Answer: There are often costly unintended consequences when you draw up a will. These often come in the form of capital gains tax and estate duty.

Estate duty and capital gains tax are levied when someone dies. If the full estate is bequeathed to the surviving spouse, however, these will only be payable when the second spouse dies. If anything is bequeathed to anyone else, including your children, the capital gains tax and estate duty on that bequest will have to be paid immediately.

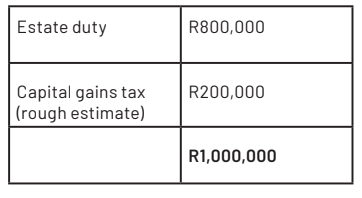

In your situation, as 50% of the value of the house will go to the children the following taxes will be payable should your wife die before you:

Your wife’s bequest of 50% of the property to your sons will require that these amounts be payable when her estate is wound up. Had it been bequeathed to you, it would only be payable on your death.

There are further implications that you need to consider. Will you carry on living in the family home or will it be sold?

If you want to carry on living in the home, it may be an idea to add a clause in your will that gives you the option of paying out your children 50% of the current market value of the house.

Now, do you have R4-million in liquid assets that could be used to pay out the children? If not, then it may be worth taking out life insurance on your wife to cover this cost, the estate duty and capital gains tax.

A neater solution, if your wife is amenable, would be for your wife to take out life insurance equal to 50% of the value of the home and make the children the beneficiaries.

She can revise the cover regularly to ensure that it keeps pace with the changing property value.

The advantages of this approach are:

- You don’t have to leave the family home if she passes away.

- Your children get their inheritance immediately and smoothly.

- You delay paying the estate duty and capital gains tax until you die.

Insider tip

Make sure that you have a will that is stored securely.

If no will can be found then your assets will be divided according to a formula. This will result in capital gains tax and estate duty on the children’s shares being payable immediately.

You could end up having to sell your home to pay these taxes. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper, which is available countrywide for R25.

Comments

Scroll down to load comments...