercial platforms, resulting in higher repeat purchases from app members and increasing average basket size. Already, 30% of Nike’s business is digital, and its ambition is 50%.

“At NIKE, innovation is a systemic approach and it's how we extend our lead”.

/file/dailymaverick/wp-content/uploads/2022/04/Graph5-Stanlib.png "Source: J.P. Morgan Asset Management, Nike Annual Reports, Asics Annual Reports.December 2021")

We also analysed the return on equity for both the laggards and the leaders and found that the leaders were not only growing faster but they were also producing better returns.

/file/dailymaverick/wp-content/uploads/2022/04/Graph6-Stanlib.png "Source: J.P. Morgan Asset Management. December 2021")

The difference was of a smaller magnitude than the growth rate, however the leaders exhibited a ROE of 19% compared with the laggards’ 15%, and 14% for the coverage universe.

Many investors assume that a fast-growing company is likely to be more risky and have more debt. This is not what we found. The analysis below considers total debt to equity and shows that the leaders are far less leveraged at 0.78x than the laggards at 1.38x. The reason that leverage is not a strong feature of digital leaders is the availability and appetite of funding for newer, innovative companies.

/file/dailymaverick/wp-content/uploads/2022/04/Graph7-Stanlib.png "Source: J.P. Morgan Asset Management. December 2021")

We should also note that not all the stocks picked as digital leaders are new companies. Many, such as Paypal, Assa Abloy, Tencent, Otis, HDFC Bank, Allegion, Accenture, Mastercard, Nike, L’Oreal, Microsoft and Starbucks have maintained top positions because of their digital leadership.

A strong partnership

Through the strategic partnership with J.P. Morgan Asset Management (JPMAM), STANLIB is providing SA investors an opportunity to gain access to significant global reach and depth of expertise. DM/BM

Authors:

Caroline Keen, is a portfolio manager within the J.P. Morgan Asset Management International Equity Group, based in London. An employee since 2019, Caroline was a portfolio manager at Newton Investment Management, where she was on the Emerging Markets and Asia equity team, with responsibility for Asia Pacific ex Japan Portfolios. Caroline holds a B.A. degree in Politics, Philosophy and Economics from St. John's College, Oxford. She is a CFA charterholder.

Alex Stanic, is a portfolio manager within the J.P. Morgan Asset Management International Equity Group, based in London. An employee since 2015, Alex was Head of Global Equities at River & Mercantile Asset Management, having founded the division in 2009. Alex holds a MA in economic & Social Geography from Edinburgh University.

Important notes:

The companies above are shown for illustrative purposes only. Their inclusion should not be interpreted as a recommendation to buy or sell.

This is a marketing communication and as such the views contained herein are not to be taken as advice or a recommendation to buy or sell any investment or interest thereto. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and investors may not get back the full amount invested. Past performance and yield are not a reliable indicator of current and future results. There is no guarantee that any forecast made will come to pass. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co. and its affiliates worldwide. Our EMEA Privacy Policy is available at www.jpmorgan.com/emea-privacy-policy. This communication is issued in Europe (excluding UK) by JPMorgan Asset Management (Europe) S.à r.l.and in the UK by JPMorgan Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. 09li221603125003